Global| May 11 2015

Global| May 11 2015Dutch IP Surprisingly Sags as EMU Outlook Hangs on Greece

Summary

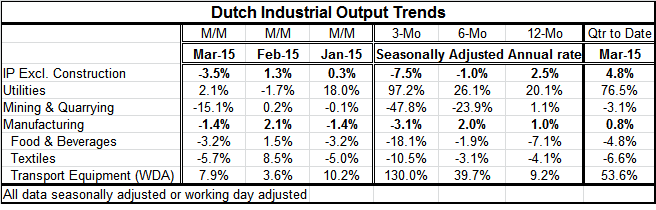

Dutch manufacturing and overall IP both fell in March. Overall IP fell for the first time in two months while manufacturing had fallen in two of the last three months. Trends for IP are not good. Utilities output and transportation [...]

Dutch manufacturing and overall IP both fell in March. Overall IP fell for the first time in two months while manufacturing had fallen in two of the last three months.

Dutch manufacturing and overall IP both fell in March. Overall IP fell for the first time in two months while manufacturing had fallen in two of the last three months.

Trends for IP are not good. Utilities output and transportation equipment (the latter, working day adjusted but not seasonally adjusted) are showing some explosive growth from 12-month to six-month to three-month. But overall IP and manufacturing totals do not echo that strength.

Both manufacturing and overall IP are showing more or less progressive contraction in output trends. Overall IP excluding construction IP is growing at a 2.5% pace; over 12 months but is contracting at a rapid 7.5% annual rate over three months substantially because of a 3.5% drop in output in March.

In manufacturing, output is up by 1% over 12 months and is higher over six months but is contracting at a 3.1% annual rate over three months. The Netherlands show no sign of growth building in the EMU.

However, in the quarter to date, Dutch IP is up at a 4.8% annual rate and IP is up at a small but positive 0.8% annual rate.

The Dutch result fits in with most of the EMU results reported so far as Germany also showed declines in overall output and in manufacturing over three months but registered net gains for both in the recently completed first quarter (quarter-to-date column). Among the EMU-members that have reported IP, only Finland has a quarter-to-date decline. Even Greece has as a strong gain on the measure. And Greece continues to hang over the outlook for all of the EMU.

It's all Greek to me...

As expected, the European finance ministers that met today did not take any action on Greece. Greece made its 750 million euro payment to the IMF, but the euro group wants more concessions from Greece and Greece wants some admission of the progress it has made in order to unlock the current bailout funds that are being locked up. There is still disagreement about the red lines Greece still claims it will not cross because of election promises made. Yet, euro group members still seek Greece to stick with the deal it made to get those funds. Greece is now on a very short tether. It clearly believes it has done enough to get the next tranche of monies while so far the EMU position has been to not agree to disperse funds as long as Greece has in a one-sided way decided to change the deal. I suspect this is the real sticking point, how Greece has gone about it.

You may recall that Greece was downgraded a few weeks ago by S&P when the euro group made it clear it would not cut Greece more slack and forgive debt. The S&P view is that without debt forgiveness Greece is not viable. If S&P is right, it is hard to understand what all this debating is about. Either Greece will be ejected from the EMU because it cannot pay its bills or realizing that the current deal is not sustainable, the euro group will forgive debt and try to offer Greece a path to survival. But being stinky now about past terms and conditions when even adhering to those terms leads only to a dead end makes no sense. Yet that, it seems, is the crossroads where Europe and Greece are stuck. Even if Greece gets through this, it's out of the frying pan, into the fire, as J.R.R. Tolkien might say.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief