Global| Aug 28 2013

Global| Aug 28 2013Brussels...We Have A Problem

Summary

Apollo 17? The understated words that informed the world of the serious risk that the US space mission called `Apollo 13' faced came with the simple phrase, "Houston, we have a problem." Unfortunately, no one in Europe is telling [...]

Apollo 17? The understated words that informed the world of the serious risk that the US space mission called `Apollo 13' faced came with the simple phrase, "Houston, we have a problem." Unfortunately, no one in Europe is telling Brussels that it has a problem and one of similar dimension. As in the United States, the central bank, the European Central Bank, has taken the lead to do what it can to bridge the gaps in Europe. But, it's attempting that feat with a charter and a mandate that is far narrower and more constricting than that of the Federal Reserve in the United States. I'm not lamenting this restriction as much as I am simply pointing it out.

Apollo 17? The understated words that informed the world of the serious risk that the US space mission called `Apollo 13' faced came with the simple phrase, "Houston, we have a problem." Unfortunately, no one in Europe is telling Brussels that it has a problem and one of similar dimension. As in the United States, the central bank, the European Central Bank, has taken the lead to do what it can to bridge the gaps in Europe. But, it's attempting that feat with a charter and a mandate that is far narrower and more constricting than that of the Federal Reserve in the United States. I'm not lamenting this restriction as much as I am simply pointing it out.

Both the glue and the cheese are binding: Europe, as much is the United States, if not more so, needs fiscal policy to help it dig out of the deep hole it's in. The nations that have bound themselves together in this arrangement that we call the European Monetary Union need to either strengthen the glue that binds them together or dissolve it altogether. The glue will either be their salvation or their downfall. That much is clear. The solution is not to profess even more belief in the strength of this binding agent (the single currency system) but to give that glue (system) more support. After all, the risk when you glue things together is that a break will occur at the point that the two pieces (or seventeen pieces) are joined - not in the middle of one of them.

The cellophane and staples central bank of Europe: Reaffirming that each country meet some specific fiscal solution is not as likely a remedy as one that offers further fiscal support that spans the pieces that are so glued together, reinforcing the connection. Yet- so far - there is no taste for more loss of national sovereignty, a necessary ingredient for a Zone-wide fiscal union of some sort. What the central bank has been doing amounts to the way my mother used to fix things, with her favorite tools being cellophane-tape and a stapler. That might have been suitable for a very short term fix of an unraveled hem, but it's an arrangement that would be in need of being repeated again and again and that eventually will need more permanent attention. Can Europe rise above the use of cellophane-tape and staples?

Celebrating symptoms while the disease runs wild: Currently, Europe and the rest of the world are celebrating the day-by-day and month-by-month release of somewhat improved economic statistics in the Monetary Union. However, let's remember that people who die often `rally' and improve, finding a special moment of clarity before they relapse and expire. What Europe is doing, is a bit like celebrating each time you paint a new room of your house to make it look better even as the termites are eating their way through your building's foundation. The foundation - the very basis of European growth - is flawed it's incomplete and it still is crumbling. Thinking you can `remodel' or build something solid on top of it is pure folly. What we see in the release of the new money and credit data is that on the monetary side, the unraveling has already begun. Monetary policy that has been the cellophane-tape and staples that have held the union together so far is seeing that its holding power is diminishing.

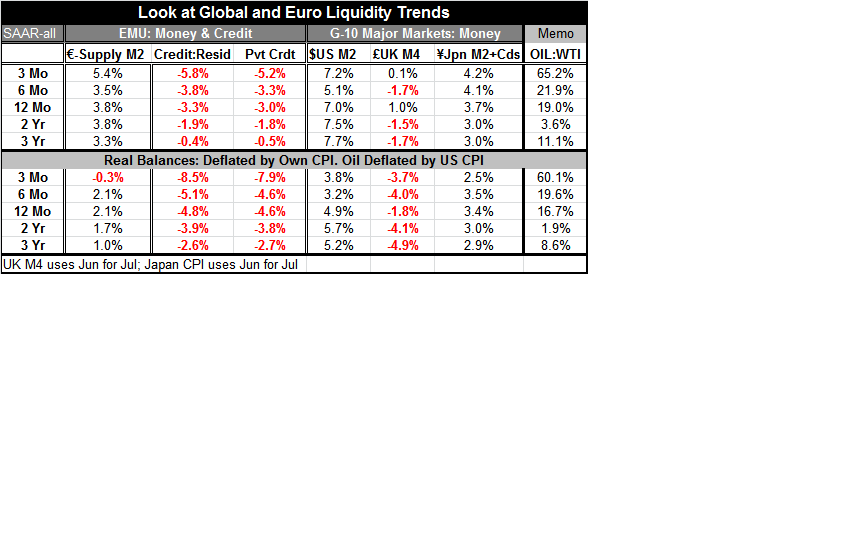

Money, money, money: Money supply growth in the European Monetary Union has been gradually increasing in the wake of the financial crisis, from a low point of about 1% year-over-year in May 2010, to a peak rate of 4.8% in April 2013. As of July 2013 that year-over-year growth rate is down to 3.8%. Of course, hairsplitting on an annual growth rate that's declined by only one percentage point over three months is hardly decisive - and that is really not the real point.

ECB not equal European Credit Bank! The real point is that credit growth in the Eurozone is calling the tune and it is not just `still declining' but its decline is accelerating and it is now pulling money growth into its descending orbit. The real problem is that `ECB' does not stand for European Credit Bank and that money is not credit.

Credit leads money not vice-versa: Euro-credit growth bottomed prior to the bottoming of money growth. Growth in total private credit growth as well as total credit bottomed in October 2009 ahead of the May 2010 bottoming in money growth. Credit growth then began to accelerate. Credit growth reached a peak in February 2011 and held its growth rate in the neighborhood of 3%, or just below that, until September 2011. Then credit growth fell off that growth rate plateau with both total and private credit growth, falling off fairly steadily. Thus from late 2011 onward there has been a clear schism between money growth and credit growth. Credit growth has continued to decelerate while money growth had continued to accelerate - until just the last three months. And that is what is significant.

Halloween come early for Europe? Trick or trick? And so this is the issue. It's not just that the one percentage point change in the growth rate of money supply is by itself so significant. Clearly it isn't. But what is significant, is that the ongoing and deepening weakness, the intensifying deceleration, in total credit growth and in private credit growth in the European Monetary Union seems finally to have taken its toll on money growth. No longer do we look at these series, one for money, the other for credit, see the divergence, and marvel at something that's not supposed to happen. Instead, we should be struck by the horror of what is actually happening and what it means for Europe.

Giving money credit or does credit give life to money? Economists have long had a debate about whether it was money or credit that's most important. Although a single episode is never going to change anyone's mind (and in the case of economists, maybe no information whatsoever will ever change their mind) the evidence in this cycle in the US as well as in Europe is that credit is more important than money. At the least, that is so in this cycle.

Credit clamp or liquidity trap? While Keynes was the one who introduced the idea of a liquidity trap, the idea that some point could be reached in which people would simply continue to hold more money rather than spend it, the evidence suggests that we observe such a phenomenon today because either banks will not extend credit or because people will not take it under the circumstance in which it's offered. In short, the suggestion here is that it's a credit clamp not a liquidity trap or that the appearance of a liquidity trap is an illusion created by the credit clamp. Nothing up my sleeve.

The money creation process is a credit creation process: In the case of the US, and the Fed's eventual adoption of quantitative easing, we see a clear example of extraordinarily liquid bank reserves. and a huge decoupling of reserve growth compared to money supply growth as measured by either M1 or M2 - or any other aggregate you care to construct. Thus the problem is that the `money multiplier' is broken. Banks have huge excess reserves and do not make new loans so (1) new loan balances are not drawn by borrowers and re-deposited in the banking system (2) banks do not keep a fraction of the new deposit (which they do not get) for reserve maintenance (3) the remainder of the funds are not relent to the public, triggering a repeat of that process and, (4) therefore, nothing is fueling money OR credit growth. Note that it all begins - or in this case it fails to begin - because of an unwillingness to expand credit. In other words when we say that the `money multiplier' is broken what we are saying is that the credit process is broken. It's credit that's not being extended and therefore money that's not being created. Credit is the problem, money is result. That credit is the problem is even clearer when you notice that it's bank reserves that are overflowing- extraordinary levels of `excess' bank reserves - and represent `not lending' as clearly as any measure you could desire.

Hope springs infernal? Similarly in Europe what we've seen is that the expansion of money supply has not been sufficient to restart the credit process which has been in decline, a decline that the European Central Bank had hoped only involved reversible retrograde motion. Nevermore.

The Potemkin party: So while Europeans are pleased about the improvement of some of the recent economic statistics, what we see under the surface is that credit still is not expanding. Banks in Europe are still very wary. The new Basel rules are going to make bank leverage even more difficult and will require banks to carry even more high-grade capital at a time when high-grade capital is even harder to come by. In this environment, what is high-grade capital? Is it government bonds? Is that true in Greece, in Spain and in Portugal. as well as in Germany?

The clothes make the man: Banks have had enough problems, and in fact they still have issues festering under the thin scab of widely used accounting rules. No bank, either in Europe or in United States, would want to subject its entire balance sheet to mark-to-market accounting - nor should it. However, that statement reflects the fact that banks are still carrying at artificial valuations for a large amount of badly priced assets left over from the financial crisis. And yet many these institutions still are paying nice bonuses to their people and operating as though all is well.

Hello, darkness, my old friend: If ever we were to look at the performance of an economy and to hear the sound of thin ice cracking while it continued to `grow' and celebrate on that thin surface, it is Europe today. Unemployment rates in Europe are too high. Youth unemployment is staggering. The divergence is in the performance among European economies is both stunning an unsustainable. Debt levels are constricting. How can growth flourish if the fiscal clamp is engaged and if BIS leverage rules require less leverage and more capital at the same time? About the only thing that Europe can agree upon is that its new anthem is bound to be Simon and Garfunkel's, "The Sounds of Silence".

The next euro- appointment? Disappointment! The money and credit developments in Europe are telling. Given its very difficult economic circumstances it's very hard to see how the European recovery can manage escape velocity with credit decelerating at an ever faster pace. The erosion of money growth is just one example of this. Europe is in a very thick soup, and that might be the only nourishing thing it has for quite some time. Do not join in with the folly of euro-enthusiasm. You are bound to be disappointed.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief