Global| Dec 12 2007

Global| Dec 12 2007U.S. Import Prices Boosted in November by Oil

by:Tom Moeller

|in:Economy in Brief

Summary

During November, another jump in petroleum prices raised overall import prices by 2.7% after a 1.4% October increase. Consensus expectations had been for a 2.4% gain. Petroleum prices, overall, gained 18.0% (68.7% y/y). Fuel oil [...]

During November, another jump in petroleum prices raised overall import prices by 2.7% after a 1.4% October increase. Consensus expectations had been for a 2.4% gain.

Petroleum prices, overall, gained 18.0% (68.7% y/y). Fuel oil prices rose 18.0% (68.7% y/y) and crude petroleum prices rose 7.5% (53.0% y/y).

Less petroleum, import prices rose 0.7% after a 0.5% rise uptick during October.During the last ten years there has been a 66% (negative) correlation between the nominal trade-weighted exchange value of the US dollar vs. major currencies and the y/y change in non oil import prices. The correlation is a reduced 47% against a broader basket of currencies. Why a Dollar Depreciation May Not Close the U.S. Trade Deficit from the Federal Reserve Bank of New York is available here

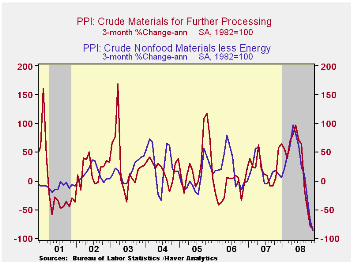

Prices for industrial supplies & materials excluding petroleum surged 2.7% (7.9% y/y). The detailed import price series can be found in the Haver USINT database.

Capital goods import prices rose 0.2% (0.8% y/y). Prices of computers, peripheral and semiconductors fell 0.2% (-5.1% y/y). Less the high tech sector, capital goods prices rose an accelerated 0.3% (3.2% y/y).

Prices for imports of consumer goods rose 0.2% (1.7% y/y) as apparel prices were unchanged after firm gains early this year (1.5% y/y). Prices for furniture and household items rose 0.2% (2.0% y/y).

Overall export prices were strong again and posted a 0.9% gain (6.1%y/y). Agricultural prices rose another strong 1.4% (23.0% y/y) while nonagricultural prices also were firm and rose 0.8% (4.6% y/y).

Global Savings, Investment and World Real Interest Rates is a 2007 working paper from the Royal Bank of Canada and it can be found here.

| Import/Export Prices (NSA) | November | October | Y/Y | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|

| Import - All Commodities | 2.7% | 1.4% | 11.4% | 4.8% | 7.5% | 5.6% |

| Petroleum | 9.8% | 5.1% | 53.0% | 20.6% | 37.6% | 30.5% |

| Non-petroleum | 0.7% | 0.5% | 3.0% | 1.7% | 2.7% | 2.6% |

| Export- All Commodities | 0.9% | 0.8% | 6.1% | 3.6% | 3.2% | 3.9% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief