Global| Jul 01 2002

Global| Jul 01 2002ISM Index Rose Further

by:Tom Moeller

|in:Economy in Brief

Summary

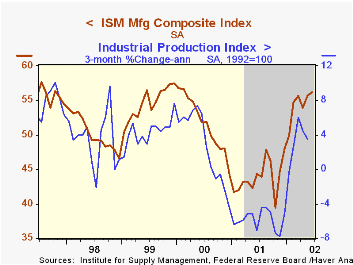

The ISM Composite Index of manufacturing sector activity rose slightly more than expected last month. Consensus expectations were for a slight decline to 55.5. Higher production, employment and vendor performance (slower deliveries) [...]

The ISM Composite Index of manufacturing sector activity rose slightly more than expected last month. Consensus expectations were for a slight decline to 55.5.

Higher production, employment and vendor performance (slower deliveries) fueled the gain in the composite index to its highest level since February 2000.

The new orders index fell but has remained in a relatively high range since earlier this year.

Inflation pressure rose sharply as the percentage of companies reporting lower prices fell to the lowest since August 2000. The percentage of companies reporting higher prices rose to the highest since April 2000.

Over the last twenty years there has been a 66% correlation between the ISM Composite Index and quarterly growth in chained GDP.

| ISM Manufacturing Survey | June | May | Y/Y | 2001 | 2000 | 1999 |

|---|---|---|---|---|---|---|

| Composite Index | 56.2 | 55.7 | 44.3 | 43.9 | 51.6 | 54.6 |

| Prices Paid Index | 65.5 | 63.0 | 42.8 | 43.0 | 64.8 | 54.2 |

by Tom Moeller July 1, 2002

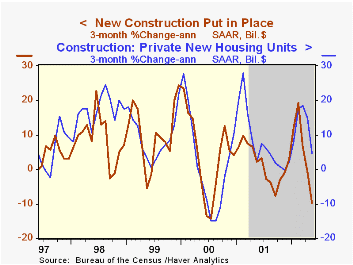

The value of construction put in place fell unexpectedly in May. A slight gain had been expected. It was the second decline in three months following hefty gains in January and February. Figures were revised back to 1999. Growth in 2001 was lowered substantially in all sectors.

Residential building fell for the first month since October. Activity is up 7.4% versus last year and has been strongest in the multi-unit sector.

Nonresidential building activity fell sharply for the third month this year, continuing a trend of decline that began last year. Industrial and office building has fallen notably but has been offset somewhat by gains in the hospital and educational areas.

Spending by governments rose for the fourth month this year driven by gains in the education and military sectors.

| Construction Put-in-place | May | April | Y/Y | 2001 | 2000 | 1999 |

|---|---|---|---|---|---|---|

| Total | -0.7% | 0.4% | 0.6% | 2.5% | 7.3% | 8.7% |

| Residential | -0.8% | 0.4% | 7.4% | 3.3% | 7.4% | 11.2% |

| Nonresidential | -3.1% | 0.1% | -14.4% | -3.1% | 7.1% | 1.9% |

| Public | 1.9% | 0.1% | 3.1% | 7.4% | 5.4% | 10.6% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief