Global| Mar 14 2006

Global| Mar 14 2006U.S. Retail Sales Off, But ...

by:Tom Moeller

|in:Economy in Brief

Summary

US retail sales fell 1.3% last month but several factors suggest the decline hardly indicates consumer spending weakness, even though it exceeded Consensus expectations for a 0.8% drop. 1) January's warm weather surge in spending was [...]

US retail sales fell 1.3% last month but several factors suggest the decline hardly indicates consumer spending weakness, even though it exceeded Consensus expectations for a 0.8% drop. 1) January's warm weather surge in spending was revised higher to 2.9%. 2) Retail sales during January and February were 2.8% above 4Q05. 3) The 0.4% decline in nonauto sales was less than Consensus expectations for a 0.5% drop.

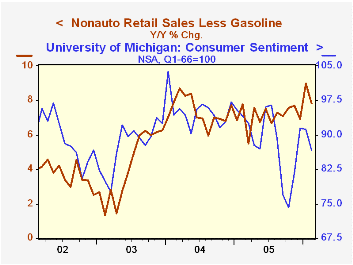

Lower nonauto retail sales followed a January surge revised up to 2.6% and the two month strength in sales left the 1Q average so far 2.3% above 4Q which rose 1.9% from 3Q.

Motor vehicle & parts dealers sales fell 4.6% (-0.9% y/y) after an upwardly revised 4.2% January spurt. The decline was in line with the 5.8% m/m drop in unit auto sales during February.

Lower apparel store sales reflected the brunt of the warm-weather give back from January strength. A 3.3% (+1.6% y/y) drop followed the downwardly revised 2.4% gain. Elsewhere, discretionary spending looked respectable. General merchandise store sales slipped just 0.3% (5.3% y/y) after a little revised 1.8% January rise. Sales of furniture, electronics & appliances fell 3.1% (+5.6% y/y) after a 5.6% January spurt that was much stronger than the 2.9% gain reported initially.

Building material sales rose another 1.5% (20.5% y/y) after a 7.3% jump in January that was double the rise initially estimated.

Sales at gasoline stations fell 1.6% (+17.7% y/y) as retail gasoline prices fell 1.5%. In March, gasoline prices at $2.35 per gallon are 3.0% higher than during February.

Less gasoline, nonauto retail sales fell 0.3% (+7.8% y/y) last month following a 2.4% January spike that revised up from 1.8% reported initially.

Sales of nonstore retailers (internet & catalogue) surged 3.2% (13.3% y/y) after a little revised 2.7% January decline.

| Feb | Jan | Y/Y | 2005 | 2004 | 2003 | |

|---|---|---|---|---|---|---|

| Retail Sales & Food Services | -1.3% | 2.9% | 6.7% | 7.5% | 7.3% | 4.3% |

| Excluding Autos | -0.4% | 2.6% | 8.9% | 8.6% | 8.2% | 4.7% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief