Global| Mar 21 2019

Global| Mar 21 2019Canadian Growth: Headed for the Big Sleep or Just Dozing?

Summary

Canada, like much of the global economy, is showing sales weakness across sectors with its most topical three-month and six-month sales growth rates by sector showing declines. Manufacturing shipments, retail sales - both overall and [...]

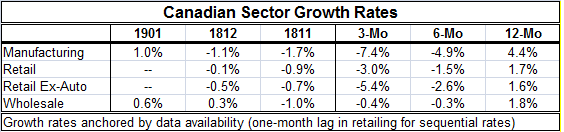

Canada, like much of the global economy, is showing sales weakness across sectors with its most topical three-month and six-month sales growth rates by sector showing declines. Manufacturing shipments, retail sales - both overall and excluding autos - as well as wholesale sales, all are falling on balance over three months and six months and the pace of the drop is intensifying.

Canada, like much of the global economy, is showing sales weakness across sectors with its most topical three-month and six-month sales growth rates by sector showing declines. Manufacturing shipments, retail sales - both overall and excluding autos - as well as wholesale sales, all are falling on balance over three months and six months and the pace of the drop is intensifying.

However, January brings some respite to these trends. Manufacturing shipments rose by 1% in January and wholesale sales rose by 0.6%. The jury is still out on retail sales that have not yet been reported.

Year-over-year trends are modest. Canadian inflation metrics generally are up by about 1.5% over 12 months. So the manufacturing gain of 4.4% leaves some real growth on the table while retailing and wholesaling seem to offer only very thin margins for real growth.

Year-on-year sector growth rates generally peaked in mid-2017 and since have been eroding. However, all three sectors show a modest bump up in the most recent 12-month growth rates compared to their penultimate ones.

A snapshot of other Canadian sectors shows that there still is some resiliency. Employment gains are still solid and have even picked up some speed recently. Mining and oil output, important Canadian sectors are on an upswing. And the unemployment rate remains at a low level. But housing starts have been weak; they are declining at a horrifically fast pace over three months. Manufacturing output barely ekes out a gain over 12 months and is now on an accelerating path of contraction. Exports are also showing an accelerating contraction with severe weakness logged over the last three months. Imports, a series that is more connected with domestic demand than with international events, show more resiliency than exports. Still, imports fall at a 2.6% annual rate over six months and rise at just a 0.5% pace over three months. Year-over-year imports are rising in step with inflation.

Canada's situation is more or less similar with that of the other G7 countries. It does not have an inflation problem. And it is having a hard time keeping growth in gear and yet economic performance has been good even if not strong. The unemployment rate is low. The problem is the turn of events in the current situation. Currently, there are mixed signals and mixed results by sector, but there is a liberal dose of weakness thrown in. Concerns about global trade overhang Canada as they do every other trading nation. The Baltic dry goods index has been showing weakness in global shipping volumes for a number of months now. Canada trades intensely with the U.S. where growth signals also have been dodgy and where the Fed has halted a program of rate hikes and just wiped the potential for rate hikes in 2019 off the slate. The U.S. yield curve is flatting voraciously again. That is never a signal that is friendly to U.S. growth. And it is ominous for Canada as well since the U.S. economy is an important trade partner and because U.S. growth has a lot to say about which way commodity prices turn and they also are important to Canada's economy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief