Global| Oct 02 2019

Global| Oct 02 2019Japan's Tankan Survey Weakens

Summary

Japan's Tankan survey weakened in Q3 as did the outlook for Q4. The only ‘saving grace' in this report is that despite widespread weakness it had been expected to show even greater slippage. This is a very comprehensive and closely [...]

Japan's Tankan survey weakened in Q3 as did the outlook for Q4. The only ‘saving grace' in this report is that despite widespread weakness it had been expected to show even greater slippage. This is a very comprehensive and closely watched survey in Japan. The survey is segmented into three main parts, large companies, medium-sized companies and small companies. The large company survey is the one that is stressed and it is the performance of manufacturing firms that is considered the economic bellwether. And that is the weakest part of the survey this quarter.

Japan's Tankan survey weakened in Q3 as did the outlook for Q4. The only ‘saving grace' in this report is that despite widespread weakness it had been expected to show even greater slippage. This is a very comprehensive and closely watched survey in Japan. The survey is segmented into three main parts, large companies, medium-sized companies and small companies. The large company survey is the one that is stressed and it is the performance of manufacturing firms that is considered the economic bellwether. And that is the weakest part of the survey this quarter.

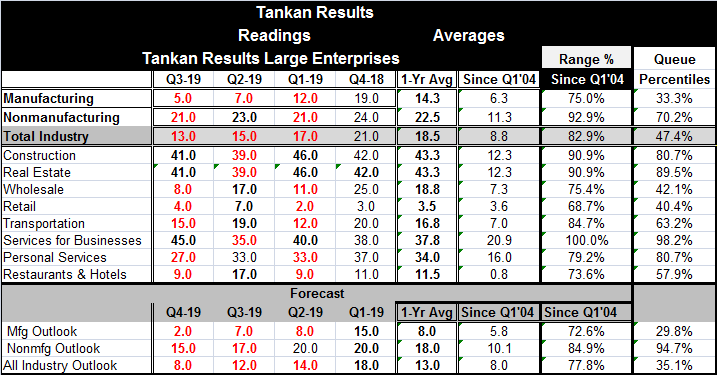

Japan's tankan index for Large Manufacturing Companies (LMCs) saw its index fall to 5 in Q3 from 7 in Q2. That follows readings of 12 in Q1 2019 and of 19 in Q4 2018. From Q4 2017, this Tankan reading has been at the same level or lower quarter-to-quarter, marking 7 quarters of ongoing decline. In Q4 2017, the reading was 25, but it was 19 as recently as Q4 2018. While the slippage is somewhat long lived, the bulk of the weakness has comes in 2019 as the trade wars have arrived and intensified.

That finding is echoed by the fact that the outlook (which extends though Q4 2019) has five straight quarters of slippage for LMCs with peak optimism for this period at 21 in Q3 2018. The outlook reading shows four points of slippage from Q4 2018 to Q1 2019, then seven points of slippage in Q2, a thin one-point slippage in Q3, followed by a five-point slippage in Q4. The dynamic seems very much linked to the issues and escalation of the U.S.-China trade war.

The graph shows the ongoing slippage in the outlook for large companies by sector. The weakness is clearly being led by manufacturing and spread from there. That sequence also argues for the trade war, which impacts goods by threatening the trade in goods, as the culprit. In Q3, wholesaling has been hit the hardest among service sector industries followed by restaurants & hotels, transportation and retail, judging from month-to-month changes. However, in terms of month-to-month changes manufacturing only worsened by 2 points in Q3 after worsening by five points in Q2.

Another measure of how impacted sectors are is the queue percentile standing. This metric ranks each industry or sector in its own time-series of results. On that basis, manufacturing is the weakest with a 33.3 percentile standing. Nonmanufacturing as a whole is still quite solid at a 70.2 percentile standing. But within nonmanufacturing, retailing is weak at 40.4 percentile standing. Any standing below its 50% mark is a result that is below that industry's own median. Wholesaling is also weak with a 42.1 percentile standing.

However, the nonmanufacturing and service sector also has some heat. Services for businesses are holding the highest level of activity for the entire period from Q1 2004. Construction and real estate also have high percentile standings in their respective 80th and 89th percentiles. Personal services have an 80th percentile standing. Restaurants and hotels as well as transportation sectors have more modest but still firm rank standings.

The outlook reflects this same disparity. The manufacturing outlook that fell sharply this month has a 29th percentile standing, well below its median. But nonmanufacturing has a 94th percentile standing, still quite firm. Despite the downgrade in the outlook by manufacturers, the nonmanufacturers are much more buoyant in their outlook. Similarly, the outlooks for nonmanufacturing in medium and small firms continue to have 72nd to 88th percentile standings – still quite high. And the manufacturing vs. nonmanufacturing outlooks for smaller establishments are mixed. For medium-sized firms, the nonmanufacturing outlook stands at the 88.5 percentile mark, stronger than for manufacturing. For small firms, the outlook for manufacturing is reversed and the outlook is better than for nonmanufacturing with an 82.8 percentile standing for the manufacturing sector, about 10 percentile points above the outlook for nonmanufactures.

The Bank of Japan is still having a hard time moving the needle on inflation expectations. The expectation for one year ahead is 0.9% and over five years it is for 1.1%. These expectations fall short of the BOJ's objective for 2% inflation. Despite myriad of plans and actions, the BOJ still can't convince firms that it will be able to achieve 2% inflation over the next half-decade.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief