Global| Dec 18 2008

Global| Dec 18 2008IFO Index Drops

Summary

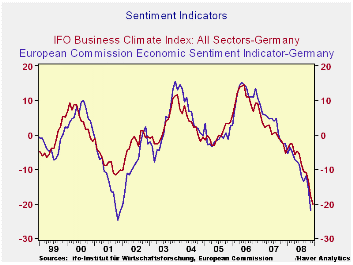

The IFO index fell to 82.6 in December from 85.8 in November. The current situation index fell to 88.8 in Dec. from 94.9 in Nov. Business expectations decreased to 76.8 from 77.6. The IFO index is much weaker in 2008 than it was in [...]

The IFO index fell to 82.6 in December from 85.8 in November.

The current situation index fell to 88.8 in Dec. from 94.9 in Nov.

Business expectations decreased to 76.8 from 77.6. The IFO index is

much weaker in 2008 than it was in 2001. But the EU sentiment index is

only about as week in 2008 as it was in 2001.

The all –sector reading of the IFO is weaker than any

individual sector in terms of its position in its range. That result is

a testament to how this crisis is leaving no sector untouched.

Construction is the best relative performing sector as it stands in the

39th percentile of its range. This is mostly because construction has

remained weak in recovery. The next strongest sector is wholesaling at

a -21.8 net reading. At that it stands in the bottom quarter of its

range. The service sector, the most stable of them all, registers a raw

net reading of -7.3 but that resides in the bottom 18 percentile of its

range. Retailing and MFG are in, roughly, the bottom 10 percent of

their respective ranges, since early 1991.

The IFO is showing great weakness and the detailed readings

(not yet available) for December have been showing more weakness in the

important export sector. The IMF is urging Germany to do more to

stimulate its economy. The German economics ministry is cutting its own

outlook for growth. It said: "The outlook for the economic development

has deteriorated further. The weakening of the world economy will be

stronger than previously assumed. At the same time, the situation on

international financial markets is still severely strained," the German

economics ministry continued in its December monthly report to discuss

the outlook. "The outlook for the export-driven German economy is

gloomier." It said economic indicators are signaling that that the

contraction of real gross domestic product, which was down 0.5% in the

third quarter, has probably continued at a faster pace and there is no

sign of any change in the weakening trend.” This of course is exactly

the message from the day’s IFO report, too.

| Summary of IFO Sector Diffusion readings: CLIMATE | ||||||||

|---|---|---|---|---|---|---|---|---|

| CLIMATE Sum | Current | Last Mo | Since Jan 1991* | |||||

| Nov-08 | Oct-08 | average | Median | Max | Min | range | % range | |

| All Sectors | -29.0 | -20.2 | -7.7 | -8.4 | 16.9 | -30.9 | 47.8 | 4.0% |

| MFG | -29.6 | -18.9 | -0.2 | 1.6 | 27.0 | -35.9 | 62.9 | 10.0% |

| Construction | -30.2 | -27.7 | -28.2 | -30.3 | 1.3 | -50.5 | 51.8 | 39.2% |

| Wholesale | -21.8 | -15.1 | -13.2 | -15.7 | 23.6 | -39.3 | 62.9 | 27.8% |

| Retail | -33.5 | -25.1 | -14.2 | -14.5 | 28.7 | -39.7 | 68.4 | 9.1% |

| Services | -7.3 | -4.3 | 11.0 | 9.5 | 28.5 | -15.2 | 43.7 | 18.1% |

| * June 2001 for Services | ||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief