Global| Jun 07 2006

Global| Jun 07 2006Inflation Expectations Rise

by:Tom Moeller

|in:Economy in Brief

Summary

Inflation expectations were piqued this week by Fed Chairman Bernanke's comments that the three-month and six-month core PCE inflation figures at 3.0% and 2.3% were "unwelcome developments." As a result, the yield on the inflation- [...]

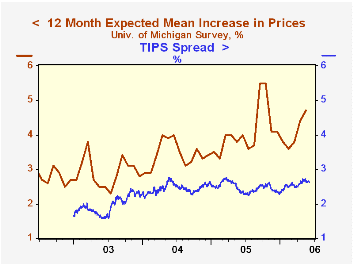

Inflation expectations were piqued this week by Fed Chairman Bernanke's comments that the three-month and six-month core PCE inflation figures at 3.0% and 2.3% were "unwelcome developments."

As a result, the yield on the inflation-protected Treasury note rose to 2.44% from 2.40% on Monday but the yield on the nominal security fell to 5.01%. The so called TIPS spread narrowed to 2.57% from 2.62% on Monday.

Bernanke's comments implied that more inflation pressure existed than had been perceived but that the Fed would combat those pressures more forcefully than previously expected.

The rise in the TIPS spread this year has followed a rise in 12 month inflation expectations to 4.7% in May from 3.8% in January, as surveyed by the University of Michigan.

Inflation Expectations: How the Market Speaks from the Federal Reserve Bank of San Francisco is available here.

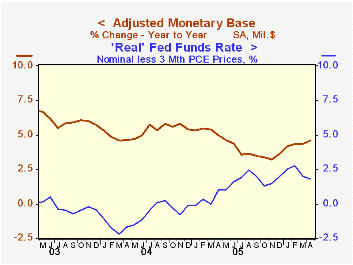

How much work the Fed still must do to contain inflation is the $64,000 question. Already it has lifted short term interest rates by 400 basis points to 5.0%. More action might be suggested, however, by a recent pickup in the y/y growth of the monetary base (liquidity) to 4.6%. It had slowed previously to 3.2% from 5.8% late in 2004. In addition, the "real" Fed funds rate fell as the three month growth in "core" PCE prices tripled to 3.0% in May versus last August.

The Shadow Open Market Committee can be visited here and its Policy Statement from May, 2005 can be found here.

| Treasury Inflation Indexed Securities | 06/06/06 | 06/05/06 | 12/31/05 |

|---|---|---|---|

| 10 Yr. Treas. Note at Constant Maturity Due 1/15/16 | 2.44% | 2.40% | 2.06% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief