Global| Jul 14 2008

Global| Jul 14 2008UK Losses Grip on PPI Inflation

Summary

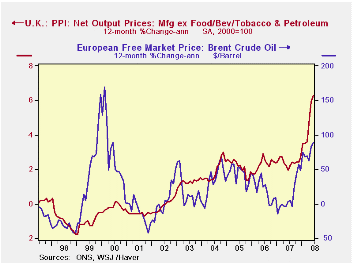

You can like Mervyn King, Governor of the BOE, and BOE itself. But that bank has lost its grip on inflation, at the PPI level and that is chilling. PPI inflation has absolutely surged sending the CORE PPI rate up by 6.3% Yr/Yr and the [...]

You can like Mervyn King, Governor of the BOE, and BOE itself.

But that bank has lost its grip on inflation, at the PPI level and that

is chilling. PPI inflation has absolutely surged sending the CORE PPI

rate up by 6.3% Yr/Yr and the three month core rate to 11.8% in arise

reminiscent of the 1970s bell-bottoms and Carnaby Street – all that

along with its destructive episode of inflation. Of course the RPC/HICP

inflation measures are more important ones, but these sorts of

pressures at the factory gate level spell bad news for inflation

elsewhere in the economy. PPI headline inflation is bristling at a 10%

paces and over three-months UK headline inflation is over 17% for the

PPI. All that is very bad news indeed.

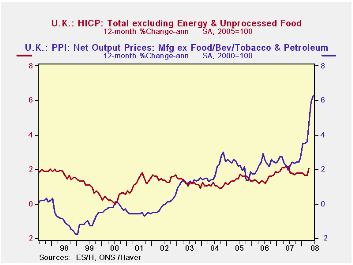

The second chart shows that the core HICP inflation rate has remained much more stable in the face of rising oil prices and even the rising PPI results. Still, there have been several step ups in the HICP pace and right now there is the threat of an acceleration that may be taking root.

As is the case in the US there is more pressure at the PPI level than at the consumer prices level in the UK. UK the core PPI inflation has a correlation with the core HICP of only 0.25, in R-square terms that is only 0.06 – a very low association.

The BOE may be able to keep this wolf at bay. But what is shocking for the moment at least is the degree of pressure that is being mounted on the PPI. If only a fraction of it gets into the HICP it will be too much. With this report in hand and with PPI data more topical by a full two months (June for the PPI Vs April for the HICP) inflation trends at the consumer level will be under the microscope in the UK.

| UK PPI | |||||||

|---|---|---|---|---|---|---|---|

| %m/m | %-SAAR | ||||||

| Jun-08 | May-08 | Apr-08 | 3-mo | 6-mo | 12-mo | 12-moY-Ago | |

| MFG | 0.9% | 1.8% | 1.3% | 17.2% | 13.6% | 10.0% | 2.4% |

| Core | 0.3% | 1.4% | 1.1% | 11.8% | 9.6% | 6.3% | 2.0% |

| Core: ex food beverages, tobacco & Petroleum | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief