Global| Apr 11 2018

Global| Apr 11 2018Bank of France Business Survey Sees Weaker Future But There Are Even Deeper Problems

Summary

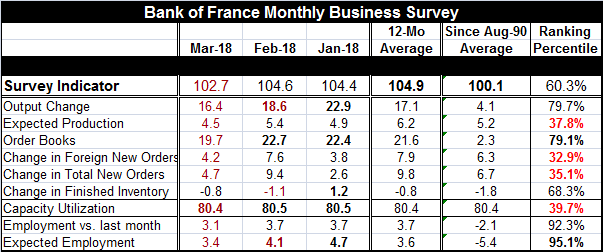

The Bank of France business survey stepped down to a reading of 102.7 in March from 104.6 in February. The reading is the weakest since the survey barometer logged 101.9 in January 2017, a bit more than one year ago. Since then the [...]

The Bank of France business survey stepped down to a reading of 102.7 in March from 104.6 in February. The reading is the weakest since the survey barometer logged 101.9 in January 2017, a bit more than one year ago. Since then the survey peaked at a level of 107.1 in December and now is engaged in a downward drift.

The Bank of France business survey stepped down to a reading of 102.7 in March from 104.6 in February. The reading is the weakest since the survey barometer logged 101.9 in January 2017, a bit more than one year ago. Since then the survey peaked at a level of 107.1 in December and now is engaged in a downward drift.

Weaker GDP is a’ comin’

The Bank of France uses this survey to gauge what GDP is expected to do in the upcoming quarter. Based on the new survey readings the Bank of France now expects Q1 2018 GDP to rise by 0.3%, a downward revision compared to its previous projection of 0.4%.

The BOF survey is in line with other indicators, notably the Markit PMI gauges, that have been backtracking in Q1.

Elsewhere, in the U.K., the National Institute of Economic and Social Research (NIESR) has estimated a step down to a 0.2% gain for Q1 U.K. GDP growth. That is a reduction from a gain of 0.4% in Q4 2017 as U.K. manufacturing production fell in February.

BOF Survey Components

All of the readings in the BOF survey have weakened in March compared to February except the change in finished inventories; that number still shows an inventory drop, but a smaller drop than the one logged in February.

The queue percentile standings for the BOF survey show the overall barometer at a 60.3 percentile standing, a moderate and positive reading. Recall that the median reading for all the queue standings occurs at a reading standing of 50%.

Four component readings in the March survey are below their respective medians; they are for (1) expected production, (2) change in foreign new orders, (3) change in total new orders, and (4) the level of capacity utilization.

The strongest readings are for the job market gauges. ‘Employment vs. last month’ has a weaker reading month-to-month, of course, but still has a standing in its 92nd percentile. ‘Expected employment,’ despite its monthly erosion, still has a 95th percentile standing. Labor market gauges tend to be either contemporaneous or lagging. So this is a problem since the forward-looking readings in this survey are among the weakest and the current-to-lagging indicators are among the strongest. The current output change and order books each have a relatively firmer 79th percentile standing. Finished inventories have a 68th percentile standing.

We can further assess the survey levels in March by comparing them with their historic averages. On that basis, we get below average readings in March from the same categories that are below their respective medians with the exception that capacity utilization is at its average value in March.

The slowdown in France is not remarkable in any way. But these numbers post a month before the national railway strike has gone into effect to protest President Macron’s labor market modernization program. The French are notorious for resisting changes in social and labor market conditions. It is remarkable given this reluctance –and willingness to strike- how closely France has been able to keep its inflation rate tracking Germany’s since its people resist changes that streamline the economy that often mean taking perks and pay away from workers.

France is caught between a rock and hard place over reform/no reform. In Hungary, the newly elected head of state has taken his mandate as meaning that his people envision a united Europe of separate states instead of a united states of Europe. Of course, the U.K. is being ejected from the EU because its people voted out, and they did that because of intrusive rules on immigration; the same bug-a-boo they have in Hungary. Italy and Greece already are absorbing immigrants so fast that it will change their national demographics significantly if the immigrants continue to pile in and stay. Meanwhile, the rest of Europe seems to be not eager to deal with the issues that are deep problems for some members, notably border members, and will become deeper problems for them should they choose to share the burden.

Out damn spot!

Europe seems focused on expelling the U.K. and carving up its former fiefdom within EMU among surviving members. It is also setting a significant new fence between the U.K. and EMU. Given that the people of the U.K. largely have the same gripes as many of the people in the EU maybe, the EU should be not-so-fast to act on the U.K. vote and separation? Maybe it should deal with the issue that the U.K. voters did not like and that much of the remaining EU populace does not like? With the other problems swirling around Europe, in the Middle East, and with Russia ‘acting up’ in the Ukraine and around the Baltics, Europe could find a closer relationship with the militarily adept U.K. quite useful. France’s reluctance to deal with change is a particular example of how Europe responds to new circumstances. If the U.S. does pull out of Syria, something we now know that U.S. President Donald Trump wants to do, will the influx of immigrants from the Middle East to the EU increase? If migration spurts…then what? Who will ultimately absorb it? Not I said the little red hen…

Getting a Grip

I don’t see how ignoring long-term problems and issues that divide EU members can possibly be productive. Quite apart from weakening growth in Europe, there is a lot of political unrest. Germany is still headed by Angela Merkel, but her powers have been diluted. Italy’s five star movement made great election headway, but Italy has had a hard time forming a government. In the U.K., Prime Minister Theresa May is still weathering the post Brexit storm. And while Emmanuel Macron won his election handily in France, he is finding his agenda is much less popular. Europe has more than just fading economic growth to come to grips with. Can it come to terms with itself and confront its own contradictions?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief