Global| Jan 22 2010

Global| Jan 22 2010U.S. Leading Economic IndicatorsSuggest Continued Recovery

by:Tom Moeller

|in:Economy in Brief

Summary

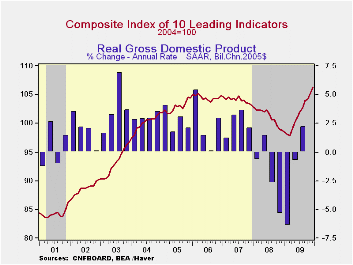

The firm uptrend in the Conference Board's Index of Leading Economic Indicators continued last month with a rise of 1.1% following an upwardly revised like gain in November. It was the ninth consecutive monthly increase and the 10.8% [...]

The firm uptrend in the Conference Board's Index of Leading Economic Indicators continued last month with a rise of 1.1% following an upwardly revised like gain in November. It was the ninth consecutive monthly increase and the 10.8% (centered) rate of increase during the last six months remained nearly the strongest since early-1983. The leading index is based on actual reports for eight economic data series. The Conference Board initially estimates two series, consumer and capital goods orders.

The leaders' increase supports widespread forecasts for a 4.5% (AR) gain in 4Q 2009 real GDP. The preliminary figures will be released this coming Friday.

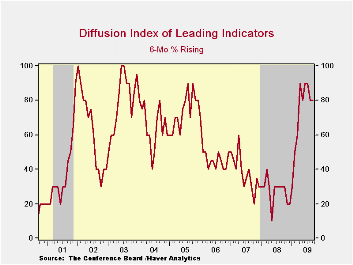

The breadth of increase amongst the component series improved last month back to the strongest percentage of the cycle. Nine out of the ten components rose during December versus 70% during the prior two months. During the most recent six months, however, just 80% of the series rose. Prominent in last month's increase was a steeper interest rate yield curve, higher building permits and lower initial claims for unemployment insurance.

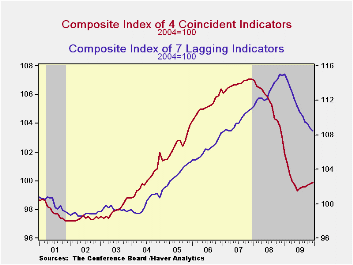

Continuing to suggest economic improvement was the coincident indicator series which rose for the fifth month in the last six. The 0.1% December gain followed a 0.1% November increase that was revised down slightly. During the last six months the 1.2% rate of increase in the coincident series compares to a -7.9% reading at its worst in January. Increases in industrial production, real personal income and business sales have been modest but compare to sharp declines late in 2008. Declines in payroll employment also have eased considerably.

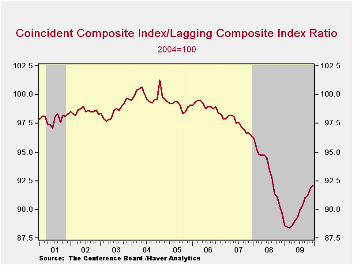

In a continued sign that excesses in the U.S. economy are still falling, the lagging index has been falling since January. Leading the decline have been lower commercial & industrial loans outstanding, slower growth in labor costs, less consumer credit and slower service price inflation. The ratio of coincident-to-lagging indicators (another leading indicator) also continued higher for the ninth straight month to the highest level since August of 2008.

The Conference Board figures are available in Haver's BCI database. Visit the Conference Board's site for coverage of leading indicator series from around the world. The latest U.S. Leading Indicators release can be found here here.

| Business Cycle Indicators (%) | December | November | October | Sept. 6-Month % (AR) | 2009 | 2008 | 2007 |

|---|---|---|---|---|---|---|---|

| Leading | 1.1 | 1.0 | 0.3 | 10.8 | 0.4 | -2.8 | -0.4 |

| Coincident | 0.1 | 0.1 | 0.1 | 1.2 | -5.1 | -1.2 | 1.4 |

| Lagging | -0.2 | -0.5 | -0.2 | -4.8 | -1.6 | 3.2 | 3.0 |

by Robert Brusca January 22, 2010

EMU orders rise,

but beware the optimism

EMU orders rose in November more than expected. A lot is being made of

the much smaller Yr/Yr drop which now at -4.1% compares to the -12.1%

reported last month (not shown in the table). But this arithmetic is

tricky. As you can see this rise in orders in November was a relatively

modest +0.6%, while the difference in the Yr/Yr drop is a massive eight

percentage points. It’s because in November of 2008 orders had been

dropping very rapidly. Orders AVERAGED month-to-month drops of 6.8% in

Sept, Oct, and November of 2008. In December of 2008 orders then

plunged m/m by 10.9%! The upcoming Dec orders figure will be

delightful, as, if the level of orders is unchanged in Dec 2009, the

Yr/Yr orders figure will jump by 7.6% Yr/Yr. But that outcome would not

really signal any change in the pace of recovery, would it?

Perspective

We include in the table a column to remind you how much these various

series are off from their cycle peaks EVEN if that peak was more than

one year ago. Currently sales are off by 20% from their peak. Orders

are off by 23.6% from their peak. Orders in Germany, France, Italy and

the UK are also clustered around a peak-to-current drop of about 30%

(see table for hairsplitting).

No MFG sector

tooth-fairy

The point is that yes, there is some rebound in train, but that

industry has not made some magical recovery as if visited overnight (or

over-month) by the tooth-fairy. The industrial sector remains severely

impacted by the recession and is still very much in dig-out mode even

though the yr/yr figures will turn to a sharp positive reading in

December. For now e-zone sales are up from their cycle’s lowest point

by only 3.8%. Orders are up from their cycle lowest point by 10.9%. At

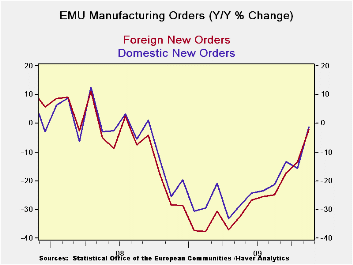

that foreign orders are leading the rebound with a rise of 12.7% from

their low compared to a rise of 9.3% by domestic orders form their low.

Germany at +19% from its low is showing the most rapid recovery –even

if its drop from its peak is now only about the same as elsewhere in

EU/EMU. While France at +2% is experiencing the smallest bounced from

its cycle low.

Growth, ‘yes’

but acceleration, ‘no’

Momentum is still building to the upside but it is not

accelerating. The three-month growth rate of orders is less than the

rate over six months (both annualized, of course). Over three-months

France and the UK have seen drops in orders and that is not good, but

it’s not decisive either. . Trichet’s warning that recovery would be

moderate and somewhat irregular is a simple statement of extrapolating

what is already in train: the gospel from the church of what’s

happening now.

Upbeat

interpretation is exaggerated

So despite the upbeat tone on the orders report of today, if we put the

data in context, it’s a slow plodding and irregular recovery in Europe.

Recovery is not gaining momentum despite the month’s result on orders

growth and despite yr/yr improvement in orders. We are more interested

in yr/yr results that are driven by changes in the front month than by

those driven by the back month which is the case in November and likely

will be the case in the December.

The Obama Plan

meets world opinion and reality

The recent reports from the e-Zone have become more circumspect. The UK

reported out some poor December retail sales results today (Friday, Jan

22). Japan hit a 21-year low in supermarket sales. President Obama’s

plan to corral unruly bank practices has sent a pall across the

financial sector and has bushwhacked stocks around the globe. It is

clear that a lot of work still lies ahead for the world’s key economies

if they are to get recovery in full swing. Attempts to set a new fairer

path for financial institutions may slow down this already slow

recovery. To make matters worse the noises from around the world’s

policy circles show a lot of disagreement over what President Obama has

announced even among those who like it ‘in principle.’ So, are we

doomed to an even weaker recovery?

A rational view

of irrationality

I urge a different message be distilled from this reluctance by banks

and bankers to modify their post-crisis behavior. Many see it as greed

and simply foment anger about it. I urge that bankers’ behavior be seen

in a broader context. Look at how reluctant bankers are to change even

with all their troubles and failings that were obviously of their own

doing. They do not want to change behavior or alter their

bonus-getting… why do economists assume that consumers will be so much

more wiling to make changes; to save more and to spend less? It seems

to me that the key to recovery is to get jobs growth going. Once it is

in gear I would expect consumers to spend as they always have. For

those newly back to work the urge to spend will be strong (pent up

demand). Discipline will flag among those who are now thrifty as the

crisis passes and as fear erodes.

Behavior is

behavior is behavior…

Behavior is hard to change and not just for bankers. Try to stop

smoking; try to lose weight; just TRY to stop spending. It is harder to

change when one does not learn from his own lesson; as bankers have not

learned as they were bailed out. Consumers have been put on a

starvation diet by taking their jobs and destroying their wealth. They

have not modified their behavior out of choice – something economists

don’t; yet seem to appreciate. They long to go back to their old

spending ways. And the wheels of change are spinning. I think the

potential of the up-swing is being under-valued for these reasons even

with all the obvious problems faced by the world’s economies. Behavior

is the hardest thing of all to change even if it is not rational

(smoking, overeating, overspending). Give consumers jobs and let them

earn income and they will go back to the ‘old normal’. Forget this

stuff about a ‘new normal’ that is more austere; it’s a positively

abnormal thought.

| Euro-Area and UK Industrial Orders & Sales Trends | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m |

% m/m | Nov 09 |

Nov 09 |

Nov 09 |

Nov 08 |

Nov 07 |

Qtr -2- Date |

From 2Y |

||

| Euro-Area Detail | Nov 09 |

Oct 09 |

Sep 09 |

3Mo | 6mo | 12mo | 12mo | 12mo | Saar | max |

| MFG Sales | 0.6% | 0.4% | -0.8% | 1.1% | 6.0% | -10.0% | -7.1% | 4.8% | 4.4% | -20.6% |

| Intermediate | 1.0% | -6.7% | 6.6% | 1.8% | 19.4% | -1.2% | -6.2% | 4.6% | 12.2% | -29.4% |

| MFG Orders | ||||||||||

| Total Orders | 1.6% | -1.9% | 1.6% | 5.0% | 19.3% | -4.1% | -23.4% | 9.8% | 0.3% | -26.5% |

| E-13 Domestic MFG orders | 1.0% | -6.7% | 6.6% | 1.8% | 19.4% | -1.2% | -25.5% | 8.8% | -14.6% | -29.4% |

| E-13 Foreign MFG orders | 0.6% | -2.2% | 7.1% | 23.8% | 26.7% | -2.1% | -28.3% | 11.0% | 4.7% | -30.6% |

| Countries: | Nov 09 |

Oct 09 |

Sep 09 |

3Mo | 6mo | 12mo | 12mo | 12mo | Qtr-2 Date |

|

| Germany: | 3.2% | -2.3% | 1.5% | 9.9% | 24.3% | -2.1% | -25.5% | 13.4% | 5.4% | -27.1% |

| France: | -0.4% | -8.8% | 4.7% | -17.9% | 4.0% | -4.5% | -23.7% | 9.7% | -23.2% | -29.6% |

| Italy | 2.6% | 0.6% | 6.0% | 42.9% | 11.9% | -4.1% | -25.7% | 9.6% | 12.9% | -30.0% |

| UK(EU) | -15.2% | 13.9% | 2.7% | -3.7% | -9.3% | -3.6% | -20.7% | 6.8% | 12.4% | -32.1% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief