Global| Apr 30 2009

Global| Apr 30 2009U.S. Personal Spending & Income Still Under Pressure

by:Tom Moeller

|in:Economy in Brief

Summary

Any recovery in consumer spending will have to wait. The U.S. Bureau of Economic Analysis reported that personal spending during March fell another 0.2% and adjusted for inflation spending also fell 0.2%. These declines followed two [...]

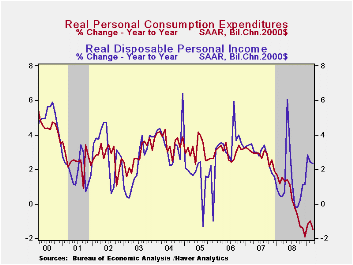

Any recovery in consumer spending will have to wait. The U.S. Bureau of Economic Analysis reported that personal spending during March fell another 0.2% and adjusted for inflation spending also fell 0.2%. These declines followed two months of increase but for all of the first quarter, real spending rose at just a 2.2% annual rate. That makes up little of the 4.3% decline during 4Q and the 3.8% 3Q drop.

Real spending on furniture & appliances last month retraced the gains of January & February with a 2.3% (-1.3% y/y) decline. Real spending on apparel also stuttered and fell 0.6%, reversing the February increase. Even real spending on services has been flat as it rose 0.1% last month after no change during February (+0.9% y/y). Any life in spending during March was limited to autos which rose 0.9%. That finished a quarter where spending made up half of the 4Q decline with a 4.8% increase.

The reason for the delay in a spending recovery is that income remains under extreme pressure from the soft job market. The 0.3% decline in March personal income was the fifth shortfall in the last six months and it fell short of expectations for a 0.2% decline. In addition, disposable personal income was flat for the second consecutive month. That followed the 1.6% jump which was the result of a 10.5% monthly drop in taxes. Adjusted for inflation, real disposable income also was flat last month after a 0.3% decline during February. For the quarter, real take-home pay rose at a 6.2% annual rate which was double the 4Q increase.

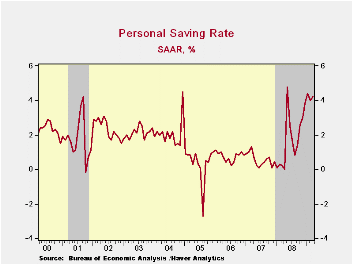

The good news from the latest report was that despite weaker income growth, lower spending has worked to lift the savings rate. The rise to 4.2% during March lifted the quarter's rate also to 4.2% which was its highest level since 1998.

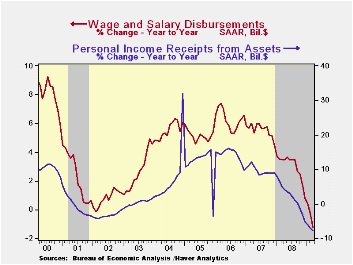

Reflecting the weakness in the job market, wages & salaries fell another 0.5% (-1.2% y/y) and they have been flat or down in each of the last seven months. Over that period wages have fallen at a 3.2% annual rate, the quickest rate of decline since 1994. Private sector wages during that period were down at a 4.7% annual rate, still the worst since 1994. These declines contrast to wages in the government sector which continue to increase, at a 4.1% rate during the seven months.

Lower interest rates continued to pull interest income down, by 0.6% during each of the last three months (-6.1% y/y). In addition weak corporate profits lowered dividend income by 1.8%, about the monthly rate of decline since October (-10.2% y/y).

Finally, the PCE chain price index benefited from a 4.3% seasonally adjusted decline in gasoline prices (-37.7% y/y) and fell slightly. Core pricing power repeated the gains of the prior two months with a 0.2% increase that reflected a 1.5% increase in "other" nondurable goods prices. Most other goods and services prices were flat or down. The latest gain in the overall price deflator exceeded Consensus expectations for a 0.1% rise.

The personal income & consumption figures are available in Haver's USECON and USNA databases.

Ponds and Streams: Wealth and Income in the U.S., 1989 to 2007 from the Federal Reserve Board can be found here.

| Disposition of Personal Income (%) | March | February | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Personal Income | -0.3 | -0.2 | 0.3 | 3.8 | 6.1 | 7.1 |

| Disposable Personal Income | -0.0 | 0.0 | 3.0 | 4.6 | 5.5 | 6.4 |

| Personal Consumption Expenditures | -0.2 | 0.4 | -0.9 | 3.6 | 5.5 | 5.9 |

| Saving Rate | 4.2 | 4.0 | 0.2 (March '08) | 1.8 | 0.5 | 0.7 |

| PCE Chain Price Index | -0.0 | 0.3 | 0.6 | 3.3 | 2.6 | 2.8 |

| Less food & energy | 0.2 | 0.2 | 1.8 | 2.2 | 2.2 | 2.3 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.