Global| Oct 09 2019

Global| Oct 09 2019BOF Survey Weakens

Summary

The BoF survey indicator fell to 96.0 in September from 98.9 in August. With the survey in hand, the Bank of France is looking for Q3 GDP to gain 0.3%, the same as its previous estimate. However, the survey indicator has only a 27th [...]

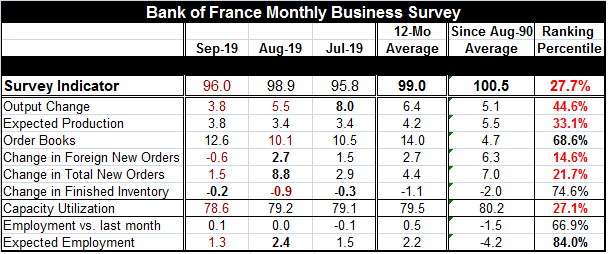

The BoF survey indicator fell to 96.0 in September from 98.9 in August. With the survey in hand, the Bank of France is looking for Q3 GDP to gain 0.3%, the same as its previous estimate. However, the survey indicator has only a 27th percentile standing. It resides close to the lower 25 percentile of its queue of statistics since August 1990, a weak showing. The average of the Q3 (96.9) survey is well within the value parameters for the BoF to hold its Q3 growth estimate at 0.3%.

The BoF survey indicator fell to 96.0 in September from 98.9 in August. With the survey in hand, the Bank of France is looking for Q3 GDP to gain 0.3%, the same as its previous estimate. However, the survey indicator has only a 27th percentile standing. It resides close to the lower 25 percentile of its queue of statistics since August 1990, a weak showing. The average of the Q3 (96.9) survey is well within the value parameters for the BoF to hold its Q3 growth estimate at 0.3%.

The output change fell to 3.8 in September from 5.5 in August, putting it well below its 12-month average gain as well as its average gain since August 1990. The output change has a 44.6 percentile standing, well below its median (for all queue rankings the median is at a ranking of 50%).

Looking ahead, expected production also has a value of 3.8, but that reading is a gain from August for the outlook but still below its 12-month average. Expected production has a 33rd percentile standing.

The order book reading has also advanced from its August level, rising to 12.6 from 10.1. Despite this pick up, the reading is still below its 12-month average but well above its long-term average and at a 68th percentile standing, in the top two-thirds of its historic range. Order books remain healthy.

The change in foreign new orders shows a negative reading of -0.6, a sharp deterioration from one month ago. The average change over 12 months is 2.7, well below the average change over the full sample. In fact, the current reading is extremely weak at a 14th percentile standing. While order books are healthy, French new foreign orders are weak.

The change in total new orders is slightly better with a 21st percentile standing. That change was at a positive 1.5 in September, down very sharply from 8.8 in August. The slight improvement in the overall order standing suggests a bit better performance by domestic orders. But there is a sharp order deceleration in place month-to-month.

Employment edged slightly higher month-to-month at a pace below its 12-month average and above its long-term average. As a result, the employment ranking is at its 66th percentile standing in the top one third of its historic queue of data. The standing for expected employment is even stronger with an 84th percentile standing. However, expected employment softened slightly month-to-month, falling to a 1.3 reading and is below its 12-month average. In sum, employment expectations are still quite good, but that perception is losing some momentum.

Finished inventory changes continue negative in September but at a slower pace than in August. Inventories have been at a greater pace of correction over the past 12 months. Despite its negative value, the August reading has a relatively high 74th percentile standing.

With the French survey showing some weakness, but still pointing to steady GDP growth ahead, Finance Minister Bruno Le Maire said that the trade war between the United States and China could cut global growth by 0.5 points next year. La Maire has joined his voice to those looking to get China and the U.S. to end their growth-reducing stand-off.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief