Global| Oct 17 2019

Global| Oct 17 2019U.K. Retail Sales Volumes Are Nearly Flat on the Month

Summary

U.K. retail sales in September fell by 0.2% as the volume index ticked higher by 0.1%. Nominal sales volumes with a 50.7 percentiles are just a nudge above their median while sales volume growth over the past year at 6.3% has a 59.9 [...]

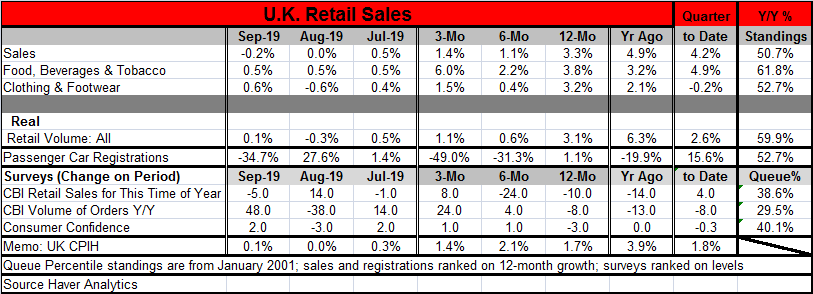

U.K. retail sales in September fell by 0.2% as the volume index ticked higher by 0.1%. Nominal sales volumes with a 50.7 percentiles are just a nudge above their median while sales volume growth over the past year at 6.3% has a 59.9 percentile standing, above its median pace. With the quarter completed nominal retail sales are up at a 2.5% pace in the quarter while real sales are up at a 1.4% pace. Inflation as measured by the CPIH is up at a 1.3% pace quarter-over-quarter, weaker than its 1.7% pace year-over-year.

U.K. retail sales in September fell by 0.2% as the volume index ticked higher by 0.1%. Nominal sales volumes with a 50.7 percentiles are just a nudge above their median while sales volume growth over the past year at 6.3% has a 59.9 percentile standing, above its median pace. With the quarter completed nominal retail sales are up at a 2.5% pace in the quarter while real sales are up at a 1.4% pace. Inflation as measured by the CPIH is up at a 1.3% pace quarter-over-quarter, weaker than its 1.7% pace year-over-year.

Passenger car registrations also fell in September, dropping by 34.7% month-to-month after spurting by nearly that much the month before. Still, passenger car registrations are falling fast over three months and six months against a gain of only 1.1% over 12 months.

Trends in nominal and in real sales are not one way. For both year-over-year pace gives way to a weaker six-month pace, but then the three-month pace rises above the six-month pace. Yet, in both cases, the three-month pace is still below the year-on-year pace by at least 50% so here is a reason to say that sales are slowing.

The bottom panel of the table features surveys with the appropriate inflation metric memorialized at the table’s very bottom. Surveys are presented as changes so the various columns show month-to-month changes or 12-month to six-month changes or six-month to three-month changes and so on. The rankings of the indicators, however, are done on their raw levels. These rankings are below their respective medians (below 50% for all three metrics: (1) CBI retail sales for the time of year, (2) CBI volume of orders compared to a year ago, and (3) consumer confidence. On all three of those metrics, retailing is below its median and in all cases quite far below its median. Year-over-year all three metrics are net lower; over six months only the CBI orders (y/y) have any real improvement-and even that one is small. Over three months compared to six-month average all show some improvement, but then look back at the queue ranking column to see what the actual standing is and there is nothing but residual weakness (repeat: all rankings are below their respective medians; below 50%).

Brexit...as in exit. At least for some; is that a catch?

However, the big news on the day for the U.K. is not retail sales and its prospects, but the fact that Boris Johnson has gotten a Brexit deal with the EU that he must now sell at home. His deal is one that was derided and tabled when Theresa May tried it because it does not keep all of the U.K. on the same system. It is for that reason opposed by the DUP, the conservative Northern Irish party. But if Northern Ireland does not want to have hard borders with Ireland that it must remain in the EU along with it. Boris’ solution is to take the rest of the U.K. off of EU rules and to keep Northern Ireland in the EU. That will mean that all U.K.-Northern Ireland shipments must be inspected and this is what Northern Ireland abhors. But policy is not made in a vacuum. And the only other non-hard-border solution would be to keep all of the U.K. in the EU as well. Apparently Johnson is not willing to do that. Ireland has lauded this solution as ‘innovative.’ But then this solution will cause Ireland and Northern Ireland to grow closer together as they will be in the same customs union. This precisely what the DUP is worried about. Boris is simply taking one of the many paths tried by Theresa May and offering it up as his own (inevitable) solution against a hard time line and EU ‘tyranny.’

Since Johnson ejected the DUP from his party, he no longer needs to kow-tow to them. But it will soon become clear how the rest of parliament thinks about the matter. The U.K. has to decide if it wants to jail-break most of the U.K. out of EU or if having one set of rules for commerce in the U.K. makes more sense.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief