Global| May 20 2016

Global| May 20 2016German PPI Drops with Upward Pressure Mounting and a Mixed Future

Summary

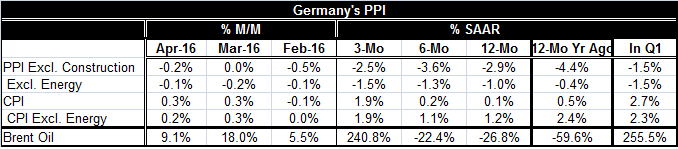

The German PPI (ex-construction) fell by 0.2% in April, returning to its declining ways after a flat performance in March. PPI declines are still in force even as oil prices are rising strongly. Brent rose by 18% in March and by an [...]

The German PPI (ex-construction) fell by 0.2% in April, returning to its declining ways after a flat performance in March. PPI declines are still in force even as oil prices are rising strongly. Brent rose by 18% in March and by an additional 9.1% in April. Oil has switched from declining at 20%-plus annualized rates over six months and 12 months to advancing over three months at a 240.8% annualized rate.

The German PPI (ex-construction) fell by 0.2% in April, returning to its declining ways after a flat performance in March. PPI declines are still in force even as oil prices are rising strongly. Brent rose by 18% in March and by an additional 9.1% in April. Oil has switched from declining at 20%-plus annualized rates over six months and 12 months to advancing over three months at a 240.8% annualized rate.

PPI-CPI trends are less connected

The German CPI, also displayed in the table, shows some pick up already in train in terms of sequential pressures. The year-on-year German CPI is still up by only 0.1% and the ex-energy CPI is up a more robust 1.2%. While the PPI usually moves ahead of the CPI, the relationship between the core PPI and the core CPI for Germany is very loose. Still, the coming pressure in the PPI pipeline from oil seems a real threat despite current PPI and core PPI trends which show prices are still dropping.

The impact of the euro on the PPI

One possible threat to the restoration of PPI inflation is the impact of the euro. Euro exchange rate movements can offset or amplify oil-price pass-through effects. In addition, if the euro is pushed by movements in the dollar, particularly in the wake of a Fed interest rate move, we could find considerable push-back against rising oil-induced inflation pressures. A rising dollar will tend to depress global (dollar-priced) commodity prices as we have seen in the past. Ironically, as oil prices rise and give the Fed a sort of all-clear signal, the Fed prepares to hike rates boost the dollar and push oil and other commodity prices back down.

Global impact of Federal Reserve policy

The Fed seems oblivious to the global repercussions of its actions or is willing to treat them as de minimis. A growing cadre of Fed members is looking to hike rates as the Fed is preparing to implement its process to restore what it sees as normalcy in the U.S. interest rate structure. There is more at stake here than just the Fed deciding to raise rates as part of its domestic policymaking obligations. The global implications are clear. Once the Fed re-launches its rate hike effort, everything will be in play again. Then we will see if the linkages from Fed actions to exchange rates and through global commodity prices remain as strong as they were previously. That in turn will have implications for German inflation, the EMU exchange rate and for ECB policy as well as for policies pursued elsewhere. Based on rhetoric from the U.S., the game could be on soon. Is the Fed right in putting its own objective ahead of those of the global economy? Is the U.S. policy objective even correct? We are also on the road to finding that out. There is no knowing. There are opinions. And the process will be hit or miss in nature. In all likelihood, a bumpy rise lies ahead.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief