Global| Jan 29 2010

Global| Jan 29 2010Ain’t No Sunshine When It's Gone…Money Growth

Summary

Tight money isn’t funny – With the Fed’s balance sheet bloated like glutton at a roman feast, tensions have run high on the prospects of inflation. Like Mr Creosote in the Monty Python skit everyone is sure that with the equivalent of [...]

Tight money isn’t funny – With the Fed’s balance sheet bloated like glutton at a roman feast, tensions have run high on the prospects of inflation. Like Mr Creosote in the Monty Python skit everyone is sure that with the equivalent of just one wafer thin mint the whole mess will explode in a frenzy of inflation forces…. Meanwhile, back at the ranch where reality rules the roost, money supply growth rates among the world’s key industrial country aggregates is tempered, steady or falling. At the same time a rise in oil prices has given the appearance of inflation. Europe in December has just reported out its fastest rise in the CPI (HICP) in nearly one year. But Japan has posted the largest drop in inflation in the history of its CPI series that began in 1970 (a drop 1.2% in the month).

I would hope that after the last business cycle in which oil traded up nearly to $150/bbl and yet core inflation in the US and in Europe remained ‘restrained’ was a lesson to not spend so much time looking at headline inflation. Still, headline inflation has its advocates. They must be the same people who love to watch the action on those bobble-headed dolls sitting on the dashboard of a car as it travels over a bumpy road. There is not much else to commend headline inflation-watching.

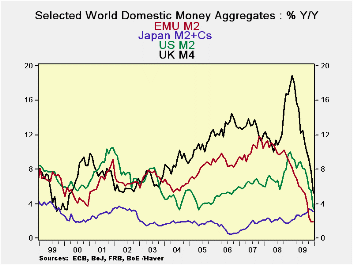

Money supply, the key driver of inflation over the long haul, is not flashing any warning signals about inflation. It is giving no reason to have inflation concerns alt all. Money supply growth in the UK, in EMU and in the US has dropped its growth rate dramatically and steadily. The drop off in money growth is ONGOING in the UK, in EMU and in Japan whereas, in the US, money growth has bounced up off its six-month low to see its three-month growth rate hover at the pace of year-over-year money growth at 3.5% - hardly a barn burner.

In EMU credit growth remains restrained in terms of over overall loan growth and in terms of credit to residents. Both of these measures of credit are declining in real terms and the rate of shrinkages is either large or is accelerating from one-year to six-months to three-months. That is not a good story if you want it end with everyone living ‘happily ever after.’

Money and credit are the raw material or fuel for growth. Right now the tanks are dang near empty across the major monetary center countries. Even China has begun a program of pulling back on credit, but there it is after a period of excessive growth.

On balance for all the concerns about inflation all we really have is some volatile oil price that on occasion feeds though to bash headline inflation like cars in a long train bumping into one another on down the line, long after the locomotive has stopped. Inflation by the core measures remains tame. Inflation fundamentals are rock solid as there are huge GDP-gaps around the world and an all-too ample supply of labor. Money supply growth is tame, tempered or outright withering. Worrying about too-liquid bank reserves while banks are bottling up credit growth makes no sense at all. Yet I like to understand this fear by pointing out that a large block of the economics profession forms a school called ‘monetarism’ and if it did not register horror at the size of those bank reserves all those economists probably would have to find a new ‘religion.’ It may be in time that those reserves will be worth worrying about. Once banks lose their fear and start lending again, reserves may one again be a risk. But forest fires rarely start in the wet and rainy season; that is what we have as an economic environment right now. Inflation starting in an environment like this is really a very small risk. Conversely, it is growth that is at risk and it is lending that is needed to keep it going. So far that spark of lending is lacking just about everywhere. We should not douse a spark to warm our hands for fear of burning a forest.

| Look at Global and Euro Liquidity Trends | |||||||

|---|---|---|---|---|---|---|---|

| Saar-all | Euro Measures (E13): Money & Credit | G-10 Major Markets: Money | Memo | ||||

| €-Supply M2 | Credit:Resid | Loans | $US M2 | £UK M4 | ¥Jpn M2+Cds | OIL:WTI | |

| 3-MO | -0.7% | -0.1% | 0.3% | 3.5% | 3.1% | 1.7% | 33.5% |

| 6-MO | 0.6% | 0.1% | -0.7% | 2.0% | 5.7% | 2.4% | 15.3% |

| 12-MO | 2.0% | 0.7% | -0.2% | 3.4% | 5.3% | 3.1% | 74.0% |

| 2Yr | 5.5% | 4.1% | 2.9% | 6.5% | 10.8% | 2.4% | -9.5% |

| 3Yr | 7.1% | 7.2% | 5.6% | 6.4% | 11.2% | 2.3% | 6.3% |

| Real Balances: deflated by Own CPI. Oil deflated by US CPI | |||||||

| 3-MO | -2.8% | -2.2% | -1.8% | 0.2% | -0.1% | 2.6% | 29.2% |

| 6-MO | -0.9% | -1.4% | -2.2% | -0.9% | 2.4% | 3.7% | 12.1% |

| 12-MO | 1.0% | -0.2% | -1.1% | 0.6% | 2.4% | 4.8% | 69.3% |

| 2Yr | 4.2% | 2.8% | 1.7% | 5.1% | 7.6% | 3.1% | -10.7% |

| 3Yr | 5.2% | 5.2% | 3.7% | 4.0% | 8.2% | 2.5% | 4.0% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief