Global| Mar 14 2008

Global| Mar 14 2008BoF Indicator Continues to be Weak

Summary

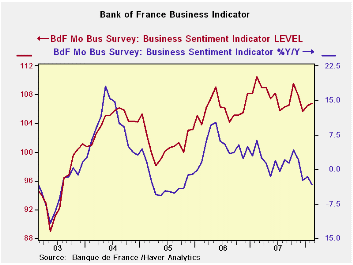

The Bank of France has put the logical spin on its survey as showing that growth continues. After a marked slowdown in French GDP growth in 4Q, the new BoF survey shows that activity has picked up somewhat, although the Industry [...]

The Bank of France has put the logical spin on its survey as showing that growth continues.

After a marked slowdown in French GDP growth in 4Q, the new BoF survey shows that activity has picked up somewhat, although the Industry sentiment index is still below its 12-month average.On the basis of its February business survey, the central bank actually has revised down its projection for Q1 GDP growth to 0.4% from the 0.5% it initially forecast. This is just below the December forecast of the national statistics institute Insee and just above the 0.3% gain in 4Q.

Industry output continued to expand in February but less strongly than in January, to say the least. The February reading for production is 4.55 compared to 19.17 for January and a 12-month average of +7. Weaker gains were reported in most sectors. Autos posted an outright decline in February after a spike in January and a decline in the auto output in December. Manufacturing capacity utilization slipped to 83.4% after a rebound in January to 83.5%, remaining above the long-term average of 83 since 1987 but below the average of 84 for the last 12 months.

Executives said new domestic orders slowed in February and overall order books were somewhat lighter, in fact at 8.76 they are below the 12-month average for orders and below the long-term average of 9.

Growth also slowed in most segments of the services sector in February.

Activity is expected to continue to expand in most branches but at a more moderate pace. Foreign orders gains were much weaker in February, as the euro climbed. Importantly, service providers indicated that price hikes would be slightly less rapid in the months ahead. Cleary the BoF has put some positive spin on the report in which growth is indicated but momentum seems to be fading.

Going back to 1987 the semi-finished goods sector is in dire straits with the lowest production outlook and lowest new orders it has ever seen. Production in this sector is in the bottom 16 percent of the range for orders in the past 30 years. Auto sector production is in the bottom third of its range as is the agriculture and food sector; consumer goods production is in the bottom 42 percent of its range. The production outlook for capital goods and consumer goods is the lower 36th percentile and lower 15th percentile of their respective ranges. This report is really very weak.

| Bank of France Monthly INDUSTRY Survey: SUMMARY | ||||||

|---|---|---|---|---|---|---|

| 12 MO | Since Jan-87 | 2Yr Percentile | ||||

| Feb-08 | Jan-08 | Dec-07 | AVERAGE | Average | rank/range | |

| Production-latest mo | ||||||

| Total Industry | 5.44 | 19.17 | -4.13 | 7 | 7 | 32.5% |

| Production Outlook | ||||||

| Total Industry | 12.91 | 15.86 | 22.21 | 16 | 15 | 29.4% |

| Demand | ||||||

| Overall order books | 22.81 | 24.85 | 25.33 | 27 | 4 | 39.7% |

| Foreign Orders | 10.24 | 10.87 | 8.89 | 11 | 9 | 27.0% |

| New Orders | ||||||

| Total Industry | 8.76 | 12.28 | 9.3 | 10 | 9 | 18.9% |

| Stocks: Finished Gds | ||||||

| Total Industry | -3.76 | -1.88 | -4.76 | -3 | -2 | 22.1% |

| Capacity Utilization | 83.35 | 83.48 | 80.86 | 84 | 83 | 57.2% |

| Hiring | ||||||

| Latest Mo | 0.41 | 2.74 | -1.43 | 0 | -1 | 74.8% |

| Outlook | -0.44 | -1.48 | -0.67 | -2 | -4 | 88.5% |

| Industry Sentiment Index | 106.8 | 106.47 | 105.68 | 107 | 107 | 48.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief