Global| Feb 17 2006

Global| Feb 17 2006Japan GDP Grows 5.5% in Q4; Shows Biggest Yearly Gains in 9 Years

Summary

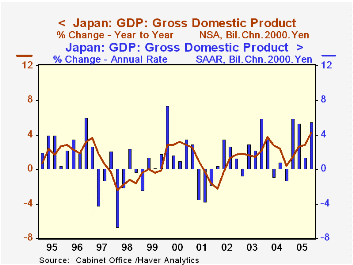

Japan's GDP grew at a 5.5% annual rate in Q4, making three strong quarters during 2005 and bringing the Q4/Q4 growth to 4.2%. Calculations of GDP have changed in recent years, so long history is not available on this same basis, but [...]

Japan's GDP grew at a 5.5% annual rate in Q4, making three strong quarters during 2005 and bringing the Q4/Q4 growth to 4.2%. Calculations of GDP have changed in recent years, so long history is not available on this same basis, but this Q4/Q4 advance is likely the strongest performance of the Japanese economy since about 1990. Moreover, the recent range of growth is similar to the magnitudes of the halcyon period of the late 1980s. [Note that "real GDP" is now defined in chain prices, but is available only since 1994. Fixed-weight GDP is available back to 1980, but Q4 on this basis will not be published until after the second release next month of the chained Q4 data. So exact information on these historical comparisons is not yet available.]

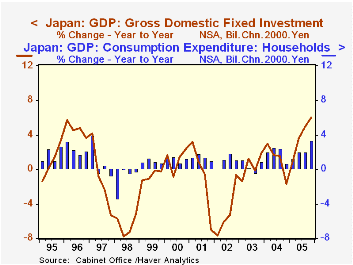

In Q4, household consumption grew at a 3.2% pace; this wasn't the highest of the year, but it brought the four-quarter growth to 3.3%, which was the highest since Q1 1997 (4.0%). The year 2005 as a whole saw 2.2% consumption growth, the largest since 1996. Similar comparisons apply to investment outlays (fixed capital formation): four-quarter growth of 6.0% is indeed the strongest since the current "official" GDP series begins in 1994, and the yearly total of 3.9% is the largest since 4.7% in 1996. [The good gains in 1996, it might be noted, were marked by substantial anticipatory buying ahead of an increase in Japan's consumption tax, so growth then was stimulated somewhat artificially, unlike the present, more fundamental progress.]

Net exports made a major contribution to Q4 GDP, with a continuing double-digit pace (annualized) for growth in exports, 13% in the quarter, the third consecutive such increase. Imports declined in chain-price terms, due to a substantial increase in import prices.

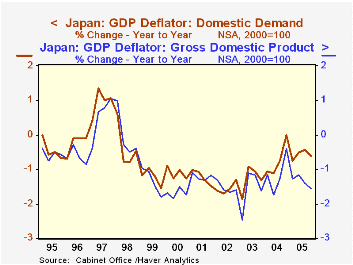

We have noted here several times recently that various price measures in Japan have started to stabilize following their long bout of deflation. The GDP deflator and other related price aggregates in the national accounts are still generally falling, though, as seen in the accompanying graph. However, in the latest quarter the role of that surge in import prices is evident as the total deflator is off 1.6% from a year earlier, but that for domestic demand (which nets out exports and imports) is down "only" 0.6%. But the increasing vigor of domestic demand suggests the possibility of reflation of the Japanese economy. In fact, investors picked this element to focus on in the wake of the better-than-expected growth report. Stock prices fell as investors evidently interpreted the good growth as a sign that the Bank of Japan's liquefying monetary policy might be shifted to a less accommodative stance.

| Japan (SAAR, %) | Q4 2005 | Q3 2005 | Q2 2005 | 2005 | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|---|

| Total GDP | 5.5 | 1.4 | 5.4 | 2.8 | 2.3 | 1.8 | 0.1 |

| Household Consumption | 3.2 | 1.7 | 3.3 | 2.2 | 1.9 | 0.4 | 1.0 |

| Gross Domestic Fixed Capital Formation | 4.3 | 6.1 | 5.9 | 3.9 | 1.0 | 0.5 | -5.0 |

| Exports | 13.0 | 12.6 | 14.6 | 6.7 | 13.9 | 9.0 | 7.5 |

| Imports | -5.1 | 13.5 | 9.0 | 6.1 | 8.5 | 4.0 | 0.8 |

| Domestic Demand | 3.2 | 1.3 | 4.6 | 2.6 | 1.5 | 1.2 | -0.6 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief