Global| Jun 25 2003

Global| Jun 25 2003Durable Goods Orders Slip

by:Tom Moeller

|in:Economy in Brief

Summary

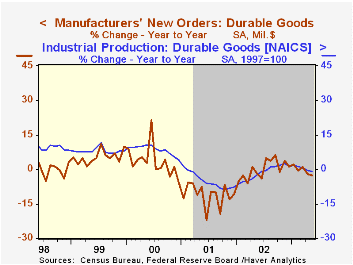

Durable goods orders slipped 0.3% in May versus the Consensus expectation for a 1.0% rise. April figures were little revised. Sharp declines in orders for transportation equipment, off 1.6%, and electrical equipment, down 2.2%, were [...]

Durable goods orders slipped 0.3% in May versus the Consensus expectation for a 1.0% rise. April figures were little revised.

Sharp declines in orders for transportation equipment, off 1.6%, and electrical equipment, down 2.2%, were offset by gains in orders for computers and electronic products. Excluding the transportation sector altogether, durable orders fell 0.4% (-3.3% y/y.

Nondefense capital goods orders fell 0.9% and have been virtually flat since early last year. Excluding aircraft and parts, nondefense capital goods orders fell 0.5% (-0.1% y/y).

During the last ten years there has been a 74% correlation between the y/y change in orders for durable goods and the change in industrial production of durable goods.

Shipments of durable goods fell 0.3% (-4.0% y/y) and it was the third monthly decline this year.

Durable inventories fell 0.2% (-1.4% y/y) for the fifth consecutive monthly decline.

| NAICS Classification | May | April | Y/Y | 2002 | 2001 | 2000 |

|---|---|---|---|---|---|---|

| Durable Goods Orders | -0.3% | -2.4% | -2.7% | -0.1% | -11.4% | 3.3% |

| Nondefense Capital Goods | -0.9% | 0.0% | -1.5% | -5.3% | -16.5% | 7.9% |

by Tom Moeller June 25, 2003

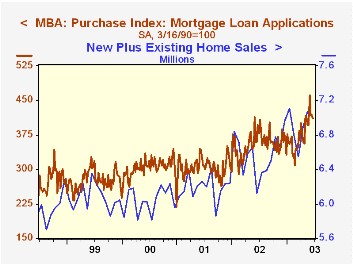

The index of mortgage applications compiled by the Mortgage Bankers Association fell 8.7% last week. The decline pulled the index to the lowest level in five weeks.

Applications to refinance fell 10.5% w/w and are down 17.8% from the peak in late May.

Applications for home purchase fell 1.9% w/w and are down 10.7% from the late May peak. Nevertheless, applications so far in June are about even with the record May level.

During the last ten years there has been a 52% correlation between the y/y change in purchase applications and the change in new plus existing home sales.

Interest rates on a conventional 30-Year mortgage ticked higher w/w with the effective rate at 5.43% versus 6.13% averaged in December. The effective rate on a 15-year mortgage also rose slightly w/w to 4.87% versus 5.55% averaged in December.

The Mortgage Bankers Association surveys between 20 to 35 of the top lenders in the U.S. housing industry to derive its refinance, purchase and market indexes. The weekly survey accounts for more than 40% of all applications processed each week by mortgage lenders.

Visit the Mortgage Bankers Association site at www.mbaa.org.

| MBA Mortgage Applications (3/16/90=100) | 6/20/03 | 6/13/03 | 2002 | 2001 | 2000 |

|---|---|---|---|---|---|

| Total Market Index | 1,554.5 | 1,701.7 | 799.7 | 625.6 | 322.7 |

| Purchase | 411.2 | 419.1 | 354.7 | 304.9 | 302.7 |

| Refinancing | 8,204.6 | 9,162.7 | 3,388.0 | 2,491.0 | 438.8 |

by Tom Moeller June 25, 2003

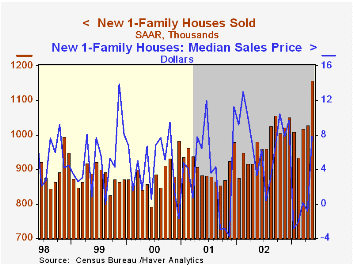

Sales of new single family homes in May jumped 12.5% m/m to 1.157M, a new record. The surge followed generally sideways movement during the prior nine months. Consensus expectations were for a 1.035M May sales rate.

Sales strength was concentrated in the West where sales rose 19.7% (20.9% y/y) and in the South where sales rose 15.9% (25.1% y/y).

Elsewhere in the country sales where mixed: down 9.0% (-1.4% y/y) in the Northeast and up 1.6% (3.4% y/y) in the Midwest.

The median price of a new home rose to $195,200 (7.8% y/y) and the prior month was revised up.

The new home sales data reflect current sales versus the existing home sale figures which reflect closings on past sales.

| Homes Sales (000s, AR) | May | April | Y/Y | 2002 | 2001 | 2000 |

|---|---|---|---|---|---|---|

| New Single-Family | 1,157 | 1,028 | 17.9% | 977 | 907 | 880 |

by Tom Moeller June 25, 2003

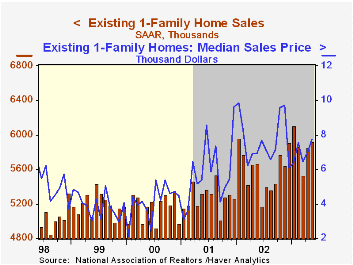

Sales of existing single family homes rose 1.2% last month to 5.920M. The gain pulled sales close to the record level set this past January. Consensus expectations were for 5.84M.

Home sales in May were mixed across the country's regions: up in the Northeast and up in the Midwest but down just slightly in the South and the West.

The median price of an existing home rose to $167,000 (+7.7% y/y).

The figures reflect closings of past home sales.

| Existing Home Sales (000, AR) | May | April | Y/Y | 2002 | 2001 | 2000 |

|---|---|---|---|---|---|---|

| Existing Single-Family | 5,920 | 5,850 | 4.4% | 5,598 | 5,282 | 5,158 |

by Tom Moeller June 25, 2003

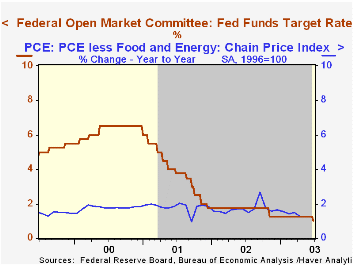

The Federal Reserve lowered the target rate for federal funds 25 basis points to 1.00%, the lowest level since 1958. The discount rate also was lowered by a quarter point to 2.00%.

The action was less aggressive than expected by most economists and it was not unanimous. San Francisco Bank President Parry preferred a 50 basis point reduction.

The press release which accompanied the Fed’s action contained the following statement. "The economy ... has yet to exhibit sustainable growth. With inflationary expectations subdued, the Committee judged that a slightly more expansive monetary policy would add further support for an economy which it expects to improve over time."

With regard to the risks to the economic outlook, the Fed stated that "the upside and downside risks to the attainment of sustainable growth are roughly equal." The Fed statement added that "the probability, though minor, of an unwelcome substantial fall in inflation exceeds that of a pickup in inflation from its already low level."

Here is the complete text of the Fed's latest press release.

A paper presented by Federal Reserve Board Governor Donald L. Kohn and Senior Economist Brian P. Sack titled "Central Bank Talk: Does it Matter and Why?" can be found here.

"Why Predict Past FOMC Actions" from the Federal Reserve Bank of St. Louis is found here.

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief