Global| Jan 20 2006

Global| Jan 20 2006Second Mortgages

by:Tom Moeller

|in:Economy in Brief

Summary

Worry that some potential bursting of the "bubble" in housing market valuations at least in part rests on the idea that homeowners are borrowing against those "inflated" values to support current spending. In fact, real spending [...]

Worry that some potential bursting of the "bubble" in housing market valuations at least in part rests on the idea that homeowners are borrowing against those "inflated" values to support current spending.

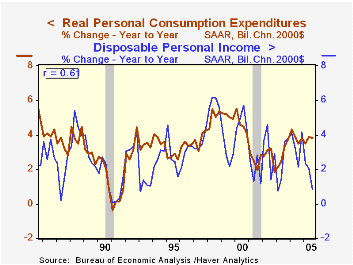

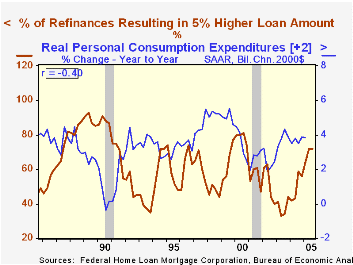

In fact, real spending growth of 3.8% over the last year vastly exceeded the growth in real disposable income of 0.8%; prima fascia evidence of unaffordable profligate spending? And Freddie Mac (FMAC) reported that in 3Q05, mortgage "cash out" refinancing activity rose to the highest level (72%) since 2000. An increased percentage of homeowners increased their loan amounts by 5%.

Over the last twenty years, however, it didn't take some real estate bubble to generate these conditions. Today's cash out refinancing may be nothing other than what previously was termed a second mortgage. And this pejorative terminology was used when economic times were about to weaken.

Since 1985, the correlation between the level of cash out refinancing and the change in real consumer spending has been a statistically significant negative 40%. The correlation with spending on durables has been an even higher -57%. A piece of that spending surely was supported by the second mortgage, but the more likely rationale for spending growth has been income.

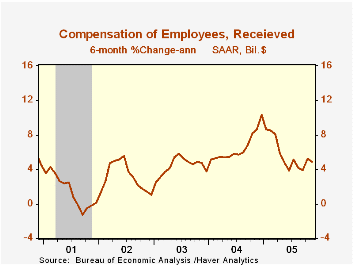

Real compensation growth has suffered due to the latest rise in inflation and also the comparison to what was heady growth late in 2004. Most recent growth in compensation, however, has been encouraging as improved job creation has held nominal compensation growth at 5%, and inflation pressure has abated somewhat.

Will that be enough to forestall a crash in spending tied to burst housing market valuations? For many, no, but for most the future decision to spend will depend on the fundamentals of income and employment.

House of Cards from the Federal Reserve Bank of Richmond can be found here.

Cash-Out Refinancing: Check It Out Carefully from the Federal Reserve Bank of St. Louis is available here.

Has the Housing Boom Increased Mortgage Risk? from the Federal Reserve Bank of Dallas can be found here.

| Freddie-Mac Cash Out Refinance Activity | 3Q05 | 2Q05 | 3Q04 | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| 5% Higher Loan Amount | 72% | 72% | 59% | 50% | 38% | 52% |

| Median Appreciation of Refinanced Property | 23% | 23% | 17% | 11% | 7% | 16% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief