Global| Apr 24 2009

Global| Apr 24 2009U.S. Durable Goods Orders Slip; Trend Still Sharply Negative

by:Tom Moeller

|in:Economy in Brief

Summary

There seems to be no letup in the factory sector's distress. That's the indication from a 0.8% slip in new orders for durable goods last month. While the magnitude of the slip was a positive surprise versus Consensus expectations for [...]

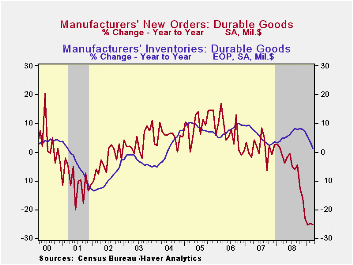

There seems to be no letup in the factory sector's distress. That's the indication from a 0.8% slip in new orders for durable goods last month. While the magnitude of the slip was a positive surprise versus Consensus expectations for a 1.5% decline, February's gain was lessened to 2.1% from 3.7% reported initially. The best that can be said about the latest figures is that the downward momentum in orders has slackened to a -24.2% annual rate during the last three months versus the 50% rate of decline as of January.

Lower orders for transportation equipment again led the decline in overall bookings with a 1.4% decline. Orders for motor vehicles fell hard and they are down by more than one-third during the last year. Orders for computers also fell a sharp 2.0% (-21.3% y/y) and primary metals bookings dropped 3.2% (-43.2% y/y). There were glimmers of light elsewhere in the report, but they were just faint ones. Electrical equipment orders made up their February decline with a 1.8% (-9.7% y/y) increase and machinery orders slipped just 0.1% (-26.3% y/y). Their strong February increase, however, was halved to 7.1%.

Perhaps another glimmer was the 1.9% increase in orders for nondefense capital goods. That followed a 4.9% jump during February. Orders excluding aircraft also recovered 1.5%. During the last ten years there has been an 80% correlation between the y/y change in nondefense capital goods orders and the change in equipment & software spending in the GDP accounts. The correlation of the GDP figure with capital goods shipments is, as one would expect, a larger 92%.

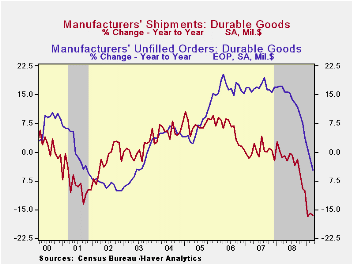

Shipments of durable goods continued to the downside at a steady rate. They fell 1.7% last month and they are off at a 27.9% annual rate during the last three. That weakness has been accompanied by a 30.0% three-month rate of decline in industrial production of durable goods. During the last ten years there has been an 80% correlation between the change in shipments of durable goods and the change in durables industrial production.

Inventory accumulation continues to respond to these production cuts. Inventories of manufactured durables fell 1.1% during March, about the same as they did during the prior two months. That brought the annual rate of decumulation to 13.1% during the last three months. That nearly matches the rate of decline during the 2001 recession but there's no end in sight if shipments don't show a sign of stabilization.

The durable goods figures are available in Haver's USECON database.

Fed Confronts Financial Crisis by Expanding Its Role as Lender of Last Resort from the Federal Reserve Bank of Dallas can be found here.

| NAICS Classification (%) | March | February | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Durable Goods Orders | -0.8 | 2.1 | -25.2 | -5.8 | 1.4 | 6.2 |

| Excluding Transportation | -0.6 | 2.0 | -20.3 | -1.2 | -0.3 | 9.1 |

| Nondefense Capital Goods | 1.9 | 4.9 | -31.1 | -6.8 | 3.5 | 9.4 |

| Excluding Aircraft | 1.5 | 4.3 | -18.4 | -0.3 | -2.7 | 10.7 |

by Tom Moeller April 24, 2009

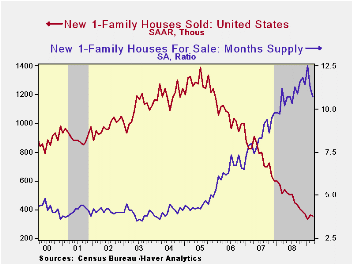

Sales of new single-family homes showed signs of forming a bottom after having declined by more than three-quarters since 2005. Sales during March slipped just 0.4% to 356,000 units after an upwardly revised 8.2% February increase. March sales exceeded Consensus expectations for 340,000 units.

The bottom, however, reflects divergent patterns across the country's regions. Sales in West rose sharply during the last two months though sales last quarter still were down 15.9% from 4Q'08. March sales in the South held steady after a sharp February gain and for the quarter fell a moderate 3.7%. Elsewhere in the country there's been little sign of stabilization of the downtrend. New home sales in the Midwest fell 7.8% last month after no change during February and for the quarter were down another 14.9%. Finally, in the Northeast new home sales fell to a record low and they've been dropping at a steady 60% annual rate.

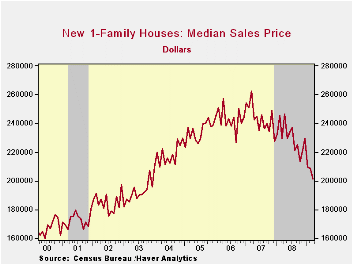

Reflecting sales weakness was another decline in the median price for a new single-family home. At $201,400 the figure was off for the third straight month as homebuilders attempted to move inventory. Since their peak early in 2007, new home prices have fallen by roughly one-quarter.

And the attempt to move inventory has been successful. The inventory of unsold homes is down by nearly one-half since the peak during 2006. In each of the country's regions, the inventory is down by one-quarter to one-third just during the last year.The month's supply of new homes for sale also has started to drop, in March to the lowest level since last July. But there's more inventory to move.

The new home sales figures are available in Haver's USECON database.

The Federal Reserve System published the annual financial statements for the combined Federal Reserve Banks. The report can be found here.

| US New Homes | March | February | Y/Y (%) | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Total Sales (SAAR, 000s) | 356 | 358 | -30.6 | 479 | 768 | 1,049 |

| Northeast | 19 | 28 | -32.1 | 35 | 64 | 64 |

| Midwest | 47 | 51 | -32.9 | 69 | 118 | 161 |

| South | 206 | 206 | -29.7 | 264 | 408 | 559 |

| West | 84 | 73 | -31.1 | 111 | 178 | 266 |

| Median Price (NSA, $) | 201,400 | 208,700 | -12.2 | 230,408 | 243,742 | 243,067 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief