Global| Aug 04 2020

Global| Aug 04 2020EMU PPI Makes a Long Overdue Monthly Gain

Summary

Global growth is weak; unemployment globally has been rising from its previous cycle lows. There is slack in the global economy that is paired with ongoing weak growth. Although there is a great deal of fiscal and monetary stimulus [...]

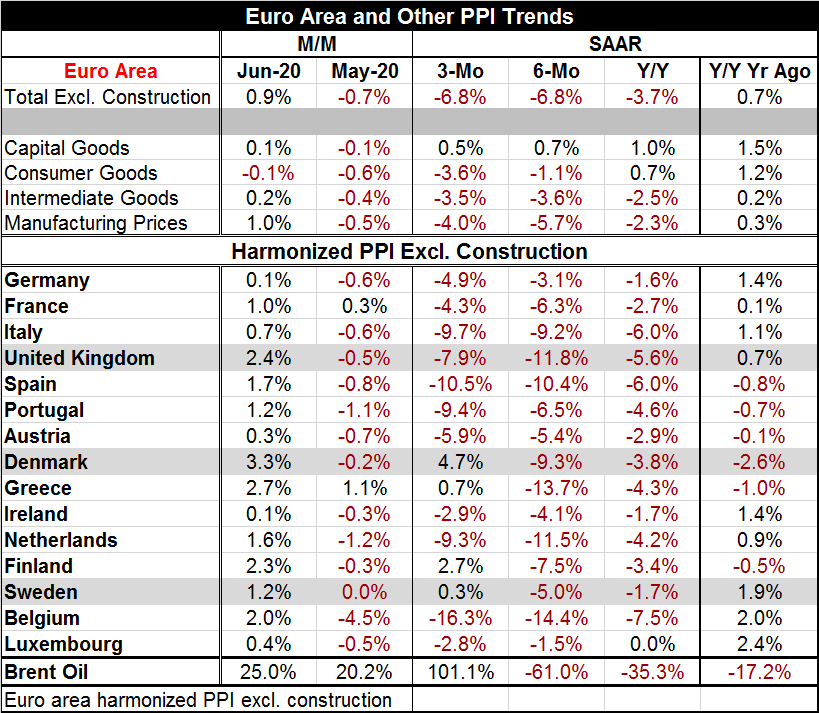

Global growth is weak; unemployment globally has been rising from its previous cycle lows. There is slack in the global economy that is paired with ongoing weak growth. Although there is a great deal of fiscal and monetary stimulus being used together – a bit like taking drugs and drinking alcohol at the same time- the adverse impact of those joint policies is evident nowhere as the slack and weakness and concern about growth all have helped to keep inflation under wraps. The EMU PPI did rise by a strong 0.9% month-to-month in June, its first monthly net gain since January. But inflation and its trends are still weak with the year-on-year PPI falling by 3.7% in the EMU as of June.

Global growth is weak; unemployment globally has been rising from its previous cycle lows. There is slack in the global economy that is paired with ongoing weak growth. Although there is a great deal of fiscal and monetary stimulus being used together – a bit like taking drugs and drinking alcohol at the same time- the adverse impact of those joint policies is evident nowhere as the slack and weakness and concern about growth all have helped to keep inflation under wraps. The EMU PPI did rise by a strong 0.9% month-to-month in June, its first monthly net gain since January. But inflation and its trends are still weak with the year-on-year PPI falling by 3.7% in the EMU as of June.

The chart memorializes the year-on-year paths for sector PPI inflation rates over 12-month periods. By sector, inflation is still deflating year-over-year for capital goods, consumer goods and intermediate goods. And inflation is still deflating within the annual framework from 12-months to six-months to three-months for the following: (1) headline inflation, (2) capital goods inflation, (3) consumer goods inflation, and (4) intermediate goods inflation. Those are very broad brushstrokes that mark the state of inflation as controlled and perhaps even too controlled and too contained.

The data table below presents overall PPI trends for 15 European economies, 12 of whom are some of the longest-lived members of the EMU community. The trends across these countries make another statement of how controlled inflation is in Europe.

Inflation trends in Europe are impressively contained:

• Year-over-year prices are falling in every country in the table except Luxemburg where the 12-month PPI is flat over 12 months.

• Inflation is also lower over 12 months than it was over the previous 12 months in every country in the table with no exceptions.

• Over six months, prices are falling in every country in the table.

• Over six months, inflation is lower than it is over 12 months for every country in the table.

• Over three months, prices are falling in all the EMU member countries except Finland. Over three months, prices also are rising in Denmark and Sweden.

• Over three months, inflation is lower than it has been over six months in seven of twelve EMU member countries. For the whole 15-member panel, inflation is falling in seven countries and rising in eight when three-month and six-month rates of change are considered.

• However, oil prices that have helped to drive the trend for inflation lower are starting to turn higher.

• Brent oil prices fall on balance over 12 months and six months and fall faster over 12 months than over the previous 12 months and fall faster over six months than over 12 months.

• But over three months, the Brent oil price picnic of progress ends. Over three months, Brent prices soared at a 101.1% annual rate! Brent oil prices rose by 20.2% in May and rose again by 25% in June. But oil is not simply 'back.' Oil has made some recovery, but global growth is still uneven and its future is unclear. In the U.S., energy prices have recovered enough that some fracking has restarted, increasing the supply of oil again effecting some push-back against rising oil prices. And the outlook for the virus and its impact on growth remains uncertain and that uncertainty fails to underpin oil prices as well. So oil has had some recovery, but the way forward will not be to extrapolate that trend higher at least not at the same pace.

Of course, in June partly on the back of these oil price moves month-to-month PPI prices rise in each of our 15 sample countries. Prices rise for capital goods and intermediate goods with only consumer goods prices barely ticking lower month-to-month.

After seeing inflation whacked by oil, which was a complicated affair in and of itself, there is now the ongoing sluggishness in the global economy and an uncertain outlook for that economy as the virus spreads and lingers. No one is quite sure what it will bring next. There are also hostile political relations between the two global trading giants, the U.S. and China. There may be some reset in that relationship after the U.S. elections in November, but for now there are geopolitical tensions to add to the virus uncertainty and still an unsatisfactory balancing act in the oil market.

'More' is just a four-letter word

The way ahead for the global economy still has a lot of unknowns to be worked out. But even if there is a miracle cure for the virus discovered, there will continue to be interruptions to growth through at least the middle of next year. Vaccines, even if they work, take time to manufacture, to distribute and to administer. The stock market keeps trading on the basis of the glass being half full and ready to be refilled. However, heath experts seem to take the view that however full the glass is, it is at risk of being spilled; they are constantly cautioning people and firms to do less. At some point, 'more' might become allowable, but for now that day seems far off.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief