Global| Oct 02 2008

Global| Oct 02 2008EMU PPI Finally Loses Some Momentum

Summary

Today Jean Claude Trichet opened the door to a consideration of changing interest rates in the direction of a cut. It was a surprise and the impact of the statement stung the euro. But be clear that inflation remains wildly over the [...]

Today Jean Claude Trichet opened the door to a consideration of changing interest rates in the direction of a cut. It was a surprise and the impact of the statement stung the euro. But be clear that inflation remains wildly over the top of the ECB ceiling. Trichet speaks of increased risk to the downside of the economy but continues to give lip service to upside (inflation) risks lingering. It does not seem he is yet ready to unlock the way. The way is shut, as Aragon once was told in the Lord of the Rings trilogy. Of course he eventually found a way to open it and save the day, as may Trichet.

And while PPI headline pressures have abated at long last, the picture and the dynamics of the PPI are still NOT what you would like to see if you are a central bank wanting to cut rates. The ECB that prides itself on being a one-mandate central bank is in no position to ague that it has done any better a job on the inflation fighting than has the Federal Reserve in the US with multiple mandates.

The PPI fell by a sharp 0.5% in August (PPI excluding construction) a huge drop really and with that drop, three month inflation is now ‘down’ to 7.3% at an annual rate. It breaks an accelerating trend for headline inflation that is at 9.5%, higher than its 12-month rate at 8.5% and that is higher than its year-ago annual rate of 1.8%.

Still, PPI inflation ex-energy continued to rise. The 0.2% gain is moderate but it comes on the heels of a 0.6% rise in July. Three month ex-energy PPI inflation is at a pace of 4.6% over 3-and 6-months and that pace is an acceleration from its 4.3% yr/yr pace.

By component the PPI is not behaving all that well either:

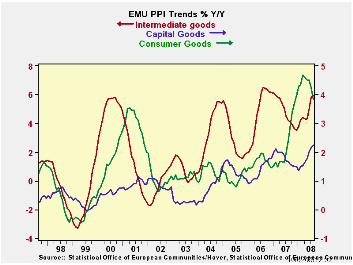

- Capital goods inflation is moderate but still exceeds the 2% HICP ceiling that the ECB sets. Moreover at 2.5% over three-months the pace is higher than its 2.3% over six months and its 2.2% yr/yr. Capital goods inflation may not be accelerating that much but it is still accelerating. Capital goods prices did rise by just 0.1% in August, however.

- Consumer goods inflation also is excessive but this is the sort of series a central bank could live with and still cut rates. With a rise of just 0.1% in August its three-month pace is 2.2%, its six-month pace is 2.5% and its Yr/Yr pace is 3.8% - far too high but definitely it has the right trend in place.

- For intermediate goods, prices rose by 0.2% in August and at a 6% pace over three-months, a 5.8% pace over six months and a 4.6% pace over 12-months. Not only is the pace is too high here but the trend is all wrong.

By Country Trends: Ex energy trends for Germany, Italy and the UK show a break off from a pattern of acceleration in the recent three-months. Still, for each of these counties the ex-energy PPI pace remains torrid at 3.7% over three-months for Italy, the lowest three-month pace of the group; at 6.5% the UK has the highest 3-mo ex energy pace.

The ECB will not be making monetary policy decisions based on the PPI. But the PPI is a pulse of inflation that the economy must deal with as it feeds into wholesalers and retailers and exporters. We can see clearly the weakness in the US economy and doubters now know that Europe remains linked to the US business cycle and its brief foray with de-coupling merely extended the leash that tethers it for a few added months. In seeing the weak US economy especially the ongoing construction drop and sharp fall in MFG via the ISM index Europe can see with some clarity the road ahead. It’s no wonder that Trichet wants to get out in front of the next big bend in the road. But he is careful about braking too soon since inflation is closing the gap on him and still tailgating at a rapid speed. The ECB would like inflation to show a milder hand and a broader trend of deceleration at least ex energy to salve its credibility were it to cut rates with the headline HICP above 2% by large margin.

This is the reason why HEADLINE INFLATION TARGETING IS WRONG.

I saw a rather dumb movie yesterday on cable in which the main actor made the point to a little boy he was coaching. He said don’t make a promise you can’t keep, kid: dumb movie, but good advice. Europe and the UK have this problem to a far greater extent than does the US. While the US central bank is still criticized for targeting the wrong thing (core) The Fed is closer to keeping inflation within reason of its ‘zone of preference’ than is the ECB. Interestingly each country has very similar year over Year headline and core inflation traits. So the ECB’s headline pledge did not really cause it to react any differently than did the Fed. I would repeat this notion that for a central bank you should not target something unless to are serious about hitting it. And no one is serious about containing inflation at a 2% ceiling as oil prices spurt as they did. For core inflation that’s another matter. And even with its banking crises and dual mandate the Fed is holding closer to its desired mark than is the ECB – and by a long shot. So who has credibility here: the Fed or the ECB?

| Euro Area and UK PPI Trends | ||||||

|---|---|---|---|---|---|---|

| M/M | Saar | |||||

| Euro Area 15 | Aug-08 | Jul-08 | 3-Mo | 6-MO | Yr/Yr | Y/Y Yr Ago |

| Harmonized PPI excl Construction | -0.5% | 1.3% | 7.3% | 9.5% | 8.5% | 1.8% |

| Excl Energy | 0.2% | 0.6% | 4.6% | 4.6% | 4.3% | 3.0% |

| Capital Gds | 0.1% | 0.3% | 2.5% | 2.3% | 2.2% | 1.7% |

| Consumer Gds | 0.1% | 0.2% | 2.2% | 2.5% | 3.8% | 2.4% |

| Intermediate & Capital Goods | 0.2% | 0.7% | 6.0% | 5.8% | 4.6% | 3.2% |

| Energy | -2.5% | 3.2% | 14.8% | 25.2% | 22.5% | -1.9% |

| MFG | -0.6% | 0.6% | 3.1% | 7.1% | 6.5% | 2.3% |

| Germany | -0.6% | 2.0% | 9.2% | 10.4% | 8.1% | 1.0% |

| Excl Energy | 0.2% | 0.7% | 4.6% | 4.3% | 3.5% | 2.6% |

| Italy | -0.2% | 0.8% | 5.4% | 8.6% | 8.2% | 2.1% |

| Excl Energy | 0.2% | 0.2% | 3.7% | 4.6% | 4.2% | 3.1% |

| UK | -1.8% | 0.9% | 7.3% | 16.5% | 18.6% | 0.3% |

| Excl Energy | 0.2% | 0.6% | 6.5% | 9.8% | 7.7% | 3.0% |

| The EA 15 countries are Austria, Belgium, Cyprus, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Malta, Netherlands, Portugal, Slovenia and Spain. | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief