Global| Aug 25 2006

Global| Aug 25 2006Monetary Policy's Posture: Many "Buts"

by:Tom Moeller

|in:Economy in Brief

Summary

The dissenting opinion at the last FOMC meeting from Richmond Fed Bank President Lacker no doubt reflected more than a concern that economic growth was still too robust to be consistent with moderate inflation, but that various [...]

The dissenting opinion at the last FOMC meeting from Richmond Fed Bank President Lacker no doubt reflected more than a concern that economic growth was still too robust to be consistent with moderate inflation, but that various measures of liquidity (money) growth needed further restraint.

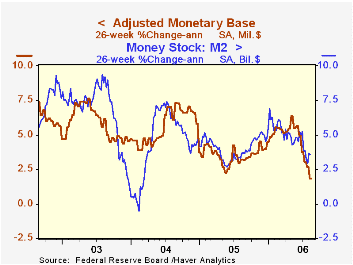

Indeed, liquidity growth has slowed. Six-month growth in the monetary base near 2% (AR) is off the 6% highs, but M2 has not slowed as precipitously and recently has picked up some.

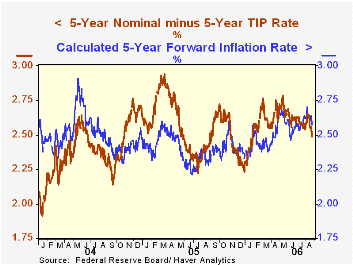

The 5-Year TIPS spread is down, but only to the middle of the range of the last year and the futures market is indicating that the forward inflation rate is in a rising trend.

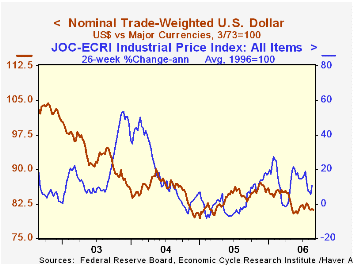

The dollar's value received some lift as the Fed was tightening, but the inkling and then the reality of a pause in the process recently caused the dollar's foreign exchange value to fall back near the bottom of its 18 month range.

Commodity prices. They've had some lift due to higher oil prices and the industrial economy's recovery but the patterns showing strength have been uneven, and these prices in the past have been better indicators of real activity than of inflationary pressure.

Inflation expectations as measured in the University of Michigan survey rose in August to 4.9% for the next twelve months, up off the 2.5% lows of the 2003, but down from last year's highs of 5.5%.

The effects of globalization on inflation and their implications for monetary policy: a speech by Fed Vice Chairman Donald L. Kohn is available here.

The long run benefits of sustained low inflation from the Federal Reserve Bank of St. Louis can be found here.

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief