Global| Apr 19 2006

Global| Apr 19 2006CPI Up An Expected 0.4% During March

by:Tom Moeller

|in:Economy in Brief

Summary

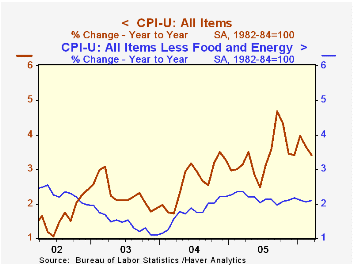

During March, the consumer price index (CPI-U) rose 0.4% following a 0.1% February up tick and matched Consensus expectations. The 0.3% rise in prices less food & energy, however, was slightly firmer than expected. Prices for core [...]

During March, the consumer price index (CPI-U) rose 0.4% following a 0.1% February up tick and matched Consensus expectations. The 0.3% rise in prices less food & energy, however, was slightly firmer than expected.

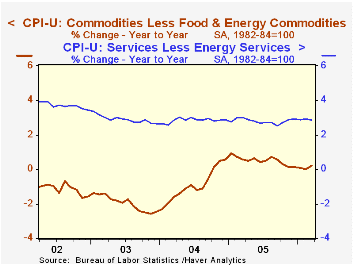

Prices for core goods rose 0.3% (0.2% y/y) after a 0.1% February decline. Apparel prices reversed all of the prior month's drop with a 1.0% (-1.2% y/y) increase and household furnishings & operation prices ticked up 0.1% (0.5% y/y) after no change during February. Medical care commodity prices rose 0.4% (4.1% y/y) while tobacco prices rose a strong 0.6% (4.5% y/y). New & used motor vehicle prices fell 0.1% (+0.4% y/y).

Another 0.3% increase in core services prices reflected a second 0.4% (2.6% y/y) increase in shelter prices. Medical care services prices increased 0.4% (4.1% y/y) while school tuition & fees posted a firm 0.5% (6.1% y/y) gain. Public transportation prices fell by 0.3% (+5.9% y/y), the third decline in the last four months.

Energy prices during March reversed all of the prior month's decline with a 1.3% jump led by a 3.6% (17.0% y/y) spurt in gasoline prices, which have moved 10.7% higher so far during April. Natural gas & electricity prices fell 1.1% (+17.8% y/y) for the third decline in the last four months and fuel oil prices ticked up 0.4% (17.9% y/y).

Food prices inched up another 0.1%, the gain held back by a 1.7% (+6.4% y/y) decline in fruits & vegetables prices. Meat, fish & poultry prices reversed all of the prior month's decline with a 0.3% (0.9% y/y) rise.

The chained CPI, which adjusts for shifts in the mix of consumer purchases, jumped 0.5% and less food & energy prices rose a stronger 0.6%.

Minutes to the latest FOMC meeting can be found here.

The Interaction of Labor Markets and Inflation: Micro Evidence from the International Wage Flexibility Project from the Federal Reserve Bank of San Francesco is available here.

| Consumer Price Index | Mar | Feb | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Total | 0.4% | 0.1% | 3.4% | 3.4% | 2.7% | 2.3% |

| Total less Food & Energy | 0.3% | 0.1% | 2.1% | 2.2% | 1.8% | 1.5% |

| Goods less Food & Energy | 0.3% | -0.1% | 0.2% | 0.5% | -0.9% | -2.0% |

| Services less Energy | 0.3% | 0.3% | 2.8% | 2.8% | 2.8% | 2.9% |

| Energy | 1.3% | -1.2% | 17.3% | 16.9% | 10.8% | 12.2% |

| Food | 0.1% | 0.1% | 2.6% | 2.4% | 3.4% | 2.1% |

| Chained CPI: Total (NSA) | 0.5% | 0.3% | 3.0% | 2.9% | 2.5% | 2.0% |

| Total less Food & Energy | 0.6% | 0.4% | 2.0% | 1.9% | 1.7% | 1.1% |

by Tom Moeller April 19, 2006

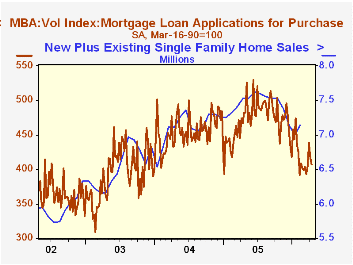

The total number of mortgage applications fell hard for the second consecutive week and posted a 1.7% drop. So far during April applications are 0.9% below the March average which fell 1.0% from February.

Purchase applications fell 2.5% w/w following the 4.7% drop to open the month but the April average so far is up 1.2% from March, which rose 0.2% versus February.

During the last ten years there has been a 54% correlation between the y/y change in purchase applications and the change in new plus existing single family home sales.

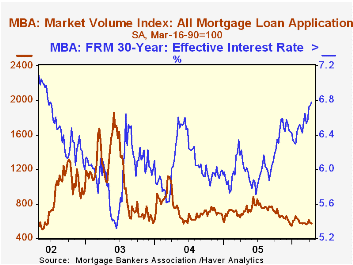

Applications to refinance slipped 0.4% after a 6.6% slide the prior week and in April are 4.1% below the March average.

The effective interest rate on a conventional 30-year mortgage rose further to 6.78% while the rate on 15-year financing rose to 6.%. Interest rates on 15 and 30 year mortgages are closely correlated (>90%) with the rate on 10 year Treasury securities and during the last ten years there has been a (negative) 82% correlation between purchase applications and the effective rate on a 30-Year mortgage.

The Mortgage Bankers Association surveys between 20 to 35 of the top lenders in the U.S. housing industry to derive its refinance, purchase and market indexes. The weekly survey accounts for more than 40% of all applications processed each week by mortgage lenders. Visit the Mortgage Bankers Association site here.

States Fight Predatory Lending in Different Ways from the Federal Reserve Bank of St. Louis can be found here.

| MBA Mortgage Applications (3/16/90=100) | 04/14/06 | 04/07/06 | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Total Market Index | 569.6 | 579.4 | -15.3% | 708.6 | 735.1 | 1,067.9 |

| Purchase | 407.4 | 417.7 | -12.7% | 470.9 | 454.5 | 395.1 |

| Refinancing | 1,526.1 | 1,532.4 | -18.4% | 2,092.3 | 2,366.8 | 4,981.8 |

by Carol Stone April 19, 2006

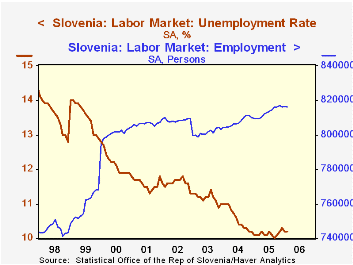

The labor market seems to be slowing just a bit in Slovenia, according to the monthly labor force survey reported today by the Statistical Office; after climbing from April 2005 through November, employment has been virtually flat since then through February. Even so, at 816,156, it stands 0.8% above a year ago, matching the growth pace for all of 2004, and close to that for the rest of Europe.

Unemployment continues stubbornly just above 10%, with January and February at 10.2%. This is low historically for the country, but as employment has apparently stopped increasing, unemployment has stopped decreasing. It bottomed out at exactly 10.0% in September.

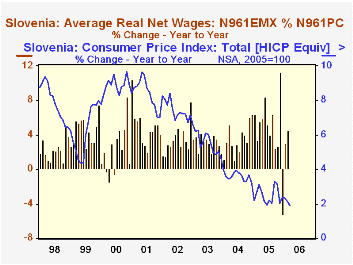

Workers, meantime, appear to be doing "all right". Their average wages, which were published yesterday, were SIT179.7 in February (SIT=Slovenian Tolars), after social security and income tax withholding. This marks a 2.7% real advance from February 2005, allowing for the 2.1% CPI inflation over the period. Real earnings in the rest of Europe were up just 0.4% in 2005, measured by wages and salaries for the EU-25 calculated by Eurostat.

The average wage indicator hints at general gains in the Slovenian economy; GDP per capita real growth (in fixed 1995 prices) was 4.1% last year. According to the CIA World Factbook, Slovenia is the first transition economy to change from borrower to donor status at the World Bank, and its currency, presently pegged to the euro, is due to switch to the euro next year. All is not completely well, though, as the population has been almost completely flat since 1999; there was net out-migration during the break-up of Yugoslavia, then a modest recovery from 1999 to 2002, but almost no change since. And as we note here, the economy may be showing signs of plateauing after a nice run during 2005.

Country-source data on Slovenia are found in Haver's EMERGECW database. Since the country joined the European Union in 2004, data generated by Eurostat are also found in the EUROSTAT database. The CIA's helpful information on the general characteristics of the country are found here.

| Slovenia | Feb 2006 | Jan 2006 | Feb 2005 | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Employment (SA, Thous.) | 816.2 | 816.6 | 809.6 | 813.1 | 807.5 | 801.4 |

| % Change (Mo/Mo & Yr/Yr) | -0.0 | 0.0 | (yr/yr) 0.8 | 0.7 | 0.8 | -0.9 |

| Unemployment Rate (SA, %) | 10.2 | 10.2 | 10.1 | 10.1 | 10.6 | 11.2 |

| Average Net Wages (Thous. Tolars) |

179.7 | 179.3 | 171.4 | 177.1 | 168.2 | 159.1 |

| "Real" % Change* (Mo/Mo & Yr/Yr) |

-0.2 | 2.0 | (yr/yr) 2.7 | 2.7 | 2.1 | 1.8 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.