Global| Dec 17 2019

Global| Dec 17 2019Car Registrations in Europe

Summary

Car registrations in Europe show somewhat mixed trends in November. Year-over-year sales are rising for three months in a row in this highly volatile and hard to seasonally adjust series. But the recent months' trends are much more [...]

Car registrations in Europe show somewhat mixed trends in November. Year-over-year sales are rising for three months in a row in this highly volatile and hard to seasonally adjust series. But the recent months' trends are much more mixed-to-weak than they are strong; the sequential growth rates also are weak. Even the year-on-year sales that are expanding for three months in a row show slipping momentum.

Car registrations in Europe show somewhat mixed trends in November. Year-over-year sales are rising for three months in a row in this highly volatile and hard to seasonally adjust series. But the recent months' trends are much more mixed-to-weak than they are strong; the sequential growth rates also are weak. Even the year-on-year sales that are expanding for three months in a row show slipping momentum.

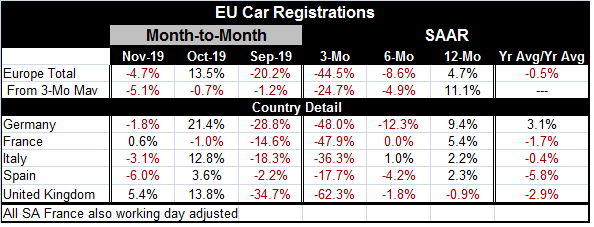

November shows declines month-to-month in overall sales as well as smoothed sales (three-month average sales compared month-to-month). Registrations fall in Germany, Italy and Spain compared to increases in France and the United Kingdom. In October, only sales in France fell, but the smoothed total for sales also fell. In September, there is widespread and severe weakens more or less across the board with aggregate sales lower by 20% month-to-month compared to a smoothed month-to-month drop of just 1.2%.

Sequential rates of growth for overall and country-by-country trends show declines across the board over three months; over six months a small gain in Italy is the only exception to that happening again. But over 12 months order is restored with gains on all measures except for the U.K. and with the smoothed measure of registrations showing a strong 11.1% rise compare to its value 12-months ago.

Trends for registrations in Europe do seem to have weakened broadly and since late-2018 in the wake of all the emission scandals registrations have clearly clung to a lower level.

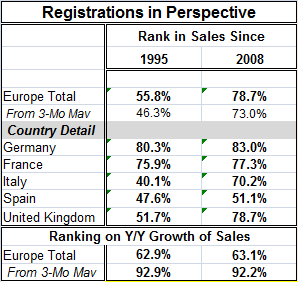

This table looks at the pace of sales (registrations) ranked since 1995 and then ranked over a shorter period since 2008. The current pace of sales is much higher when compared to more recent period than to a trend reaching back before the Great Recession. However, country-by-country we see that that is not the case. Germany shows no difference in the ranking of values back to 2008 vs. 1995. France and Spain show little difference as well. The big difference in the ranking is for sales since 2008 vs. 1995 in Italy and the U.K. Italy was hit hard by austerity and its GDP is still not back to precession levels. The U.K. is suffering from the 'brain drain' imposed on it by Brexit and the loss of a lot of financial sector and other jobs and there has been a drop in the purchase of vehicles as a result. It shows in vehicle registrations. However, the current growth rate of overall sales has the same standing when ranked against growth rates from either period.

This table looks at the pace of sales (registrations) ranked since 1995 and then ranked over a shorter period since 2008. The current pace of sales is much higher when compared to more recent period than to a trend reaching back before the Great Recession. However, country-by-country we see that that is not the case. Germany shows no difference in the ranking of values back to 2008 vs. 1995. France and Spain show little difference as well. The big difference in the ranking is for sales since 2008 vs. 1995 in Italy and the U.K. Italy was hit hard by austerity and its GDP is still not back to precession levels. The U.K. is suffering from the 'brain drain' imposed on it by Brexit and the loss of a lot of financial sector and other jobs and there has been a drop in the purchase of vehicles as a result. It shows in vehicle registrations. However, the current growth rate of overall sales has the same standing when ranked against growth rates from either period.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief