Global| Feb 10 2005

Global| Feb 10 2005Trade Surpluses Sustained in Canada and Germany, Despite Strong Currencies vs. US Dollar

Summary

December trade data were reported today for several other countries besides the US. Developments among them were not dramatic, but one aspect can be highlighted. Two major trading partners whose currencies have been strong against the [...]

December trade data were reported today for several other countries besides the US. Developments among them were not dramatic, but one aspect can be highlighted. Two major trading partners whose currencies have been strong against the dollar have seen little impact of this currency movement on their general trade flows.

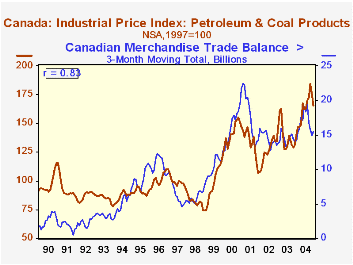

In Canada, for example, the trade surplus has remained wide. It was Can$5.21 billion in December, compared with an average for the entire year of 2004 of Can$5.60 billion and only about Can$4.80 billion the prior two years. Exports have remained sizable, although they have been lower the last few months after a surge in the spring. Imports have a largely flat trend. After such a long period of Canadian dollar strength, one might expect a more distinct narrowing of the Canadian trade surplus. However, while the Canadian dollar has strengthened against the US dollar, it has steadied against the euro during 2003 and 2004, so its trade patterns with that region would be unaffected by exchange rate considerations.

What does show as an apparent causative factor in the evolution of Canadian trade is the price of oil. As seen in the first graph, the merchandise trade balance in Canada is highly correlated with the wholesale price of petroleum and products in Canada, with a substantial 83% correlation ratio over the past 15 years.

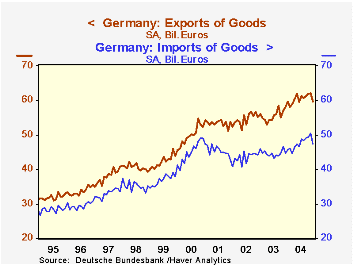

Trade in Germany also seems little affected by the dollar exchange rate. Shown in the second graph, exports and imports of goods have moved in basically parallel ways since the beginning of 2002. The trade surplus was €12.47 billion in December; as with Canada, this is lower than the year's average, €12.95 billion, but larger than the previous couple of years, which were around €11 billion. Through 2003, a simple export price deflator calculated from value and volume data shows a steep decline, followed in 2004 by some flattening. Thus, it appears that at least until recently, a good bit of the exchange rate impact was offset by local pricing, intended to try to keep German products competitive in world markets.

| Dec 2004 | Nov 2004 | Dec 2003 | 2004 | 2003 | 2002 | |

|---|---|---|---|---|---|---|

| Canada Trade Balance (Bil.Can$) | 5.21 | 5.49 | 5.09 | 5.60 | 4.85 | 4.77 |

| Exports | 36.48 | 35.56 | 33.21 | 35.86 | 33.33 | 34.48 |

| Imports | 31.27 | 30.07 | 28.13 | 30.26 | 28.49 | 29.72 |

| Germany Trade Balance (Bil.Euros) | 12.47 | 11.74 | 13.34 | 12.95 | 10.93 | 11.17 |

| Exports | 59.71 | 62.19 | 58.06 | 60.45 | 55.59 | 54.52 |

| Imports | 47.24 | 50.45 | 44.72 | 47.51 | 44.66 | 43.35 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief