Global| Mar 27 2019

Global| Mar 27 2019Canada Posts Second Largest Trade Deficit Ever

Summary

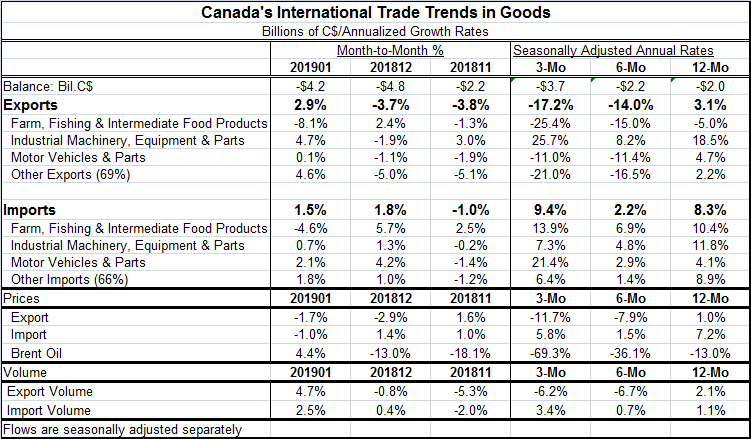

The stalactites on the chart tell a tale of Canada flirting with some very large deficits for some time, through 2016 and into 2017. After a short hiatus, the deficit erosion seems to be back. While exports and imports both rose in [...]

The stalactites on the chart tell a tale of Canada flirting with some very large deficits for some time, through 2016 and into 2017. After a short hiatus, the deficit erosion seems to be back. While exports and imports both rose in January and exports rose more than imports, the trends for exports and imports remain unfavorable to Canada's trade condition. Exports have been slowing from a 3.1% pace over 12 months to an annual rate of -14% over six months to an annualized pace of -17.2% over three months. This progressive deterioration has deep roots in trends for farming and fishing exports, industrial machinery exports, motor vehicles & parts exports as well as all other exports. None of these trends are Canadian ‘friends.'

The stalactites on the chart tell a tale of Canada flirting with some very large deficits for some time, through 2016 and into 2017. After a short hiatus, the deficit erosion seems to be back. While exports and imports both rose in January and exports rose more than imports, the trends for exports and imports remain unfavorable to Canada's trade condition. Exports have been slowing from a 3.1% pace over 12 months to an annual rate of -14% over six months to an annualized pace of -17.2% over three months. This progressive deterioration has deep roots in trends for farming and fishing exports, industrial machinery exports, motor vehicles & parts exports as well as all other exports. None of these trends are Canadian ‘friends.'

Imports per se are less of a problem. They do not show adverse trends, but rather they hew to various complicated patterns that result in import growth remaining positive and elevated so that export weakness interacts with import growth to balloon the deficit.

Canada's trade deficit grew to $4.8 billions (Canadian dollars) in December and then stepped back only to a $4.2 billion deficit in January. The average deficit is -$2.0 billions over 12 months, -$2.2 billions over six months and -$3.7 billions over three months. The clear deterioration in average deficits is the mark of true erosion trend.

Canada is an exporter of a good deal of commodities and natural resource products. It also has a deal on trade with the U.S. so that there is a vibrant trade in autos and parts between Canada and the United States. Auto trade has set patterns than are deficit raising as exports are slipping and imports are generally accelerating for auto trade. But the more compelling problem is the weakness in global commodity prices that hits Canada hard across a range of products.

Canadian export prices are up by 1% over 12 months and falling at a 7.9% annual rate over six months then falling at an 11.7% rate over three months. Falling export prices take a quick toll on the growth in export value. Typically when a country has weak or falling export prices, we expect that will aid its competitiveness and may actually lay the basis for an export rebound down the road. But since Canada exports a lot of commodities, export price weakness is less likely related to any ‘gain in competitiveness' and more likely the result of a weakening in demand for commodities globally. And we are in the grip of a global economic slump of some degree. This means there is no real silver lining for Canada's export price weakness. And over 12-months to six-months to three-months, oil prices have been collapsing.

At the same time, Canadian import prices are more or less stable without a clear pattern. Import prices are up by 7.2% (much more than export prices) over 12 months and rising at a slower but still quite firm 5.8% annual rate over three months.

We can use the price series to deflate the value series and create a volume series for exports and imports. The results expressed in volume terms reinforce Canada's deteriorating trade trends. Export volume slows from a 2.1% gain over 12 months to a 6.2% annualized pace of decline over three months. Import volume accelerates from a 1.1% gain over 12 months to a 3.4% annual rate rise over three months.

On balance, both price and volume trends act to widen Canada's trade deficit. And while domestic demand still seems strong enough to suck in imports, global trade and growth has been slowing. That slowing is not only a trend problem for domestic vs. ‘foreign' demand but also a factor that has acted to depress commodity prices and to pressure lower the prices of Canadian exports. More specifically, the U.S., Canada's major trading partner, is slowing as well. There is a lively debate about how much U.S. demand actually has slowed. But the U.S. is also part of the trend that has nagged at Canadian trade trends and these trends seem destined to make Canada's trade deficit even worse in the future.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief