Global| Oct 04 2019

Global| Oct 04 2019British Chambers of Commerce Survey Weakens

Summary

The British Chambers of Commerce (BCC) quarterly economic survey shows weakness in both manufacturing and services with manufacturing leading the way lower as was expected to with trade as the likely active operational factor. But is [...]

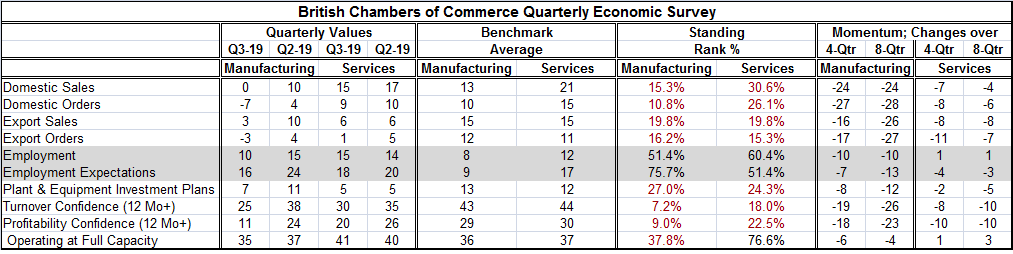

The British Chambers of Commerce (BCC) quarterly economic survey shows weakness in both manufacturing and services with manufacturing leading the way lower as was expected to with trade as the likely active operational factor. But is trade the reason for it or not? It looks like 'not.' Of course, trade and manufacturing weakness is a global theme that stems from the U.S.-China trade war and its fallout. But the U.K. has its own special negative as it careens toward Brexit with no clear plan and no sense of that the endgame will be or when it will be played despite Boris Johnson trying to create his own version of certainty. On that score, manufacturing and services, while declining at different speeds on the momentum measure, are at highly similar standings on the percentile measures.

The British Chambers of Commerce (BCC) quarterly economic survey shows weakness in both manufacturing and services with manufacturing leading the way lower as was expected to with trade as the likely active operational factor. But is trade the reason for it or not? It looks like 'not.' Of course, trade and manufacturing weakness is a global theme that stems from the U.S.-China trade war and its fallout. But the U.K. has its own special negative as it careens toward Brexit with no clear plan and no sense of that the endgame will be or when it will be played despite Boris Johnson trying to create his own version of certainty. On that score, manufacturing and services, while declining at different speeds on the momentum measure, are at highly similar standings on the percentile measures.

Services have a higher operating capacity than manufacturing and that probably accounts for the somewhat stronger services standing across the evaluation metrics in the table. The labor market evaluation lags and for both services and manufacturing the standings are still above their respective medians (above 50%).

Current sales and orders have weakened standings; they are in the 10-15 percentile angle for manufacturing and the 25-30 percentile range for services.

Export sales and orders are similarly weak for manufacturing and for services in the 15-20 percentile range. Plant and equipment investment plans have slipped in both manufacturing and services to the 25-30 percentile range. Sales and profit confidence are both extremely weak and weaker for manufacturing.

Momentum over the past four and eight quarters shows that there has been a much faster deterioration in manufacturing than in services. In fact, the pattern of weakness spread across manufacturing and services in the recent four quarters has a correlation of 0.66 and an R-squared value of 0.44. That means that they share about 44% of the same sorts of dislocations. Interestingly, export sales and orders have not been as dislocated as domestic sales and orders, a suggestion that the U.K. is suffering more from the ills of Brexit than from the same global trade disease as the rest of the global economy. In fact, if we look at the dislocation rankings across four quarters eight quarters and 12 quarters for services and for manufacturing, the correlations are quite similar for each period and relatively high, with more dislocation consistently registered in the domestic measures implying that the two sectors are reacting to the same shock and that it is internal. For manufacturing the greater part of that shock comes more consistently from domestic sources than from trade-related sources while for services the international shock is not that much different from the domestic shock.

Brexit continues to be a huge factor dogging the British economy. The Irish backstop is absolutely haunting the 'leavers' and getting in the way of their ability to use Brexit to achieve the freedom from the EU they have sought from Brexit all along. Boris Johnson and his like-minded cohorts undermined each and every effort of Theresa May and now they find that they are not able to do any better than she did. Only recently does Mr. Johnson show any sign of realizing that his Halloween date with destiny will wind up only haunting him and his own political career. He has already admitted that some sort of border check will be required for Ireland and also he has (apparently) come to terms with the prospect that he can no longer credibly talk of leaving under any circumstances by Halloween. While he continues to look for a different backstop solution, he is ready to extend Brexit in the event that a suitable backstop cannot be found by mid-month or so. Welcome to reality Mr. Johnson. So now you know what all this economic dislocation is about. It is about the failure to deliver the Brexit that was promised and the dislocation that will be created without the freedom to purse a truly new course, as was promised. It is looking more like Brexit was really sold on false pretext. And if people had known the true Brexit choices, they probably would have defeated it. Instead, they have Boris and the Brexit boys looking to somehow patch up their dream that has turned to a nightmare- and not one on Elm Street. Happy Halloween everyone.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief