Global| Jun 25 2014

Global| Jun 25 2014German GfK Consumer Climate Improves as ZEW and Ifo Drop

Summary

The GfK German consumer confidence indicator rose to 8.9 in July from 8.6 in June. This forward looking indicator sits in the top 3% of its historic queue. Its components that lag by one month are also quite strong. The economic [...]

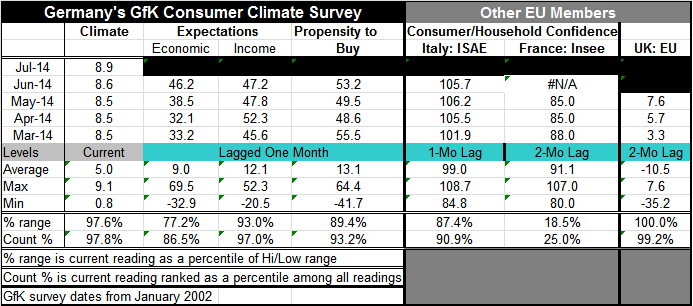

The GfK German consumer confidence indicator rose to 8.9 in July from 8.6 in June. This forward looking indicator sits in the top 3% of its historic queue. Its components that lag by one month are also quite strong. The economic variable is in its 86th percentile; the income variable is in its 97th percentile; and the propensity to buy indicator is in its 93rd percentile. These are extremely strong readings.

The GfK German consumer confidence indicator rose to 8.9 in July from 8.6 in June. This forward looking indicator sits in the top 3% of its historic queue. Its components that lag by one month are also quite strong. The economic variable is in its 86th percentile; the income variable is in its 97th percentile; and the propensity to buy indicator is in its 93rd percentile. These are extremely strong readings.

Comparing other European sentiment indicators, we find that Italy has been making gains and is also strong. Its confidence indicator is now in its 90th percentile. The UK is doing extremely well and its indicator is in its 99th percentile. However, France, a country that is lagging on all economic fronts, is also lagging very badly on the consumer confidence front. Its sentiment indicator from Insee stands in this 25th percentile; it is higher 75% of the time. France is a world apart from Germany, the UK and surprisingly, from Italy.

While the German consumer attitude index continues to push higher, it's interesting to note that both the ZEW and the Ifo business-oriented indices have been turning lower. We plot the GfK consumer climate index against the diffusion treatment of the Ifo business climate index. On that chart, you can see that these two indices broadly move together over the business cycle. However, the GfK consumer confidence index rises with more gusto than does the Ifo index and has been doing so for the past two years. When these indices last peaked, more or less together, in 2007, the GfK index peaked first, but retained its peak reading for longer than did the Ifo. The GfK index hit its low first and rebounded although the Ifo rebounded then progressed to rise faster than thr GfK. From 2011 onward, the Ifo index has been moving erratically sideways and lower. From 2011 the GFK index moved sideways for a while; however, from early 2013, it has moved relentlessly higher. A split has developed between these two indices. The GfK is higher and still rising, while the Ifo is lower and is dipping. As a result, we have the GfK index basically back to a new high, while we have the Ifo index well below its previous double peaks and with negative momentum.

These two indicators seem to be telling us different stories about the German economy. Industrial measures, (as I include the ZEW index here) ran out of gas and are showing signs of decay. Yet, the consumer treatment from GfK continues to move to new heights. If we look at the EU indices which only are updated to May, we don't see anywhere near that kind of strength in consumer confidence as in the German GfK index. German consumer confidence is still moving up in the EU treatment but not to a new high. The EU indicators still have Germany and Italy moving up with France remaining weak, quite weak and moving sideways. Thus, from the EU indices we get the same relative stories about consumer confidence trends, but not the strength for Germany.

The GfK presentation of consumer confidence gives Germany an ultra-high rating for confidence compared to other treatments. Business and consumer confidence are different things; if they are prone to move together in any one country, that country would be Germany due to its industrial dependence. Moreover, Germany seems to be up against a number of conflicts, including geopolitical conflicts that we would expect to take some toll on its measured confidence. The fact that GfK has not responded to this makes its strong assessment of the German consumer attitudes somewhat suspicious.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief