Global| Apr 26 2006

Global| Apr 26 2006UK GDP: Broader, Steadier Growth in Q1

Summary

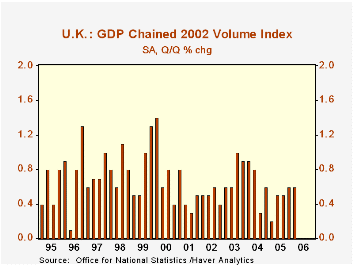

In the UK, the first major economy to report for Q1, growth maintained a 0.6% quarterly rate, the same as in Q4. However, growth was much more evenly balanced among various sectors, so the gain can be viewed more favorably because it [...]

In the UK, the first major economy to report for Q1, growth maintained a 0.6% quarterly rate, the same as in Q4. However, growth was much more evenly balanced among various sectors, so the gain can be viewed more favorably because it is more broadly based.

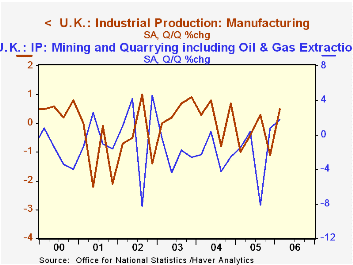

Production industries, in particular, turned up after four consecutive quarterly declines, and at 0.7% growth, had their best performance since Q3 1999. All three major sectors, mining (including oil and gas extraction), manufacturing and utilities, participated.

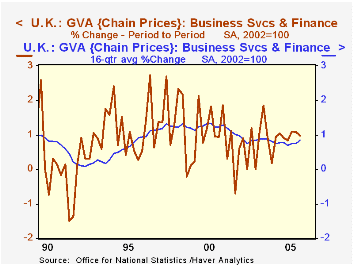

Service industries, in contrast, slowed from their pace in the second half of last year, although their 0.6% growth remained in a range that has characterized the last several years. In Q1, the distribution, lodging and catering industries were flat following a sizable increase in Q4. Transportation and communications increased 0.9% after Q4's 1.5%; this sector has been somewhat less volatile in recent quarters than the saw-tooth pattern it has generally traced over the past 20 years. The business services and finance sector has been smoothing even more. It grew almost exactly 1.0% in Q1, equal to its six-quarter average increase. So while the latest gain isn't the largest ever, it is far more likely to be sustained than the pointed ups and downs of the years before 2004.

So the UK experienced growth this past quarter that is steadier and broader than before. This combination, like diversity in an investment portfolio, puts that economy in a better position to withstand adverse developments in the months ahead, such as still higher energy prices or other inflationary stresses.

| United Kingdom: (Chained, SA, 2002=100) |

Q1 2006 | Q4 2005 | Q3 2005 | Year/ Year | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|---|

| GDP* | 0.6 | 0.6 | 0.5 | 2.2 | 1.8 | 3.1 | 2.5 |

| Production Industries | 0.7 | -0.9 | -0.7 | -1.0 | -1.9 | 0.6 | -0.5 |

| Service Industries | 0.6 | 1.0 | 0.8 | 3.0 | 2.8 | 3.5 | 2.7 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief