Global| Oct 16 2019

Global| Oct 16 2019The Grip of Weakness Or the Gripe of Slow Growth?

Summary

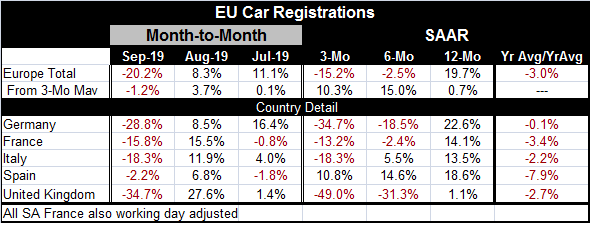

The headlines European auto sales fell sharply in September by 20.2% month-to-month but since they fell by 40% month-to-month one year ago in September; the year-over-year pace has accelerated to a 19.7% gain. That kind of volatility [...]

The headlines

The headlines

European auto sales fell sharply in September by 20.2% month-to-month but since they fell by 40% month-to-month one year ago in September; the year-over-year pace has accelerated to a 19.7% gain. That kind of volatility is why we also track the percentage gains from the trailing three-month average. On that basis, month-to-month sales in September fell by 1.2% as year-over-year sales rose by a thin 0.7%.

The stumble that keeps on giving...

Car registrations (or sales) are volatile, but they also seem to be weakening. The chart shows the massive drop in September of last year is something sales ‘worked their way out of' but not by the next month. By the next month there was only partial recovery and sales still are not back to their pre-September 2018 trend.

Smoothed momentum is anything but

The table below also calculates in the final column the year-average over year-average in sales. This metric looks at the average level of sales for the last 12 months and calculated the gain over the average level of sales over the previous 12 months. This is a very slow-moving but powerful calculation that is devoid of any seasonality. On this calculation, sales are down by 3%. On this same calculation extended to all five countries in the table, the result is a year-over-year decline, but only a thin -0.1% decline for Germany.

Did anyone get the number on that truck?

In addition to weak vehicle registrations, the euro area inflation rate was revised lower from 1% on a preliminary basis in September to 0.8%. Cooling spending and low plus falling inflation are not signs that fit together to form a package of strength for the economy. Yesterday the ZEW confidence indicators for Germany and the current assessments and expectations across the EMU continued to pump out weak readings. The U.K. reported out a relatively broad weakening in its labor market as the number of unemployed rose. The IMF issued a warning about weak global growth which it now sees as having slipped to 3%. It is also warning about corporate debt. If the economy slips, there could be another round of nasty surprises as many investors have ‘reached for yield' and bought into riskiness they otherwise would have avoided. But that has also been the ‘The Plan' of the central banks because by their buying most of the low-risk government assets the private sector has been tasked to stretch and to fund operation that otherwise might not have been so readily funded. It is also one of the reasons that the expansion has grown and sustained. So let's put the IMFs admonishment in its place.

Driven by the consumer

The expansion has been driven by the consumer. This is in no small part because China and other Asian countries have achieved so much export penetration and because Asia generally remains the domicile of the world's lowest cost producers. The slowing in registrations in Europe is not a welcome event. Neither is the weakening of the U.K. labor market. Nor is the decline in U.S. retail sales reported today.

Beyond the consumer

In yesterday's report, the IMF focused on its projections of slower pace of global growth and a reduced flow of trade. The IMF mentioned that monetary policy was no longer so equipped to act and it did not similarly note that fiscal policy too has been misused and may not pack the punch it used to deliver were it to be employed. The IMF essentially noted that if you are out of bandages you should be more careful about shooting yourself in the foot.

The easier said than done club

All the various conflicts that are in progress from Europe's tussling over Brexit to the U.S.-China trade war to Turkey's military offensive and much more play role in undermining global confidence. If growth is slowing and if weak growth countermeasures are in short supply, it might be a good idea to scale back on the things that undermine confidence. Welcome to the easier said than done club. There is no evidence that anyone is taking the IMF's advice. Turkey vowed not to have a ceasefire over Syria. The U.S. and China continue to add demands to what had appeared to be an agreement and to threaten to poke fingers in one another's eyes over ‘other matters.' This is not usually eh way successful negotiations proceed. And what had appeared to be a hopeful tilt on Brexit yesterday appears to have no impact today.

Growth trends

The global manufacturing sector has been slipping for some time. Trade has been the culprit, but services had carried on sustaining expansion. But now evidence suggests that the burden of carrying growth is too much for services. The construction sectors too in the U.S. and in Europe have lost momentum. It seems that the main thing holding growth in place is friction as all sectors slip toward weaker growth. And friction might slow the erosion, but it is not stimulus. This is my view of the problem. Underlying growth and momentum are too weak and too stretched to battle the forces of erosion that have kicked in. Monetary policy, once the domain of the knights on white horses, no longer rides to the rescue. Central bankers are no longer sure that more stimulus is a virtue. By the time they change that tune it almost surely will be too late and central banks will once more find themselves in the loss mitigation business instead of the loss avoidance business. Too bad.

Be careful what you wish for...

When the EMU was formed it was construed in the image and likeness of the Bundesbank and the notion was that the euro would become the new deutschemark- a zone of inflation stability. But the euro area was and is an amorphous place. There are different cultures and preferences and there has been the resulting culture clash that was inevitable. In the early stages of the EMU, the traditional high inflation countries continued to run higher than allowed inflation. Germany ran an extra low pace to compensate and to keep the EMU pace ‘on-target.' Eventually the excessive inflation countries had their lack of discipline catch up to them as the great recession took them down and as the EU enforced the Maastricht rules. Pain and suffering resulted as Spain, Portugal, Italy Ireland and Greece ran austerity programs. Italy's austerity was so great that it still has not gotten its GDP back to its pre-recession level! So with austerity imposed, it had appeared that the Germans and their tight money ways won and the loose-spending Southern European countries were brought to heel. Currently, Italy with annual inflation at 0.4% has one of the lowest rates in the EMU. But now the foot is in the other shoe. Europe is weak. It has been very weak. The ECB is undershooting its just less than 2% price ‘objective.' Dutch central banker Klass Knot wants to replace this inflation rule with one that will impose a symmetric inflation band. Of course a band of 2.5% to 1.5% would still leave EMU inflation too low (as it is running at a 0.8% pace). Knot, of course, from the tight money faction of the ECB, would like to use this wider band to stop the ECB's stimulus and negative rate programs in their tracks. But one wonders how the Dutch and Germans would react to inflation running at 2.4% for some time. There is something in a band for everyone but only in its time. Europe may be one of the best examples of the fallacy of composition. The policy that worked so well for Germany on its own did bring the rest of Europe to heel, but now it is creating unexpected problems.

Continued head-bumping

I continue to view these sorts of inflation and monetary policy preferences as somewhat sociologically determined. I am not at all surprised to see that Europe is having a hard time when it tries to operate like Germany does. Spain is not Germany. Nor is Portugal… and so on. Germany would not fare well in a high inflation environment either, for that matter. But the EMU has put these countries together. New EU members have to also be aspiring to be EMU members. I don't understand this requirement because customs union membership on its own does not require such a step. But Europe and the EMU still face challenges and they continue to harbor the same underlying resentments. The Germans and Dutch seem to have thought that there was a range for inflation ranging from just less than two percent to negative infinity! The rest of the EMU did not sign on for that they want policy to react to ‘too-low' inflation as well. The two sides still have not sorted that one out.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief