Global| Aug 19 2005

Global| Aug 19 2005Chicago Fed Nat'l Activity Index Suggests Above Trend Growth

by:Tom Moeller

|in:Economy in Brief

Summary

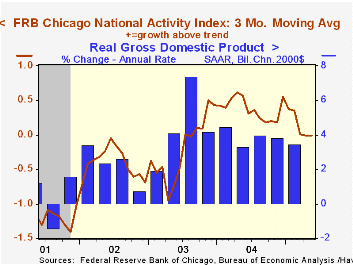

The National Activity Index (CFNAI) compiled by the Federal Reserve Bank of Chicago has improved since the low this past March and suggests that US economic growth has strengthened. Despite a dip in July to 0.16 from 0.40 in June, the [...]

The National Activity Index (CFNAI) compiled by the Federal Reserve Bank of Chicago has improved since the low this past March and suggests that US economic growth has strengthened. Despite a dip in July to 0.16 from 0.40 in June, the three-month moving average of the CFNAI improved to 0.23 versus the low near zero.

A zero value of the CFNAI indicates that the economy is expanding at its historical trend rate of growth.

The CFNAI is a weighted average of 85 indicators of economic activity. The indicators reflect activity in the following categories: production and income, the labor market, personal consumption and housing, manufacturing and trade sales, and inventories & orders.

During the last twenty years there has been a 74% correlation between the level of the CFNAI and q/q growth in real GDP.

The latest CFNAI report is available here.

| Chicago Fed | July | June | July '04 | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| CFNAI | 0.16 | 0.40 | 0.61 | 0.39 | -0.11 | -0.41 |

by Carol Stone August 19, 2005

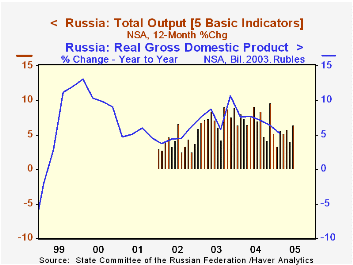

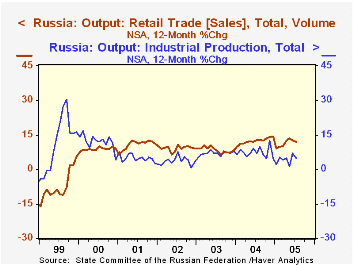

The Russian economy has maintained a firm uptrend through the summer, according to the "Five Basic Indicators", measures of output in leading goods-related sectors. In June, the combined output gauge was up 6.4% from a year earlier, stronger than May's 4.1% and last year's 5.2%. The component items for July, although not the total index, were reported this week, several of them today by the Federal Service of State Statistics, and they suggest that the momentum may have slowed somewhat. These indicators cover agriculture, industrial production, retail trade, construction and transportation. The data, contained in Haver's EMERGECW database, are not seasonally adjusted and are reported as year-on-year percentage changes. The industrial production segment gained 4.9% in July, compared with 6.9% in June and 4.6% in 2004. Retailing kept up double-digit gains, although these are a bit slower than they were during 2004. Construction and agricultural activity, by contrast, picked up considerably in July after a sluggish pace in the spring. Transportation was quite vigorous in 2002 and 2003, but has had only modest increases since then.

The volume increases in retail trade are perhaps most impressive. Russian consumers are evidently able to raise their purchasing, despite double-digit increases also in consumer prices. And since retailing is expanding so much more rapidly than industrial activity, we'd surmise that inventories are tight and that imports are continuing to flow in rapidly. Through the second quarter, total imports of goods were up 28.5% from their year earlier pace (before adjustment for inflation).

The rapid inflation makes it difficult to be unabashedly optimistic about a sustained expansion for the Russian economy, but the persisting advances in goods-producing sector output volume are encouraging. Russia's status as an oil exporter also means that rising energy costs are partially offset by the support energy sales give to incomes and profits for those employed in that sector.

| Russia: Year/Year % Changes |

July 2005 | June 2005 | May 2005 | December/December|||

|---|---|---|---|---|---|---|

| 2004 | 2003 | 2002 | ||||

| Output | -- | 6.4 | 4.1 | 5.2 | 8.9 | 3.8 |

| Industrial Production | 4.9 | 6.9 | 1.4 | 4.6 | 7.9 | 3.2 |

| Retail Trade | 11.8 | 12.5 | 13.3 | 14.2 | 8.4 | 9.2 |

| Construction | 12.9 | 7.4 | 5.3 | 10.6 | 16.6 | 3.8 |

| Transportation | 2.8 | 2.0 | 4.1 | 3.4 | 9.4 | 9.5 |

| Agriculture | 4.5 | 0.4 | 0.8 | -0.7 | 0.6 | -0.2 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief