Global| Nov 30 2020

Global| Nov 30 2020China's Manufacturing PMI Pushes Higher

Summary

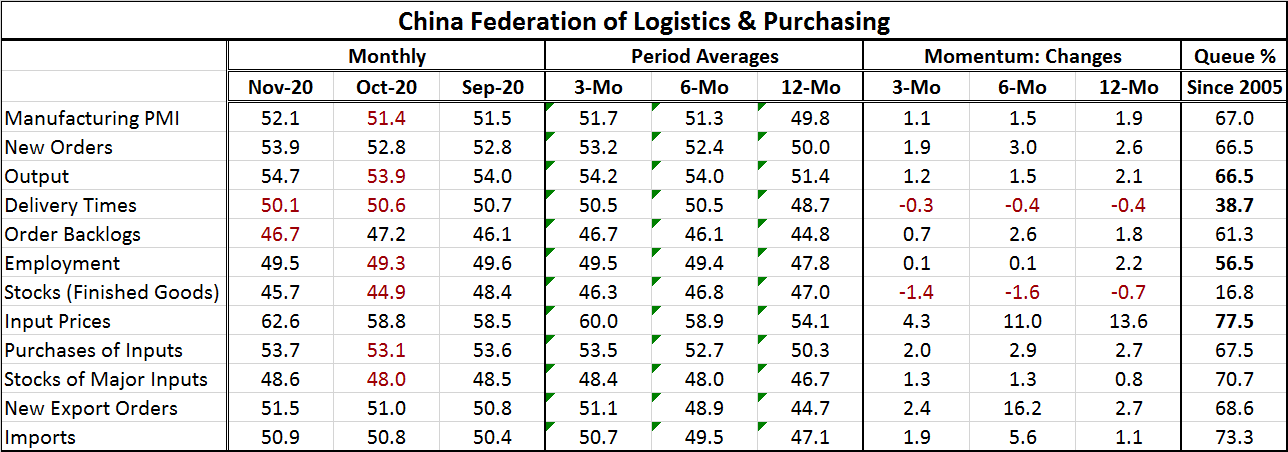

China's manufacturing PMI moved up to a reading of 52.1 in November from 51.4 in October after posing readings in the 51 area for four months in a row. The break-out gain is the highest reading since September 2017. The index has not [...]

China's manufacturing PMI moved up to a reading of 52.1 in November from 51.4 in October after posing readings in the 51 area for four months in a row. The break-out gain is the highest reading since September 2017. The index has not surpassed the current month's value for two months in a row since April 2012 and has not been steadily above this mark since April 2011. The index rise of 0.7 points month-to-month also ranks as the 34th strongest month-to-month gain in the headline index in the past 190 months marking it as a top 17th percentile magnitude gain. Still, on data back to January 2005 the current index stands only in its 67th percentile, a respectable standing but hardly strong.

China's manufacturing PMI moved up to a reading of 52.1 in November from 51.4 in October after posing readings in the 51 area for four months in a row. The break-out gain is the highest reading since September 2017. The index has not surpassed the current month's value for two months in a row since April 2012 and has not been steadily above this mark since April 2011. The index rise of 0.7 points month-to-month also ranks as the 34th strongest month-to-month gain in the headline index in the past 190 months marking it as a top 17th percentile magnitude gain. Still, on data back to January 2005 the current index stands only in its 67th percentile, a respectable standing but hardly strong.

Virus issues

With Europe having been enshrouded in a round of economic closures, this performance for China's manufacturing sector is quite good. Globally the virus is still a problem and only now some European countries are beginning to come out from behind their recent wall of restrictions. France is coming out, Germany is delaying, while the U.K. still has major lockdowns in force. So China seems to be making its move without much help from Europe. U.S. growth has continued and that is a supportive factor for China although the virus in the U.S. has continued to spread. The impact on the U.S. economy has been in this round so far delayed. But with the U.S. virus spread extending and a major holiday just having passed where travel was in fact pursued by many despite CDC warnings to ‘stay home' the U.S. could yet become a break on global growth with potential adverse effects for China and other Asia.

China shows for the most part modest queue standings for its index components. The strongest components by queue standing in order are (1) input prices, (2) imports, (3) stocks of major inputs, (4) new export orders, and (5) purchases of inputs. This list highlights prices, the international sector and stock building as key components in Chinese manufacturing recovery.

The weakest components by queue standing are (12) stocks of finished goods, (11) delivery times, (10) employment, (9) order backlogs and, tied for 7th and 8th, are new orders and output. This list highlights that despite finished stocks as low and domestic slack (delivery speeds and backlogs), employment is lagging and output and orders also lag. The standing for output and orders is just below the standing for the entire index.

On one hand the ranking for finished stocks is low but on the other indicators of domestic demand is lacking. Stock building would seem to make sense and purchases of inputs and stocks of inputs have been strength leaders. Still, demand seems largely to be from abroad. So far, employment is not being pressured higher by the revival. Order backlogs are weak and firms are easily able to fulfill orders judging from delivery speed assessments.

The three-month moving averages show progression to higher level across components with only finished stocks seeing a lower three-month reading than its six-month reading. Delivery speeds are flat six-months to three-months. Away from the period averages, simple changes on the same horizons show some persistent weakness in delivery times and in the stocks of finished goods. Neither of these are a good signal that growth is really building any head of steam. In fact, the monthly changes for finished goods stocks, stocks of major inputs, and imports all show greater change over three months than over 12 months revealing these gains to be quite recent. But other components show no reason for the stock building surge. Employment has only seen gains over three months that are 5% of their 12-month change. Order backlogs show a modest proportion of their strength over three months as well.

Aside from the PMI itself which is typically constructed by giving differing weights to the index components, those components in November have individual queue standings that average only in their 60.4 percentile - well below the 67.0 percentile standing for the headline. Extreme weakness in the standing of finished stocks and in delivery speeds contribute importantly to this rankings gap.

On balance, China's manufacturing sector seem to be on the mend. But the data are not a ringing endorsement of that and some of the PMI components rankings leave a lot to be desired. China's reported data are often subject to second-guessing. This month a close inspection of the data does yield some sizeable gaps in component strength despite a headline that seems to be progressing nicely.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief