Global| Aug 07 2008

Global| Aug 07 2008Germany's Weakness in IP Does Not Stand Alone

Summary

Weakness in industrial output is now a growing EU-wide phenomenon based on the large countries’ results. Among the early reporting large countries Germany, Italy and the UK show negative growth rates for real output in 2008-Q2. Only [...]

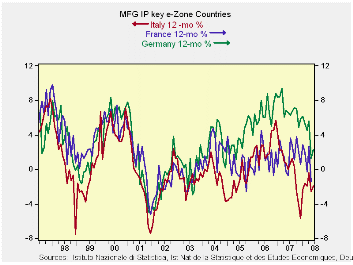

Weakness in industrial output is now a growing EU-wide

phenomenon based on the large countries’ results. Among the early

reporting large countries Germany, Italy and the UK show negative

growth rates for real output in 2008-Q2. Only Spain with an

exceptionally wild output series shows a gain in Q2 and that is after

seeing output lower over six months and over 12-months.

Frances results are plotted in the chart above but they lack a

timely update for June. Still the pattern in output is clear. Germany

is having the sharpest current drop. Italy has had the longest period

in which output has been declining (Yr/Yr). France had not had the

degree of output success of the others earlier in the expansion. It has

showed better resilience to declining forces than Italy over the past

year and has only just dropped to show Yr/Yr declines in output.

The services sectors of these countries are showing weakened

performance as well although the monthly report for EMU showed a bit of

resilience. Inflation still dogs Europe – regardless of the domain of

the central bank.

While the authorities in Japan have just opened the door to admitting

weakness and have gone so far as to admit that the economy could be in

recession even now, in the Europe a certain confidence is still exuded,

but by increasingly cautious policymakers. Today, German banking

association president Klaus-Peter Mueller said that there is no end in

sight for financial crisis. 2008 will remain a difficult year for all

banks he says. With banks so impeded and the ECB acting slowly (it

refrained from any rate changes at today’s meeting) Europe is going to

be under increasing downward pressure. The steady decline in the value

of the euro exchange rate speaks to what risks that have put in play.

| Main E-zone Countries and UK IP in MFG | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Mo/Mo | Jun 08 |

May 08 |

Jun 08 |

May 08 |

Jun 08 |

May 08 |

||||

| MFG Only | Jun 08 |

May 08 |

Apr 08 |

3Mo | 3Mo | 6mo | 6mo | 12mo | 12mo | Q-2 -Date |

| Germany: | 0.5% | -1.9% | -0.3% | -6.9% | -9.2% | -2.2% | -0.8% | 2.2% | 1.3% | -6.1% |

| France: IP excl Construction | #N/A | -2.6% | 1.5% | #N/A | -8.8% | #N/A | -1.7% | #N/A | -1.2% | #N/A |

| Italy | 0.2% | -1.5% | 0.4% | -3.3% | -4.9% | 1.5% | 1.1% | -2.0% | -2.6% | -2.5% |

| Spain | -4.9% | -14.8% | 27.5% | 13.9% | -33.7% | -17.5% | -10.0% | -9.6% | -7.7% | 2.2% |

| UK | -0.5% | -0.6% | 0.0% | -4.2% | -4.2% | -1.5% | -1.0% | -1.3% | -0.9% | -2.9% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief