Global| Jan 11 2010

Global| Jan 11 2010U.S. Consumer Credit Usage DeclineReaches Historic Proportion

by:Tom Moeller

|in:Economy in Brief

Summary

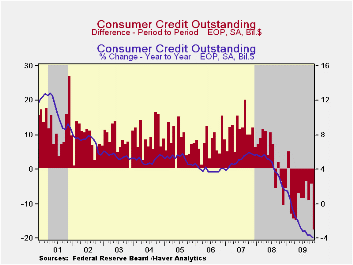

Is the consumer not attempting to borrow or is credit not being extended by the lender? It's hard to say but the Federal Reserve reported late-Friday that consumer credit outstanding fell by a record $17.5B m/m during November [...]

Is the

consumer not attempting to borrow or is credit not being extended by

the lender? It's hard to say but the Federal Reserve reported

late-Friday that consumer credit outstanding fell by a record $17.5B

m/m during November following a $4.2B October decline that was revised

slightly deeper from the initial report. The latest was the fourteenth

monthly drop since summer 2008. Moreover, the 3.9% y/y pullback in

credit outstanding set another historic record as consumers retrenched

and took account of debt-laden personal balance sheets along with job

market deterioration. Consumer credit outstanding as a percentage of

disposable income fell to 22.1% from its 2005 high of 24.7%.

Nevertheless, these rates remain up from the low near 16% in

1992.

Is the

consumer not attempting to borrow or is credit not being extended by

the lender? It's hard to say but the Federal Reserve reported

late-Friday that consumer credit outstanding fell by a record $17.5B

m/m during November following a $4.2B October decline that was revised

slightly deeper from the initial report. The latest was the fourteenth

monthly drop since summer 2008. Moreover, the 3.9% y/y pullback in

credit outstanding set another historic record as consumers retrenched

and took account of debt-laden personal balance sheets along with job

market deterioration. Consumer credit outstanding as a percentage of

disposable income fell to 22.1% from its 2005 high of 24.7%.

Nevertheless, these rates remain up from the low near 16% in

1992.

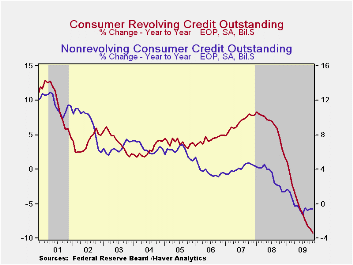

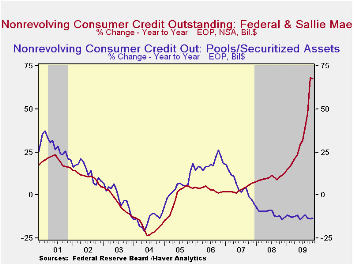

Usage of non-revolving credit (autos & other consumer durables), which accounts for nearly two-thirds of the total, fell $3.8B after a $3.2B October increase. The 0.6% y/y decline reflected a 13.2% drop in pools of securitized assets, an 11.2% decline in finance company lending and a 7.2% drop in nonfinancial business credit extensions. These were mostly offset by the federal government & Sallie Mae which expanded lending by more than two-thirds y/y and commercial bank lending which rose 1.1%. The latter figure, however, was down from 13% growth early in 2008.

Revolving credit usage fell a record $13.7B during November as part of a pullback that began late in 2008. The latest was part of a 9.3% y/y decline which also was by far a record. Versus November 2009, finance companies lowered lending by 37.9%, commercial bank lending fell 9.8%, pools of securitized assets fell 5.8%, savings institutions pulled back 3.9% y/y. Loans from credit unions offset some of these declines with a 6.2% increase.

These figures are the major input to the Fed's quarterly Flow of Funds accounts for the household sector.

Credit data are available in Haver's USECON database. The Flow of Funds data are in Haver's FFUNDS database.

Why Are Banks Holding So Many Excess Reserves? from the Federal Reserve Bank of New York is available here here.

| Consumer Credit Outstanding (m/m Chg, SAAR) | November | October | September | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Total | $-17.5B | $-4.2B | $-8.9B | -3.9% | 1.6% | 5.6% | 4.1% |

| Revolving | $-13.7B | $-7.3B | $-8.0B | -9.3% | 1.9% | 7.8% | 5.0% |

| Non-revolving | $-3.8B | $3.2B | $-1.0B | -0.6% | 1.4% | 4.4% | 3.6% |

by Louise Curley January 11, 2010

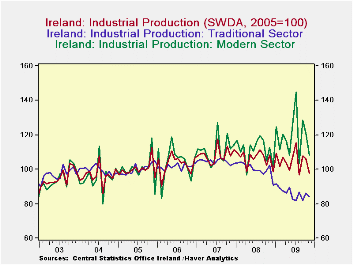

Recession continues in Ireland as Industrial production, announced today, declined 8.0% from 106.2 (2005=100) in Octoberto 97.7% in November. Ireland makes a distinction between its traditional industries and those of relatively recent origin. The "Modern" sector includes the following NACE industries reproduction of recorded music (182), manufacture of chemicals and chemical products (20), manufacture of basic pharmaceutical products and pharmaceutical preparations (21), manufacture of computers, electronic and optical products (26), manufacture of electric equipment (27) and medical and dental instruments and supplies (325). All the rest of the industries make up the traditional sector.

Month to month production in the Modern Sector has been volatile but has shown little trend. For instance production in the Modern sector declined 10.5% in November, but was down only 3.8% from a year ago. Production in the Traditional sector, on the contrary, has shown a definite downward trend. Although production in the Traditional sector was down only 2.2% in November, it was 17.7% below the year ago level. The attached chart shows total Industrial Production for Ireland and production in the Modern and Traditional sectors. The relative stability of production in the Modern Sector and the sharp decline of production in the Traditional Sector are apparent.

| IRELAND | Nov 09 | Oct 09 | Nov 08 | M/M % Chg | Y/Y/% Chg | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|---|

| Industrial Production (2005=100) | 97.7 | 106.2 | 108.0 | -8.00 | -9.54 | 106.5 | 108.3 | 103.0 |

| Traditional Sector | 84.4 | 86.3 | 102.5 | -2.20 | -17.66 | 100.3 | 104.7 | 101.6 |

| Modern Sector | 108.2 | 121.0 | 112.6 | -10.50 | -3.82 | 111.2 | 111.0 | 104.0 |

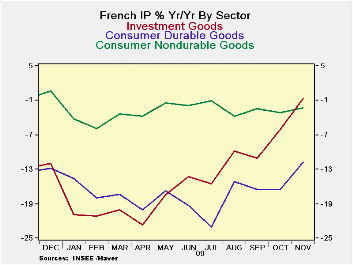

by Robert Brusca January 11, 2010

French IP is on the mend. Yr/Yr its decline has been reduced to under a 5% drop, at -3.8%. Over six months IP is expanding at a growth rate of 6.1%. Output of consumer durable goods is holding back the recovery although output of consumer durables rose in November. Auto output surged in November.

France is seeing output rise in Q4 at a very modest annual rate pace of 0.5%. Consumer durables output is falling at a 7% annual rate in Q4. Consumer nondurables and capital goods output are creeping ahead in the new quarter. Intermediate goods output is rising at a strong 6.3%.

The industrial sector globally is making a strong recovery from a disastrous drop in the recession. France’s recovery is about as advanced as that in any major industrial country. Still it has lost some momentum. This recovery continues to go in fits and starts. France’s IP advance in November is heartening but it does not turn up the speed of the expansion in any clear way.

| French IP Excluding

Construction |

|||||||

|---|---|---|---|---|---|---|---|

| Saar except m/m | Nov-09 | Oct-09 | Sep-09 | 3-mo | 6-mo | 12-mo | Quarter -to-date |

| IP total | 1.1% | -0.6% | -1.2% | -2.6% | 6.1% | -3.8% | 0.5% |

| Consumer Dur | 1.2% | -1.5% | -3.1% | -12.9% | -9.1% | -11.7% | -7.0% |

| Consumer Ndur | 0.4% | -0.6% | 1.9% | 7.1% | 3.1% | -2.2% | 0.8% |

| Capital | 2.4% | -0.8% | -3.1% | -6.0% | 12.4% | -0.7% | 0.8% |

| Intermed | 2.1% | 0.1% | -1.6% | 2.4% | 13.9% | -3.7% | 6.3% |

| Memo | |||||||

| Auto | 11.1% | -5.7% | -17.0% | -42.9% | 75.5% | 18.6% | -18.6% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief