Global| Jun 02 2020

Global| Jun 02 2020U.K. House Prices Fall

Summary

The closely watched Nationwide Survey of U.K. home prices produced a 1.7% m/m drop in May. This was the first monthly price drop in the Nationwide series since September of last year when prices ticked lower by 0.1% m/m. The May 1.7% [...]

The closely watched Nationwide Survey of U.K. home prices produced a 1.7% m/m drop in May. This was the first monthly price drop in the Nationwide series since September of last year when prices ticked lower by 0.1% m/m. The May 1.7% drop is by itself large and is the largest drop since December 2008, during the period of the financial crisis. From May to December of 2008, there were five of those eight months in which the Nationwide index fell by more than 1.7% per month. The index fell by some amount for 16-months in a row around that period.

The closely watched Nationwide Survey of U.K. home prices produced a 1.7% m/m drop in May. This was the first monthly price drop in the Nationwide series since September of last year when prices ticked lower by 0.1% m/m. The May 1.7% drop is by itself large and is the largest drop since December 2008, during the period of the financial crisis. From May to December of 2008, there were five of those eight months in which the Nationwide index fell by more than 1.7% per month. The index fell by some amount for 16-months in a row around that period.

It is reasonable to wonder what kind of a precedent 2008 might be for the period ahead since the economy is also greatly impacted and this too will become a period of recession, albeit an artificially induced recession. The drop in U.K. homes prices in May is hardly a surprise since transactions were impeded by the lockdown. Apart from the shelter at home provision, policy is causing people to lose employment and income and that is lasting damage that could impact home prices in the future. There are concerns that the virus could cause people to rethink living and commuting patterns to work and those things could affect house prices as well. The coronavirus could be disruptive not only of economic activity by reducing it but also by instigating changes in how and where people engage with the economy. So there are many possible impacts on house prices and a difference set of forces than those seen in a usual economic downturn.

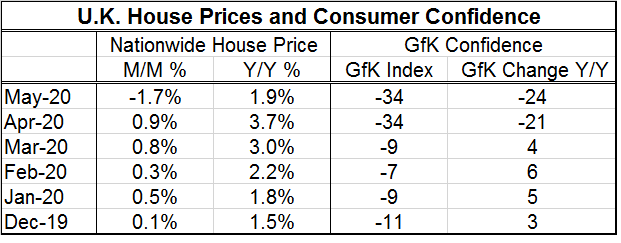

The table and the graph show the relationship between GfK consumer confidence and the Nationwide Survey home prices. The relationship is not tight, but it is indicative. The cycles in confidence and in home prices do work together. The table shows that GfK confidence fell sharply in April and in May home prices fell more sharply than they had in more than a decade. GDP matters, confidence matters, and for individuals the usual metrics of income and wages matter to home prices.

The table and the graph show the relationship between GfK consumer confidence and the Nationwide Survey home prices. The relationship is not tight, but it is indicative. The cycles in confidence and in home prices do work together. The table shows that GfK confidence fell sharply in April and in May home prices fell more sharply than they had in more than a decade. GDP matters, confidence matters, and for individuals the usual metrics of income and wages matter to home prices.

There is likely to a period of at least soggy home prices ahead in the U.K. The virus is still in play and some people frankly are still afraid of it even as government allows conditions to normalize. Economic activity will continue to be disrupted and home prices will be one of many economic casualties as the virus is brought to heel and as a new normalcy is established.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief