Global| Jun 24 2008

Global| Jun 24 2008IFO Business Sentiment Reading is Still Sinking

Summary

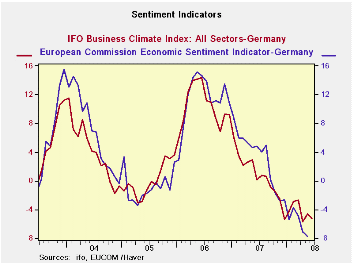

At the crossroads The IFO business sentiment reading made a deeper Yr/Yr drop in June than in May. It has slipped to the 68th percentile of its range of values (range from 1992 to date). The current situation is not as glum a reading [...]

At the crossroads

The IFO business sentiment reading made a deeper Yr/Yr drop in June

than in May. It has slipped to the 68th percentile of its range of

values (range from 1992 to date). The current situation is not as glum

a reading as it stands in the 78th percentile of its range; it is

hardly beleaguered. Yet, it slipped in the month and was lower by 2.8%

Yr/Yr, a bigger drop than May’s 2.1%. But it is the all-important

expectations index that by its very nature is more forwarding looking

and that is a cause for distress. This index fell by 7.9% Yr/Yr more

than the 7.1% registered in May. Its June level stands at the 50.9th

percentile of its range almost exactly mid range. The German economy is

at the crossroads.

The diffusion values show widespread slippage in June with

each of the major sectors lower in June than in May except for

construction. The all-sector climate diffusion index stands at 1.7 down

from 6.1 in May. It stands at the 85.2 percentile much like its pure

index counterpart listed in the table above which is in its 68th

percentile. The sector detail from diffusion data is the only sector

detail available for now.

Climate by sector slipped to 8.2 from 15.0 in MFG dropping

climate to the 61st percentile of its range. Construction is an odd

case at a -18.9 actually stronger than May’s -20.2 and standing in the

74th percentile of its range. Despite the poorer absolute performances

the construction sector is doing relatively better than MFG.

Wholesaling index slipped to 2.1 from 4.0 falling to the 66th

percentile of its range. Retailing registered a weaker -6.5 compared to

-4.4 in May, a range reading of the 80.9 percentile again, an

absolutely weaker sector with a relative standing that is better than

the group average. Services fell to a +16.3 diffusion reading from

+19.4 in May for a percentile standing of 72.4.

Since these are diffusion readings and span positive and

negative values we cannot express drops from their peaks very

effectively. But in terms of the range percentiles we can give some

idea of the slippage. Most of these series peaked in Early 2006 or late

2007. Over this period each was at its own respective cycle high 100th

percentile. So each index has fallen from 100% during this period to

its current reading. These are large drops over a span of 18-months or

less.

The net changes in these various indices the over 18-months

are about half as large as the largest 18-month dropped ever

experienced for all sectors for MFG and for wholesaling. For consumers

the last 18 month’s drop is only one-quarter on the largest ever. For

retail sales and services the drop is on the order of the fifth to

tenth percentile of the largest drop. In terms of monthly variation the

all-sector reading is 17% more variable over the past 18months than

what is normal MFG is 11% more variable. Wholesaling is has been more

variable. But construction has been 20% less variable retailing has

been 15% less variable. Services overall have been 35% less variable.

It has been a bit of a mixed bag but the German consumer and services

sector has been clearly eroding but slowly while MFG has been slipping

more rapidly.

What we have is an economy in transition with most of the

transition coming from manufacturing and wholesaling (trade). The

domestic retail construction and services industries aren’t really hit

that hard although they have been slipping. With banks seeing some

financial stress and turmoil we have to wonder how long before real

estate gets hit since it is a troubled sector internationally and

requires bank financing in most circumstances. Manufacturing shows

weakness and the euro remains strong; how long before it begins to

affect the consumer and services sectors? What of the eroding impact on

the consumer of higher oil prices? The RTC/Reuters indices already how

a bigger hit to services that does the IFO reading. Ultimately, it’s a

question of contagion from a weaker MFG sector and a direct hit from

oil.

| IFO Survey: Germany | ||||||||

|---|---|---|---|---|---|---|---|---|

| Percent: Yr/Yr | Index Numbers | |||||||

| Jun-08 | May-08 | Apr-08 | Mar-08 | Feb-08 | Current | Average | %tile | |

| Biz Climate | -5.3% | -4.6% | -5.7% | -2.7% | -2.8% | 101.3 | 96.1 | 68.6% |

| Current Situation | -2.8% | -2.1% | -4.2% | -0.7% | -1.1% | 108.3 | 95.4 | 78.0% |

| Biz Expectations: Next 6-Mos | -7.9% | -7.1% | -7.2% | -4.7% | -4.4% | 94.7 | 97.0 | 46.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief