Global| Jun 24 2021

Global| Jun 24 2021German Recovery Continues to Progress

Summary

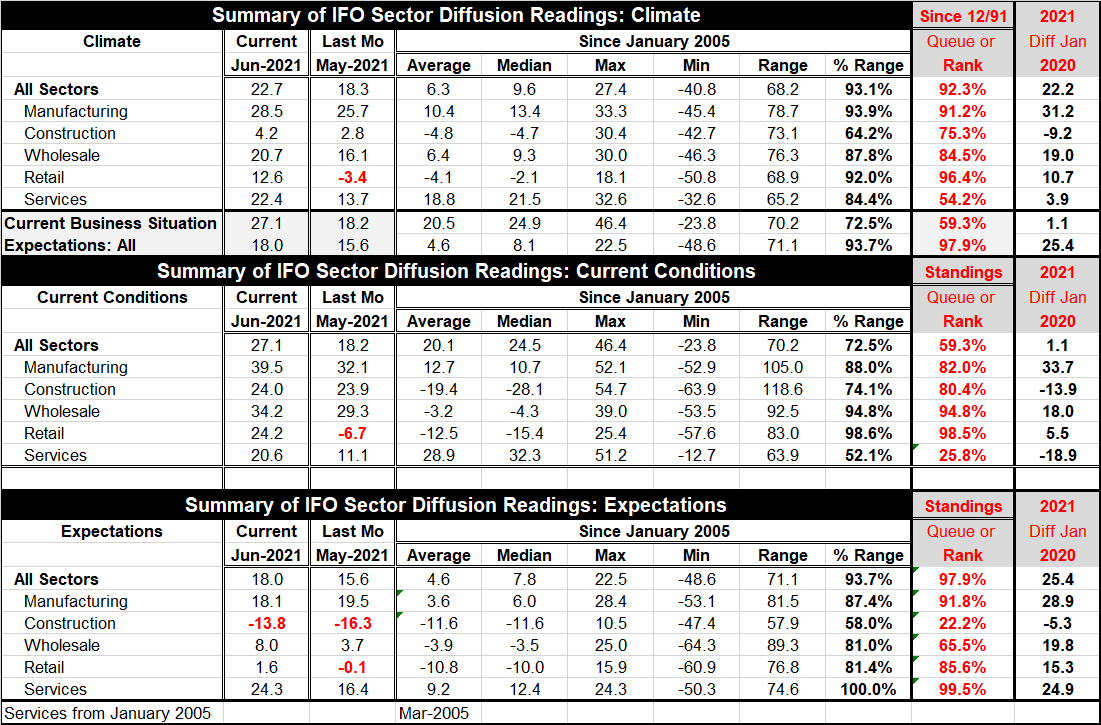

All sector climate in the IFO framework rose to a net reading of 22.7 in June from 18.3 in May. The current business situation improved to 27.1 from 18.2, while expectations moved up to 18.0 from 15.6. Climate and current conditions [...]

All sector climate in the IFO framework rose to a net reading of 22.7 in June from 18.3 in May. The current business situation improved to 27.1 from 18.2, while expectations moved up to 18.0 from 15.6. Climate and current conditions seem to improve a lot on the month but not so much for expectations. In contrast, climate and expectations hold historically high readings while current conditions have only a middling assessment despite this improvement this month. German industry is a study in contrasts.

All sector climate in the IFO framework rose to a net reading of 22.7 in June from 18.3 in May. The current business situation improved to 27.1 from 18.2, while expectations moved up to 18.0 from 15.6. Climate and current conditions seem to improve a lot on the month but not so much for expectations. In contrast, climate and expectations hold historically high readings while current conditions have only a middling assessment despite this improvement this month. German industry is a study in contrasts.

An ongoing German recovery

A clear pattern emerges about the state of the German economy. Recovery is in progress. The all sector climate index shows high 80th percentile standings as all sectors except construction (75.3%) and services (54.2%). For current conditions, four of the sectors have 80th-90th percentile standings yet the overall sector rating is only in its 59.3 percentile. This is because the one lagging sector; services is very weak with a standing in its 25.8 percentile. For expectations, this scenario flips and here the services sector has a 99.5 percentile standing and it is the highest reading ever for the services sector. Its net diffusion reading on the month jumped to 24.3 from 16.4. Suddenly the sector that has held everything back is expected vault ahead as the all-sector expectation has a very strong 97.9 percentile standing even with construction at a 22.2 percentile standing and wholesaling at a 65.5 percentile standing. Retailing expectations have a strong 85.6 percentile standing with manufacturing at a 91.8 standing. Clearly the services sector is driving the metrics for conditions, expectations, the current condition and climate.

Climate

All climate and standings are above their midpoints, above a reading of 50. And all diffusion values are net positive in June. Retailing made an especially sharp move, rising from -3.4 in May to +12.6 in June. Retailing and services made the strongest moves higher in June.

Current Conditions

Current conditions saw improvement across the board as well with a large jump in retailing, a sector that also crossed over from a net negative reading in May to a strong positive reading in June. Services also made a strong step higher. But the services metric for current conditions still lags below its median observation with a sub 50% standing (25.8%).

Expectations

For expectations, circumstances are different. The big improvement month-to-month is in services, a gain that takes it to its highest reading ever. Expectations overall are quite strong. Manufacturing has improved so much that it is the sole sector that backtracks in June but still has a percentile standing in its top 10 percent. Confidence in the construction sector has been lacking and that continues; construction has a standing below its median plus a net negative declining signal. Retailing ticks up to a positive reading, but it’s not much of a month-to-month gain. Perhaps the large improvement in current conditions calls for a less ebullient outlook from here on for retailing.

Since Covid struck

We can assess where these indexes sit compared to January 2020 just before the virus struck. Both the climate and expectations all-sector indexes are up by over 20 points on that comparison. But current conditions are only 1.1 point higher on that comparison and that is with wide sector differences. Construction and services both are lower on balance by double digits. But manufacturing and wholesaling sectors are each up by stronger double digits; for manufacturing it’s a gain of 33.7 points. Retailing is higher by 5.5 points.

Summing up

What the IFO survey shares with us this month is a bottom line assessment that whatever the bottom line is there is substantial unevenness across sectors. Usually in this framework, services are the odd man out. And the services sector does carry extra weigh as the principle employment sector; even when its performance is isolated, it is still important. But we can see very different degrees of improvement from January 2020. Current conditions readings are somewhat more uniform and consistent even across queue percentile standings except for services. Climate shows consistent firm-to-high queue standings amid uneven net diffusion readings for June and a weak services standing. It’s not really a time to make overarching statements about the German economy. However, there are two valid observations: the economy is progressing and the progress now seems to depend on expectations for the services sector being met.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief