Global| Nov 28 2007

Global| Nov 28 2007U.S. Durable Goods Orders Down Big for Second Month

by:Tom Moeller

|in:Economy in Brief

Summary

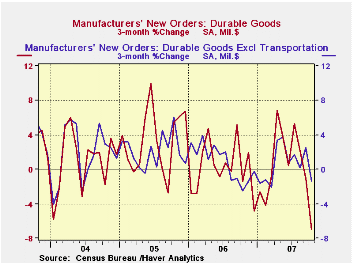

Orders for durable manufactured goods fell for the third consecutive month. The 0.4% slip in October followed a 1.4% slide in September that was only slightly revised. The latest slip contrasted with Consensus expectations for a 0.2% [...]

Orders for durable manufactured goods fell for the third consecutive month. The 0.4% slip in October followed a 1.4% slide in September that was only slightly revised. The latest slip contrasted with Consensus expectations for a 0.2% uptick.

Excluding the notably volatile transportation sector, orders

fell an unexpected 0.7% although the September figure was revised to a

1.1% gain from the slight 0.3% increase reported initially.

In the transportation sector, orders for aircraft &

parts fell 6.3% (+9.9% y/y) owing to a 5.2% (+10.6% y/y) decline in

nondefense orders. Orders for motor vehicles & parts also fell

a hefty 1.4% (-3.7 y/y), down big for the third consecutive month.

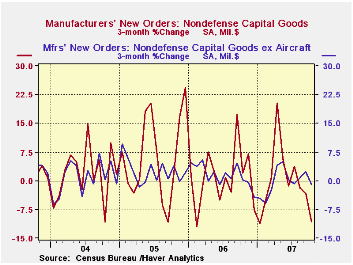

Orders for nondefense capital goods slid 3.1% helped lower by the drop in aircraft. Less aircraft, however, orders were also weak and posted a 2.3% decline. Three month growth in these orders fell to -1.0%, the weakest since early this year.

Fewer orders for communications equipment led the decline with

a 22.6% (+3.3% y/y) plunge. Machinery orders also fell 1.7% and three

month growth in these orders fell to -1.7%.

Also down were orders for computers & related products which fell 15.2% (+11.9% y/y) after strong gains during the prior two months.

To the upside, primary metal orders rose 3.0% (5.0% y/y) but

over the last three months the gain is a weaker 0.5%.Orders for

electrical equipment, appliances and components recovered all of the

prior month's decline with a 4.1% (1.8% y/y) gain.

Overall shipments of durable goods rose 0.6% (1.4% y/y) after large declines during the prior two months. Less transportation shipments rose 0.6% (1.6% y/y) after two months of declines by a like amount.

Inventories of durable goods rose 0.2% (2.1% y/y) and less

transportation rose 0.2% as well (1.2% y/y).

Unfilled orders were firm again last month and rose 1.0% (17.9% y/y). Much of that strength has been due, however, to the strength in orders for aircraft. Less the transportation sector altogether unfilled orders rose 0.7% in October and the y/y gain is a lesser 9.3%.

Financial Markets and Central Banking, today's speech by Federal Reserve Board Vice ChairmanDonald L. Kohn at the Council on Foreign Relations, New York, New York, is available here.

Minutes of Board discount rate meetings, October 1 through October 31, 2007 from the Federal Reserve Board can be found here.

| NAICS Classification | October | September | Y/Y | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|

| Durable Goods Orders | -0.4% | -1.4% | 1.9% | 6.3% | 9.9% | 5.3% |

| Excluding Transportation | -0.7% | 1.1% | 2.0% | 7.6% | 8.8% | 7.9% |

| Nondefense Capital Goods | -3.1% | 4.8% | -0.8% | 10.6% | 17.1% | 5.7% |

| Excluding Aircraft | -2.3% | 1.2% | -2.4% | 8.5% | 11.1% | 3.2% |

by Tom Moeller November 28, 2007

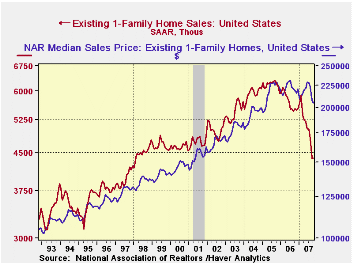

Another low was reached by existing home sales last month. The level of 4,970 (AR) about met expectations but was the lowest on record which extends back only to 1999. The tally of single family home sales, however, extends further back. For October, sales of existing single family homes were unchanged from the September level, but it was the lowest since early 1998. The figures are reported by the National Association of Realtors at the time sales are closed.

Weakness in sales last month was led by a 4.4% decline in sales out West. The count of single family sales in the West also fell by 2.5% (-33.1% y/y) to the lowest level since late 1995. Sales in the Midwest also were lower by 1.7% though single family sales were unchanged m/m (-15.9% y/y). Total sales in the Northeast were unchanged m/m as single family sales rose 3.1% (-13.2% y/y), the first gain in three months. In the South sales were also unchanged m/m as were sales of singe family units (-19.8% y/y).

The median price of an existing single family home fell for the fourth straight month. The 1.2% decline pulled prices 5.1% lower than last October and the price of an existing single family home fell as well, down 1.4% m/m and 6.3% y/y.

The Economic Outlook and Central Bank Policy is today' speech by Charles I. Plosser, President of the Federal Reserve Bank of Philadelphia and it is available here.

| October 2007 | Sept 2007 | Year Ago | 2006 | 2005 | 2004 | ||

|---|---|---|---|---|---|---|---|

| Number | M/M% | ||||||

| Total Sales | 4,970 | -1.2% | 5,030 | 6,270 | 6,510 | 7,075 | 6,727 |

| Northeast | 900 | 0.0 | 900 | 1,030 | 1,088 | 1,169 | 1,113 |

| Midwest | 1,180 | -1.7 | 1,200 | 1,420 | 1,492 | 1,588 | 1,550 |

| South | 2,030 | 0.0 | 2,030 | 2,520 | 2,578 | 2,704 | 2,540 |

| West | 870 | -4.4 | 910 | 1,300 | 1,353 | 1,616 | 1,575 |

| Single-Family | 4,370 | 0.0 | 4,370 | 5,708 | 5,677 | 6,182 | 5,958 |

| Median Price, Total, $ | 207,800 | -1.2 | 210,400 | 218,900 | 222,000 | 218,217 | 193,233 |

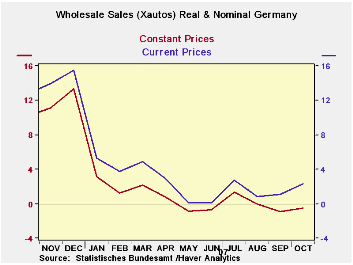

by Robert Brusca November 28, 2007

German wholesale sales growth is lagging in new quarter. Real

ex-auto sales remain challenged.

Europe has been spinning out mixed economic signals. While

there has been a lot of angst exhibited over the strong euro, the

German finance minister has embraced the strength and ECB members say a

strong currency is ‘the right sort of problem to have,’ better than the

other one.

In the wake of this strength EMU economic reports have become

uneven. While orders have showed weakness across countries, other

reports have showed some resilience, notably the IFO survey in Germany

and an INSEE morale survey for industry in France. The most recent

German consumer sentiment reading from GFK shows a weaker December is

in store. But there has been no full scale weakening.

German wholesalers fit not the mixed mode. Overall sales are

withering in the new quarter down by 0.1% Q/Q for an annual rate drop

of 0.7% and lower from the year ago three month period by 1.6% in real

terms. Ex autos sales are still eroding. The German VAT tax hike has

wreaked havoc with German retail/wholesale trends so far this year. Now

with the euro soaring, a new challenge is in gear. The strong euro does

not appear to have knocked the wind out of the German economy but it

has been added to list of headwinds that the economy faces. Labor

unrest and possibly more ECB rate hikes, especially in the wake of such

strong ongoing money and loan growth in EMU, also are on that list.

Despite it all German wholesale sales are only moderately weak.

| One Month of Quarter Complete | |||

|---|---|---|---|

| Quarterly showing | |||

| %Q/Q | %-Saar | %Q/Yr Ago | |

| Nominal | 1.1% | 5.5% | -19.8% |

| Real | -0.1% | -0.7% | -1.6 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief