Global| Oct 26 2009

Global| Oct 26 2009Chicago Fed Index Dipped LastMonth But Trend Level Still Rising

by:Tom Moeller

|in:Economy in Brief

Summary

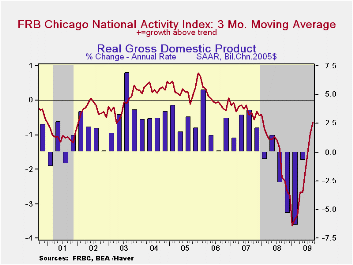

The Chicago Federal Reserve Bank indicated that while the U.S. economy had improved, growth was still below the historic trend. For September, the Chicago Fed National Activity Index (CFNAI) slipped m/m after having improved sharply [...]

The Chicago Federal Reserve

Bank indicated that while the U.S.

economy had improved, growth was still below the historic trend. For

September, the Chicago Fed National Activity Index (CFNAI) slipped m/m

after having improved sharply from the January low. The reading of

-0.90 was down from -0.56 during August yet both readings were up

sharply from the series' low of -4.13 reached this past January. Since

1970 there has been a 74% correlation between the level of the index

and the q/q change in real GDP but during the last ten years that

correlation has risen to 80%.

The Chicago Federal Reserve

Bank indicated that while the U.S.

economy had improved, growth was still below the historic trend. For

September, the Chicago Fed National Activity Index (CFNAI) slipped m/m

after having improved sharply from the January low. The reading of

-0.90 was down from -0.56 during August yet both readings were up

sharply from the series' low of -4.13 reached this past January. Since

1970 there has been a 74% correlation between the level of the index

and the q/q change in real GDP but during the last ten years that

correlation has risen to 80%.

The three-month moving average which smoothes out some of the volatility of the index improved to its highest level since June of '08.

An index level at or below -0.70 typically has indicated negative U.S. economic growth. A zero value of the CFNAI indicates that the economy is expanding at its historical trend rate of growth of roughly 3%. The complete CFNAI report is available here.

The Chicago Fed indicated that 32 of the series' individual

indicators made positive contributions to the September index while 53

made negative contributions. The CFNAI is a weighted average of 85

indicators of economic activity. The indicators reflect activity in the

following categories: production & income, the labor market,

personal consumption & housing, manufacturing & trade

sales, and inventories & orders.

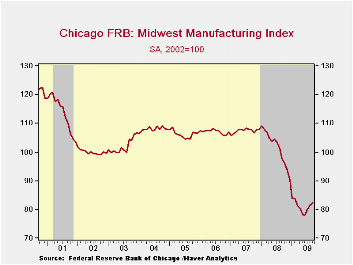

In a separate survey, the Chicago Fed indicated that its Midwest manufacturing index slipped during August but remained near its lowest since late-1993. Indicators for the steel, machinery and resource sectors improved modestly, however, that was outweighed by deterioration in the auto sector. The Chicago Federal Reserve figures are available in Haver's SURVEYS database.

International Perspective on the Crisis and Response is the title of Friday's speech by Fed Vice-Chairman Donald L. Kohn and it can be found here here

| Chicago Fed | September | August | July | August '08 | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| CFNAI | -0.90 | -0.56 | -1.82 | -2.01 | -1.77 | -0.35 | 0.05 |

| 3-Month Moving Average | -1.09 | -1.61 | -2.15 | -1.42 | -- | -- | -- |

by Tom Moeller October 26, 2009

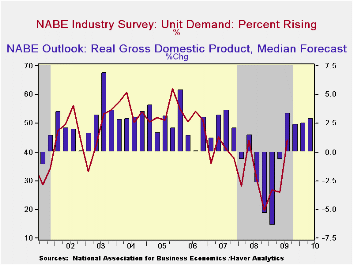

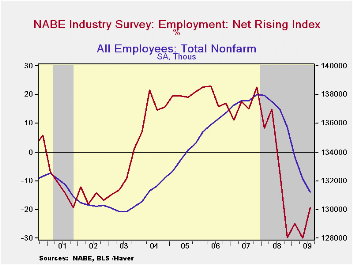

The National Association For Business Economics (NABE) indicated in its latest Industry Survey that U.S. economic conditions showed broad-based improvement during the last three months. That gain was paced by improvement in unit demand and profit margins.

The net percentage of firms reporting higher demand rose to

23.4% which was the highest level in over one year. The improvement

came as 44.2% of firms indicated higher demand but only 20.8% showed

demand falling during 3Q. That was down from nearly half reporting

lower demand at the end of last year. Overall economic growth

through the end of next year is expected to average 3%.

The net percentage of firms reporting higher demand rose to

23.4% which was the highest level in over one year. The improvement

came as 44.2% of firms indicated higher demand but only 20.8% showed

demand falling during 3Q. That was down from nearly half reporting

lower demand at the end of last year. Overall economic growth

through the end of next year is expected to average 3%.

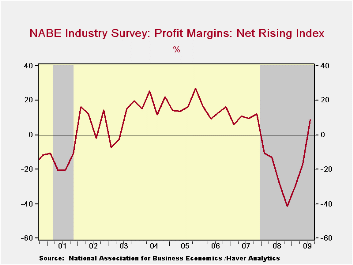

Higher net-profit margins were indicated by firms for the

first time since the fourth quarter of 2007. Thirty-six percent of

firms indicated higher margins, up from 10% during 4Q08, while a

reduced 27% reported lower margins.

Higher net-profit margins were indicated by firms for the

first time since the fourth quarter of 2007. Thirty-six percent of

firms indicated higher margins, up from 10% during 4Q08, while a

reduced 27% reported lower margins.

While still negative, net-employment improved materially as 12% of firms reported higher employment, double the low of last quarter, and a much-reduced 31% reported lower hiring.

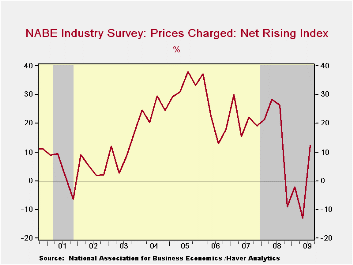

With the improvement in economic conditions, NABE indicated

that pricing power improved. The net-reading of 12% was the highest

level in one year as 23% reported higher prices and a reduced 11%

reported lower prices. Rising capital spending was indicated by firms

for the first time in one year as 26% showed higher spending while a

reduced 22% reported lower spending.

With the improvement in economic conditions, NABE indicated

that pricing power improved. The net-reading of 12% was the highest

level in one year as 23% reported higher prices and a reduced 11%

reported lower prices. Rising capital spending was indicated by firms

for the first time in one year as 26% showed higher spending while a

reduced 22% reported lower spending.

The NABE Industry Survey can be found in Haver's SURVEYS

database.

| Nat'l Assn. For Business Economics 3Q Industry Survey (Net Rising Index, %) | 3Q09 | 2Q09 | 1Q09 | 4Q08 |

|---|---|---|---|---|

| Unit Demand | 23.4 | -5.0 | -14.3 | -27.5 |

| Profit Margins | 8.7 | -17.0 | -30.4 | -41.2 |

| Employment | -19.2 | -30.0 | -25.0 | -29.8 |

| Prices Charged | 12.2 | -12.9 | -2.0 | -9.0 |

| Capital Spending | 4.2 | -23.6 | -15.8 | -26.0 |

by Robert Brusca October 26, 2009

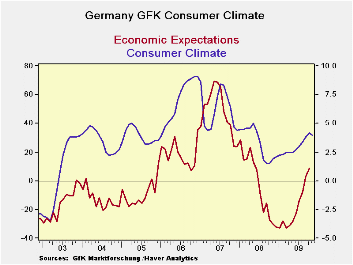

Germany’s GFK survey rose in October. It was a month-to-month

rise of 0.4 for the third month in a row. The economic index rose by

5.2 points its smallest rise since May but on the heels of a 10.9 point

spurt in September. Income expectations fell by 3.1 points, the first

drop in five months but after two large gains. The propensity to buy

dropped back by 10.4 points a huge drop and the largest since a drop of

15.7 in May 2008.

Still the Climate index at +4.2 is above its average of 3.3.

All of these components are above their average values since 2002. The

‘income’ and ‘propensity to buy’ percentiles are stronger for the count

percentiles than for the range percentiles; the standing among past

observations is stronger than their range standing between the highs

and lows. This means that while the current readings are still well off

peak they are in the upper part of the distribution of readings and in

the upper region of normal.

The GFK index shows that confidence is still improving in Germany. Germans are relatively more worried about the economy in generally than they are impacted by expectations for income or buying power problems. Still the fact of the matter is that German consumption has not been very strong. And Germany’s Chancellor is out warning that in 2011 there will be another crisis and that unemployment will rise from current levels. I guess that Obama’s pessimistic approach to assessing the economy is spreading abroad.

| Germany Consumer Climate Survey GFK | ||||

|---|---|---|---|---|

| Climate | Expectations | Propensity to | ||

| Economic | Income | Buy | ||

| Oct-09 | 4.2 | 8.7 | 12.9 | 26.1 |

| Sep-09 | 3.8 | 3.4 | 16.0 | 36.5 |

| Aug-09 | 3.4 | -7.5 | 8.8 | 31.1 |

| Jul-09 | 3.0 | -14.0 | 1.8 | 25.1 |

| Jun-09 | 2.7 | -22.6 | -3.3 | 14.5 |

| Average | 3.3 | 0.9 | -3.8 | -9.6 |

| Max | 9.1 | 69.5 | 33.6 | 64.4 |

| Min | -3.5 | -32.9 | -24.5 | -55.4 |

| % range | 61.1% | 40.6% | 64.4% | 68.0% |

| Count% | 59.6% | 66.0% | 92.6% | 87.2% |

| % range is current reading as a percentile of Hi/Low range | ||||

| Count % is current reading ranked as a %-tile among all readings | ||||

| GFK survey dates from January 2002 | ||||

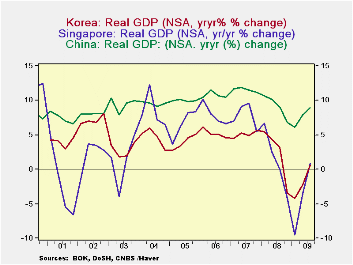

by Louise Curley October 26, 2009

South Korean

joins China and Singapore among the emerging economies of the Pacific

Rim to report third quarter GDP. GDP growth in the three

countries is shown in the first chart. The declines in the

economies of Korea and Singapore have been much more severe than those

in China. China has not experienced a year to year decline in

GDP, merely a deceleration of growth. At their low points in

the first quarter of this year, GDP in Singapore was 9.5% below the

year ago figure and GDP in Korea, 4.3% below.

South Korean

joins China and Singapore among the emerging economies of the Pacific

Rim to report third quarter GDP. GDP growth in the three

countries is shown in the first chart. The declines in the

economies of Korea and Singapore have been much more severe than those

in China. China has not experienced a year to year decline in

GDP, merely a deceleration of growth. At their low points in

the first quarter of this year, GDP in Singapore was 9.5% below the

year ago figure and GDP in Korea, 4.3% below.

Korea reported that GDP grew 2.9% in the third quarter on a seasonally adjusted basis, compared with 2.7% in the second quarter. On a seasonally unadjusted basis, GDP was 0.6% above the year ago figure, the first positive figure since the third quarter of 2008.

A swing in

inventories from a liquidation of 4,506 million won* in the

second quarter to an accumulation of 6,486 won in the third quarter was

the main factor in the third quarter strength. However, this

should not be a cause of concern at this point in the business

cycle. The rise follows three successive quarters of big

liquidations, beginning in the fourth quarter of 2008--7,290 million

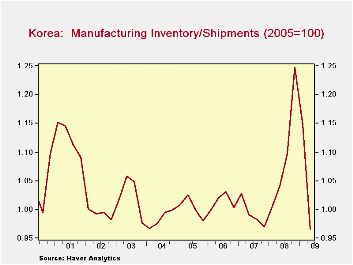

won 6,788 million won and 4,506 million wan. The inventory to

shipments ratio for manufacturing at the end of the second quarter was

.97 down from 1.25 at the end of 2008. As can be seen in the

second chart, the I/S ratio for manufacturing was somewhat below normal

at the end of the second quarter so that a build up in the third

quarter is not unexpected.

A swing in

inventories from a liquidation of 4,506 million won* in the

second quarter to an accumulation of 6,486 won in the third quarter was

the main factor in the third quarter strength. However, this

should not be a cause of concern at this point in the business

cycle. The rise follows three successive quarters of big

liquidations, beginning in the fourth quarter of 2008--7,290 million

won 6,788 million won and 4,506 million wan. The inventory to

shipments ratio for manufacturing at the end of the second quarter was

.97 down from 1.25 at the end of 2008. As can be seen in the

second chart, the I/S ratio for manufacturing was somewhat below normal

at the end of the second quarter so that a build up in the third

quarter is not unexpected.

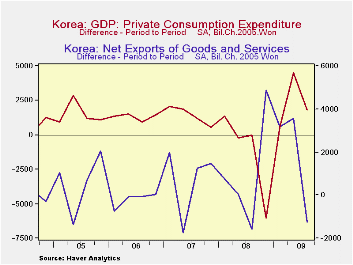

The

performance of the other components of

GDP was generally typical of that seen in the early stages of

recovery--some increases and some retrenchments. The one

notable exception was a greater decline in exports of goods and

services, than that in imports of goods and services, with the result

that the balance on goods and services declined from 20.3 billion won

in the second quarter to 19.1 billion won . In the past,

exports have been a dynamic element in the growth of the Korean economy

and generally quick to respond to improvements in the world economy.

Private consumption increased by 3,524.7 million won in the third

quarter compared with an increase of 1,367.1, this could be an sign

that Korea is beginning to shift away from its policy of export led

growth but it is probably not too wise to base a conclusion on one

quarter's evidence. See the third chart. There were small

declines in construction, fixed investment in intangible

assets and government consumption and the change in business investment

in plant and equipment was essentially unchanged at 1,778 million won

in the third quarter, compared with a rise of 1,846 million won in the

second quarter.

The

performance of the other components of

GDP was generally typical of that seen in the early stages of

recovery--some increases and some retrenchments. The one

notable exception was a greater decline in exports of goods and

services, than that in imports of goods and services, with the result

that the balance on goods and services declined from 20.3 billion won

in the second quarter to 19.1 billion won . In the past,

exports have been a dynamic element in the growth of the Korean economy

and generally quick to respond to improvements in the world economy.

Private consumption increased by 3,524.7 million won in the third

quarter compared with an increase of 1,367.1, this could be an sign

that Korea is beginning to shift away from its policy of export led

growth but it is probably not too wise to base a conclusion on one

quarter's evidence. See the third chart. There were small

declines in construction, fixed investment in intangible

assets and government consumption and the change in business investment

in plant and equipment was essentially unchanged at 1,778 million won

in the third quarter, compared with a rise of 1,846 million won in the

second quarter.

*The won in all cases is the 2005 chained won.

| SOUTH KOREA | Q3 09 | Q2 09 | Q1 09 | Q4 08 | Q3 08 | Q2 08 | Q1 08 | 2008 | 2007 |

|---|---|---|---|---|---|---|---|---|---|

| GDP | |||||||||

| Q/Q Change (SA) | 2.93 | 2.65 | 0.12 | -5.07 | 0.22 | 0.43 | 1.00 | 2.22 | 5.11 |

| Y/Y Change (NSA) | 0.58 | -2.16 | -425 | -3.40 | 3.11 | 4.35 | 5.46 | 2.22 | 5.11 |

| Change in New Exports (Mil. 2005 Chained Won) | -1263 | 3572 | 3175 | 4876 | -1590 | 48 | 756 | 10019 | 6577 |

| Change in Inventory Change " | 6487 | -4506 | -6788 | -7290 | 1396 | 467 | 2004 | 7752 | -2815 |

| Change in Private Consumption " | 3525 | 1367 | -880 | -3189 | 1648 | -3364 | -25 | 4703 | 24655 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief