Global| Apr 17 2015

Global| Apr 17 2015Has EMU Austerity Been a Success or Failure?

Summary

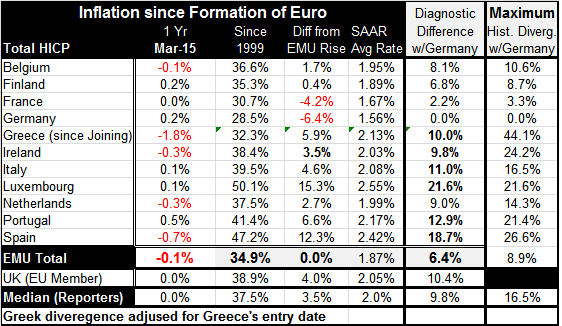

The EMU-wide harmonized index of consumer prices (HICP) fell again in March, marking the fourth consecutive month in which the price index has fallen. Looking at the earliest EMU members that have reported data (in the table below), [...]

The EMU-wide harmonized index of consumer prices (HICP) fell again in March, marking the fourth consecutive month in which the price index has fallen. Looking at the earliest EMU members that have reported data (in the table below), prices fell in five of these 11 countries in March.

The EMU-wide harmonized index of consumer prices (HICP) fell again in March, marking the fourth consecutive month in which the price index has fallen. Looking at the earliest EMU members that have reported data (in the table below), prices fell in five of these 11 countries in March.

If you direct your attention to the final two columns in this table, you will focus on two interesting statistics. The final column memorializes the greatest price level difference between each country vs. Germany since the EMU was formed. We calculate this using the difference in cumulative percentage price level changes from initial price levels when the EMU was formed. What we see is that current divergence (the second to the right column) is much diminished compared to maximum divergence everywhere except Luxembourg which is a financial center. This tells us austerity has been `working.'

These divergences have been coming down rapidly in the wake of the financial crisis and the imposition of austerity. Austerity has been a huge burden on many EMU members. The goal of austerity is to get each country living within its means by controlling fiscal deficits and debt relative to GDP. But the easiest manifestation to see of excessive fiscal policy stimulus is the extent to which inflation rates among member countries have risen above the rate for fiscal-conscious Germany.

Before 2003, Germany almost always had the lowest inflation among all the EMU nations. From 2004 to early 2008, that shifted slightly. However, after the financial crisis and recession, Germany more rarely became the low inflation country. This was because of austerity. Before the crisis, Germany averaged a year-over-year inflation rate that was only 0.6 percentage points higher than the member with the lowest rate (a designation that changed constantly, of course). But after 2007 the German rate began to average 1.8 percentage points MORE than the lowest EMU member - that is a huge shift. While the pace of German inflation has been more or less the same, the pace among some other countries has plunged to the negative to create such a huge AVERAGE gap.

After the crisis and the imposition of austerity across the euro area, countries that experienced austerity ran into trouble trying to maintain growth and as a result of weak growth inflation was battered lower. Still, German inflation before the crisis averaged 1.5% per year and after the crisis it has averaged 1.6% per year (although now all inflation rates across the euro area are lower). But in March 2015 the German year-over-year inflation rate is tied for ninth in a group of 11 early EMU members. so much for Germany usually being the lowest.

Countries wanting to regain their competiveness (reduce the value of the second to the last column in the table to zero) have to run lower rates of inflation than low-inflation Germany. And that is what has happened as the gap between German inflation and the lowest inflation in EMU post-crisis has surged. While current prices in the EMU reflect the lingering impact of lower oil prices, there is still an ongoing effect from austerity.

When Europe launched this policy of austerity, I was very skeptical of its potential for success because Germany is such a persistent low-inflation country. It was clear that countries trying to regain competitiveness lost to Germany over the early years of the EMU under a common currency would have a tough job since Germany was destined to continue to run low inflation rates (which it in fact has done). It meant that countries wanting to make competitiveness gains would have hold their annual price level gain near zero or below it. This of course would mean a great deal of pain for citizens and, if it were to go on for long, would likely create political backlash and potentially, instability. In the event, we have seen all of that play out in terms of domestic discord in each of the countries undergoing austerity. Only France has been able to violate debt constraints and get off with an extension of the period to hit them. And since fiscal austerity often meant growth was weaker than expected and that tax revenues fell short and debt-to-GDP targets were missed, austerity `fed on itself' for a while.

But everywhere in the euro area countries have cobbled together austerity-minded governments and found a way to deal with domestic discord. Presently only Greece, the country with some of the biggest gaps to make up, is hanging in the balance of staying or succumbing to domestic pressure to jettison its austerity promise.

But look at Greece! Its price level once had risen by 44% more that Germany's from the start of its joining the EMU. It now is only 10% higher. Greece has made enormous gains and done so at enormous costs, explaining why Greek discord is so high. Spain, which once had a cumulative price gap with Germany of 27% has narrowed that to 19%. That's good progress, but nothing like what Greece has done. Spain's unemployment rate, like that in Greece, is also extremely high. But Spain is more stable and staying on plan.

The ultimate success and failure of austerity will depend on whether price differences can be brought into close enough alignment. It will also depend upon whether member nations can stay together as this process evolves. New vigilance on debt-to-GDP ratios and on fiscal deficits is more likely to make gains remain in force. Excluding Luxembourg, a country that does not compete with industry in other member nations because of its financial focus, only Spain has a cumulative price divergence with Germany that is substantially greater than 10%. Portugal is at a divergence of 13%. After that, the maximum divergence is Italy at 11%. Five member nations have divergences with Germany that are in single digits.

As the euro falls in value, it is useful to keep these divergences in mind. Note that only Germany and France (due to their performance and their large weights in the EMU) have cumulative price level gains less than that for the EMU as whole. For these two countries, their individual competiveness on world markets is greater than the EMU as a whole (by about 6% for Germany and 4% for France). For a country like Spain, its competitiveness is about 18% worse that the EMU average.

The European Central Bank runs one monetary policy for all of the EMU. There are few instances of individual national divergences (and these are closely watched). Perhaps in its bond buying program, it buys more bonds of one country than in another or it assists one central bank a bit more with liquidity. But these differences are small. For the most part, national regulations and fiscal differences create rigidities or stimulus that account for inflation differences across regions.

Of course there are huge cultural differences that may never be bridged. Germans are German and the French are French, and so on. There are language and cultural differences that simply will always make labor less than mobile in the EMU than in, say, the U.S. But with mobile capital flows across the region, a good deal of harmonization can still be achieved. How much harmonization evolves will be up to the member countries themselves. So far, austerity- painful as it is- has succeeded beyond what I thought might be possible. While substantial progress has been made, risks still abound. Europe is not out of the woods. And Greece may be the biggest test of this program. If there is a Grexit, it will be interesting to see if European markets remain as placid in the aftermath as they are now in the run up to this potential disaster.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief