Global| Jul 22 2019

Global| Jul 22 2019Canada's Sector Sales Show Weakness in May But Demonstrate Improvement More Broadly

Summary

With the release of wholesale sales, we can look at and compare Canadian sector growth rates. Manufacturing sales were up strongly in May, but overall retailing, retail ex-autos and wholesale sales all declined. Wholesale sales fell [...]

With the release of wholesale sales, we can look at and compare Canadian sector growth rates. Manufacturing sales were up strongly in May, but overall retailing, retail ex-autos and wholesale sales all declined. Wholesale sales fell hard in May.

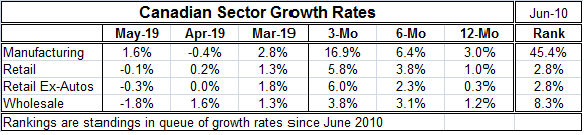

With the release of wholesale sales, we can look at and compare Canadian sector growth rates. Manufacturing sales were up strongly in May, but overall retailing, retail ex-autos and wholesale sales all declined. Wholesale sales fell hard in May.

Despite the May weakness and despite low year-on-year growth for all sectors, all sectors show steady growth accelerating from 12-months to six-months to three-months. Manufacturing sales show the strongest acceleration with a three-month gain at a very strong 16.9% annual rate; still, year-on-year gain is just 3%. Also given Canada’s strong business cycle linkage to the U.S. where conditions have slowed and are slowing down - and also given global conditions that have clearly been weakening - a Canadian manufacturing acceleration that had legs here would be a surprise.

Canadian industrial production trends show manufacturing output decelerating. There is strength where you would expect it, in this environment in mining, oil and gas extraction where growth rates have accelerated sharply to a 26.6% annual rate over three months. This sector’s need for inputs may be exerting a real tug up on manufacturing as the extractive sector does require special machinery, pipes and other manufactured goods. However, outside that strength there is weakness in Canadian utilities output as well as ongoing declines in construction. The extractive sector is not a rising tide that will lift all boats.

Looking at the current year-on-year growth rates as a queue of growth rates since mid-2010, we find all major sectors ranked below their respective median rates of growth (for rankings median occurs at a ranking of 50%). Still, manufacturing is the relative strongest sector as its 3% growth rate is in the 45th queue percentile, leaving it just a handful of percentile points below its median. But retailing, retail ex-autos and wholesaling all show extremely weak rankings. All of them lie somewhere in the lower 10th percentile of their respective queues of results. Retail and retail ex-auto sales have been weaker less than 3% of the time since mid-2010. Wholesaling shows sales have been weaker only about 8.3% of the time over that same period.

While the Canadian extractive sector- an important sector in Canada- is doing well, the overall sector results show weakening across sectors and moderation turning to weakness in manufacturing.

Globally, we still have growth. Today the National Institute of Economic and Social Research (NIESR) in the U.K. raised the question of whether the U.K. was in a recession yet as it sees encroaching weakness and believes that the transition to Brexit will eventually put the U.K. economy in recession if it isn’t there yet. China has slowed, but it still generates growth rates that would be enviable elsewhere in the world. In the U.S., the probability of recession models are ringing up gains on that eventuality- but U.S. growth just as it looks like it is about to fade seems to rebound strongly and unexpectedly either in the job market or in an unanticipated industrial gauge. Whatever the risks in the U.S. economy, it is still growing now. Canada’s slump seems to be home-grown despite a vibrant extractive sector. However, all is not negative in Canada. Despite the weakness in May, longer trends are on the rise. That result may prove too fragile to endure. But for now Canadian data are sending an unequivocally mixed message.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief