Global| Sep 06 2019

Global| Sep 06 2019German IP Falls by 0.6%; Output Is Falling and Sequentially Decelerating

Summary

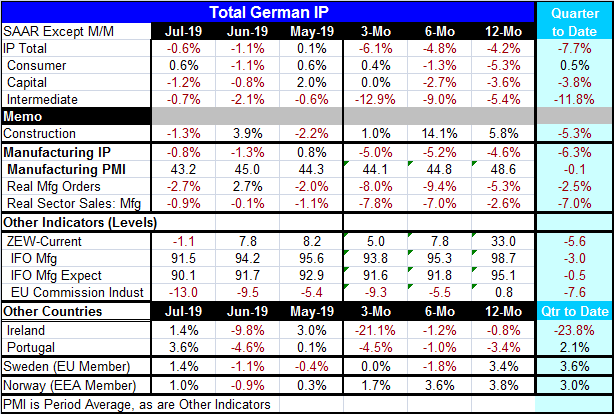

Germany's industrial output fell by 0.6% in July, having fallen for two months running. It has also fallen in three of the last four months with the only rise being a tiny 0.1% gain in May. This is a clear weak stretch for German [...]

Germany's industrial output fell by 0.6% in July, having fallen for two months running. It has also fallen in three of the last four months with the only rise being a tiny 0.1% gain in May. This is a clear weak stretch for German manufacturing.

Germany's industrial output fell by 0.6% in July, having fallen for two months running. It has also fallen in three of the last four months with the only rise being a tiny 0.1% gain in May. This is a clear weak stretch for German manufacturing.

The featured chart shows that the dizzying descent of manufacturing IP is also captured in the IHS Markit PMI for German manufacturing. The decline is real and displayed with consistency in both reports.

The table below chronicles several German indicators; weakness is the overpowering, cloying, theme that binds them together. The manufacturing PMI is below 50, showing contraction even in its 12-month average. Real manufacturing orders are declining on all three horizons in the table (three-month, six-month and 12-month) as are real sector sales. The ZEW current reading has just gone negative in July, but its sequential readings have been steadily slipping. The IFO manufacturing gauge also is sequentially lower, falling from a 98.7 average over 12 months to a six-month average of 95.3 onto a three-month average of 93.8. Manufacturing expectations have been slipping too, but their slippage has slowed. The EU Commission reading on manufacturing echoes all this weakness and deterioration in the manufacturing sector.

However, viewing manufacturing, its sector sequential changes shows a three-month improvement for consumer goods output and flat capital goods output. The overall IP index for manufacturing is dragged lower on the force of a sharp ongoing slide in the performance of intermediate goods where secular deterioration is in full force.

Germany is the largest economy in the EMU and so it gets the greatest weight in consolidated EMU data. It is not surprising that the EMU IP path strongly mirrors the performance in Germany. However, because the EMU is a common currency and because there is so much intra-union trade that there are other commonalities that cause fellow EMU members to follow the same course as the German economy; it's not just the weight of the German economy in the index.

Germany is the largest economy in the EMU and so it gets the greatest weight in consolidated EMU data. It is not surprising that the EMU IP path strongly mirrors the performance in Germany. However, because the EMU is a common currency and because there is so much intra-union trade that there are other commonalities that cause fellow EMU members to follow the same course as the German economy; it's not just the weight of the German economy in the index.

Despite differences in their respective sequential growth rate the main German sectors all are undergoing deterioration and for the most part their rates of declines are and have been clustered together.

German IP and German real orders typically move together. Orders do seem to lead manufacturing output by several months as they peak sooner then turn lower before output does. Still, both series are in sync; that underscores that the weakness in German manufacturing is real, relatively severe, and likely to persist.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief