Global| Apr 24 2006

Global| Apr 24 2006$73.83: Oil & Water

by:Tom Moeller

|in:Economy in Brief

Summary

The domestic spot price for a barrel of West Texas Intermediate crude oil settled at $73.83 on Friday, driven by Mid East supply concerns and strong demand. That easily surpassed last August's high of $70 reached in the wake of [...]

The domestic spot price for a barrel of West Texas Intermediate crude oil settled at $73.83 on Friday, driven by Mid East supply concerns and strong demand. That easily surpassed last August's high of $70 reached in the wake of Hurricane Katrina.

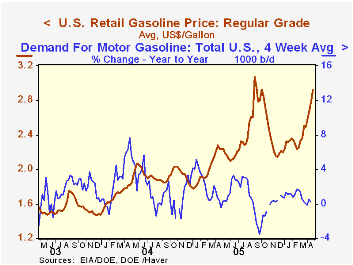

Just ahead of the peak summer driving season, retail gasoline prices at $2.78 per gallon additionally have been boosted by supply shortages (especially for high test) by the phase-out of MTBE for ethanol.

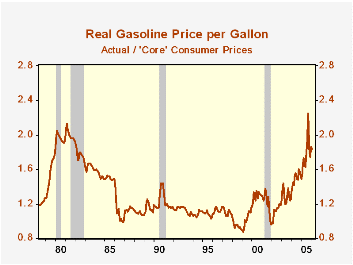

Adjusted for the inflation in "core" consumer prices, gasoline prices are at the all time high reached in 1981, although prices remain low compared to other liquids such as Evian water ($21.19/gallon) and Gatorade ($10.17/gallon).

Growth in demand for gasoline recently wobbled, but the y/y rise of 0.2% in the four week average added to gains which ranged between 1.0% and 2.6% during the prior five years. Growth in the number of miles driven by U.S. motor cars has ranged near 2% this decade, down somewhat from 2.6% during the 1990s and the average fuel consumed per car rose last year to 557 gallons, up 14% from a low during 1991. The figure is, however, down by one quarter since the early 1970s. This data is available in Haver's USECON database.

Inflationary concerns fueled Friday's gold price to $623.50 per ounce, up 20.8% since the end of last year. Since 1980 there has been a 56% correlation between the level of gold prices and the y/y change in consumer prices.

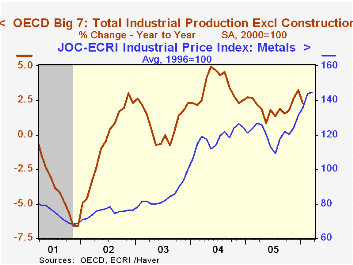

Industrial metal prices also have been strong with the JoC-ECRI Industrial Metals Prices Index up 18.9% this year driven by strength in aluminum prices (up 16.5%), copper scrap (up 16.5%) and zinc (up 65.1%). Additionally, high grade copper prices have risen 34.4% since year end '05. Growth in industrial production is behind the rise and during the last ten years there has been a 49% correlation between the level of industrial metals' prices and the y/y change in OECD Big Seven industrial production.

Gasoline Affordability from the Federal Reserve Bank of St. Louis is available here.

| Weekly Prices | 04/18/06 | 12/27/05 | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Light Sweet Crude Oil, WTI (per bbl.) | $71.36 | $58.16 | 36.4% | $58.16 | $41.78 | $32.78 |

| U.S. Retail Gasoline (per gallon) | $2.78 | $2.20 | 24.4% | $2.27 | $1.85 | $1.56 |

| Gold: Handy & Harmon (per Troy Oz., EOP) | $614.75 | $507.40 | 28.3% | $507.40 | $443.40 | $416.25 |

| High Grade Copper (Comex, /Lb., EOP) | $3.06 | $2.28 | 105.5% | $2.28 | $1.54 | $1.04 |

| Stainless Steel Scrap (/ton, EOP) | $1,574 | $1,268 | -8.0% | $1,268 | $1,558 | $1,265 |

by Louise Curley April 24, 2006

The results of the April surveys of business conditions in the Euro Zone are beginning to appear. Most of these surveys are expressed in terms of the percent balance between those who see improvement and those who see deterioration.

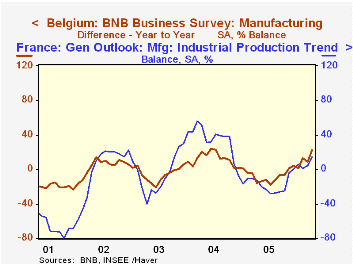

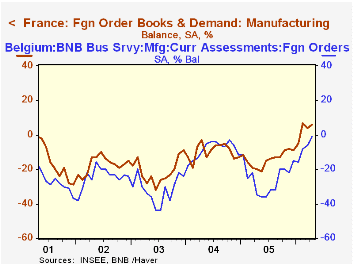

France and Belgium reported today. Both countries showed improved sentiment, particularly when compared with a year ago, as can be seen in the first chart, which compares the year-to-year changes in the percent balance reporting on the general outlook for manufacturing in both countries.

Improvement in sentiment regarding foreign orders has played a significant part in the overall improvement in sentiment in both countries. The upward trends in the percent balances from big to small negatives in the case of Belgium and from big negatives to positives in the case of France are shown in the second chart.

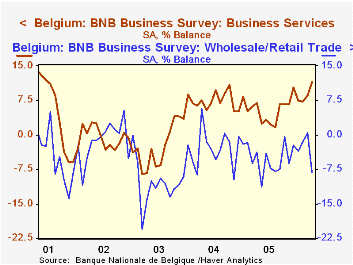

The Belgium survey is much broader than the French. The French survey conducted by INSEE (Institute National de Statisque et Etudes Economique) covers only the manufacturing industry, while the Belgium survey conducted by the National Bank of Belgium covers, in addition to manufacturing, other industry, wholesale and retail trade, the construction, ex public works, and service industries. The most marked differences among business opinion in Belgium are seen between those engaged in business services and those engaged in wholesale and retail trade. Since the end of 2003, there have been more optimists than pessimists in the service industries, while the pessimists have prevailed in the wholesale and retail trade. The third chart shows the percent balances for the service industry and for wholesale and retail trade.

The sharp run up in the price of oil of the past week or so is probably not reflected in the April surveys and could have a dampening effect on future business opinions.

| Business Surveys (Per cent Balance) | Apr 06 | Mar 06 | Apr 05 | M/M dif | Y/Y dif | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|---|---|

| France | ||||||||

| Manufacturing | 2 | -2 | -13 | 4 | 18 | -12 | 5 | -29 |

| Foreign Orders | 6 | 4 | -20 | 2 | 26 | -14 | -10 | -21 |

| Belgium | ||||||||

| Manufacturing | 6.0 | 0.0 | -16.0 | 6.0 | 22.0 | -9.9 | -2.7 | -15.0 |

| Wholesale & Retail Trade | -8.2 | 0.5 | -3.8 | -8.7 | -4.4 | -2.1 | 7.7 | -9.3 |

| Construction ex Public Works | 7.0 | 3.9 | 0.6 | 3.1 | 7.6 | 1.5 | 5.9 | 4.1 |

| Business Services | 11.5 | 8.6 | 7.0 | 2.9 | 4.5 | 5.6 | 7.6 | -2.5 |

| Foreign Orders | 18 | 6 | -20 | 12 | 38 | -8 | 5 | -9 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.