Global| Dec 28 2005

Global| Dec 28 2005Japan's CPI: Firming or Still Soft?

Summary

Japan's Statistics Bureau in the Ministry of Internal Affairs and Communications (MIC) yesterday reported consumer prices for November. Generally, these prices seem to be working their way into an upturn, but the extent of this [...]

Japan's Statistics Bureau in the Ministry of Internal Affairs and Communications (MIC) yesterday reported consumer prices for November. Generally, these prices seem to be working their way into an upturn, but the extent of this firming trend depends on the price measure being applied and what time comparison is being used.

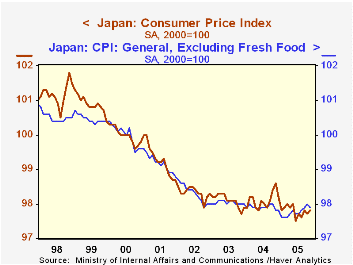

The total index, the so-called General CPI, continues to decline on a year-over-year basis. In November it was 0.8% below November 2004, the weakest change since October 2002. Seasonally adjusted and compared month-to-month, however, it looks to be stabilizing: it has actually increased from 97.5 in June to November's 97.8.

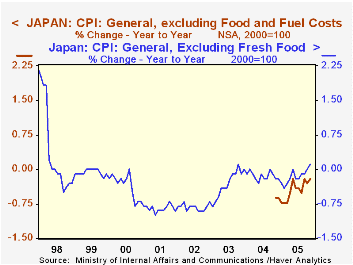

As in many other countries, a "core" rate is used for government policymaking and investment planning. Core rates are supposedly less volatile that total indexes and are defined to exclude items where supply forces predominate. So their movements reflect such non-economic events as bad weather, war and possibly political priorities, not so much market influences. Up to now in Japan, the "core" has been the general index less fresh food. This latter item is clearly more subject to weather and seasonal forces than to consumer demand pressures. The subset of the CPI excluding fresh food has been deemed the most useful for monetary policy focus. Thus, yesterday [overnight in Western markets between Monday and Tuesday] the November report made news when this core index rose on a year-to-year basis for the first time since October 2003 and for only the second time since the spring of 1998. On a month-to-month basis, this index too has been rising over the course of this year, suggesting that the year-to-year pattern could stay positive. At least one news account reported that some investors were beginning to look for a change in the Bank of Japan's current "quantitative monetary easing" as this price trend might be sustained during 2006.

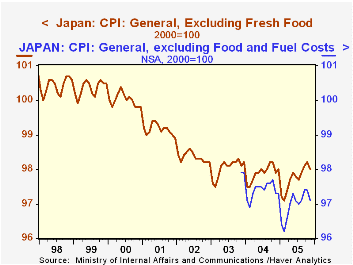

At the same time, with this release, the MIC has introduced still another core rate, one similar to those used elsewhere which exclude both food and energy products. Haver Analytics added this new series to the JAPAN database just this morning. Only two years of history are available, running back to November 2003, so these data are not yet seasonally adjusted. This price measure is still going down. In the month from October, the index fell from 97.4 to 97.1, which in turn is off 0.2% from November 2004. The earliest levels, in November and December 2003, were 97.9. So it appears that the pick up in the standard core rate may be due to energy, and when that is excluded, general prices remain soft. Among various "subgroups" of prices, clothing has risen for well over a year and furniture has edged up just the last three months. Housing costs and reading and recreation appear to be stabilizing after long downward paths. Thus, while the pace of deflation has surely slowed, it is hard to read any threat of renewed inflation into this price behavior.

At the same time, the Japanese economy itself is firming. Today, for example, METI reported that industrial production for November was up 1.4% from October, a fourth consecutive monthly advance after some hesitation in the spring and early summer. So forces may be developing for more sustainable growth and firmer prices in Japan, but the mixed behavior of the various CPI measures leaves implications for monetary policy fairly vague at the present time.

| Japan CPI (2000=100) | Nov 2005 | Oct 2005 | Sept 2005 | Year Ago | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|---|

| General CPI, SA | 97.8 | 97.7 | 97.8 | 98.6 | 98.1 | 98.1 | 98.3 |

| Yr/Yr % Change, NSA | -0.8 | -0.7 | -0.3 | -0.0* | -0.3* | -0.9* | |

| Gen CPI ex Fresh Food, SA | 97.9 | 98.0 | 97.9 | 97.8 | 97.9 | 98.0 | 98.3 |

| Yr/Yr % Change, NSA | 0.1 | 0.0 | -0.1 | -0.1* | -0.3* | -0.8* | |

| Gen CPI ex Food & Fuel, NSA | 97.1 | 97.4 | 97.4 | 97.3 | 97.4 | [97.9**] | -- |

| Yr/Yr % Change, NSA | -0.2 | -0.3 | -0.2 | -0.6* | -- | -- |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief