Global| Nov 15 2019

Global| Nov 15 2019EMU Trade Balance Is Hovering as Trade Flows Slow

Summary

The one point of crystal clear clarity on the issue of trade is that trade flows are slowing down. One –sometimes exception is for nonmanufacturing goods where commodity prices are playing a role rather than stronger trends in [...]

The one point of crystal clear clarity on the issue of trade is that trade flows are slowing down. One –sometimes exception is for nonmanufacturing goods where commodity prices are playing a role rather than stronger trends in volumes. That fact renders that particular exception as pretty meaningless. However, we often get nominal trade data before we get data on volume and break-outs omitting nonmanufactures are less accessible as well. To the extent, we can break down and assess trade flows; they remain weak and largely weakening.

The Baltic dry goods index, an index of actual shipping volumes that had been reviving since March, has been in a rapid state of decline over the past five weeks (see Chart on top right). Of course, the concern about trade is more forward-looking than what this chart depicts and it centers on the U.S.-China trade war. Still, the message here is that, despite some scattered optimism, trade trends are still challenged. And there are other related issues on trade to be aware of…there is a threatened tariff on autos that automakers are watching carefully and then there is whatever impact will come under Brexit, should, or when, Brexit comes to pass in the wake of the British elections.

Slowdown trends

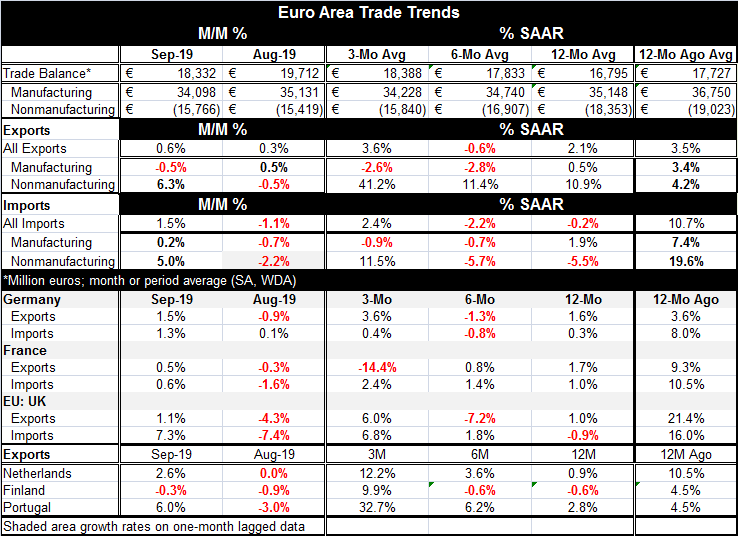

EMU-wide exports and imports have annualized trade flows over 12 months, six months and three months for which the overall growth rates are trapped between -2.2% and +3.6% on those three horizons (yes, annualized growth rates!). Exports and imports of manufactured goods are contained by that range of growth rates as well, but nonmanufactures exceed that range more or less consistently.

The table shows export results for six countries as well as for the EMU overall and in each case exports over the last 12 months post weaker growth than they do over the previous 12 months. Germany and France show data for imports and imports that also conform to this broad year-to-year slowdown phenomenon. The U.K. also logs import data; and U.K. imports, while falling over 12 months, show some life over three months and three-month life for exports as well.

For all of the EMU the deficit on nonmanufactures trade has fallen steadily and is now below its 12-month average. The surplus on manufactures trade has very gradually eroded and is also lower in September than its 12-month average.

Trends within one year

While the year-to-year trade trends in this table show some clear deceleration, looking within one year the trends are less clear overall. Still, for manufacturing goods both exports and imports are sequentially slowing in the EMU within one year. Total French exports show sequential slowing as well.

But the Netherlands, Finland and Portugal show sequential export acceleration for total exports. French imports and U.K. imports are sequentially accelerating too.

Summing up

On balance, the trends of less than a year are less clear in their message. But for the EMU, the manufacturing data show the slowdown persists on this set of dates as well so maybe that manufacturing goods slowing trend is more able to be generalized even if we lack the data here to show it.

While there have been some upside surprises in recent economic data, economic reports continue to show weak growth. Expectations data have received some lift possibly because of optimism on U.S.-China trade. But even there it is not clear how quickly trade trends would or could turn if there is a limited Phase-One agreement between the U.S. and China. Data for the U.S. today show that industrial production is declining somewhat sharply as the fourth quarter begins. Consumer spending is off to a slow start as well in the range of 1.4% in nominal terms early in Q4. U.S. inflation is still undershooting. In October, even excluding petrol, import prices are falling.

Markets are priced for optimism on the trade front, but as I mention above it is not clear how fast anything will return to normal under a phase one deal. Moreover, that which is ‘normal’ for this environment is also weak. That brings us back to the observation that trade weakening overall and manufacturing goods trade flows are the real constants, here. Trade flows are motivated by competitiveness conditions and demand growth. We can see that demand growth has been fading. And, of course, there is a lot of geopolitical discord ranging from Hong Kong to the Middle East and touching many points in-between. The U.K. is gearing up for a national elections and then dealing with Brexit. In the U.S., the divisive impeachment hearings go on - to what effect I am not sure. Neither side seems to be winning the battle for people’s hearts and minds. Minds seem to be made up- both inside and outside of Washington DC. Still, it is hard to imagine that all this pressure isn’t taking some toll on the President who wakes up every day with a new battle on his doorstep.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief