Global| Sep 11 2019

Global| Sep 11 2019EMU Inflation Remains Low, Growth Weak; Focus in on Thursday's ECB Meeting

Summary

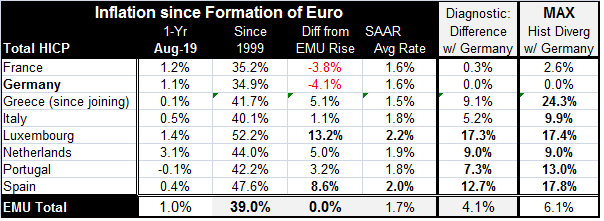

The early reporters of August's HICP that are ‘original' EMU members are listed in the table. EMU inflation is low; most member inflation rates are low and below the pace set for the EMU-wide HICP itself. There are no country level [...]

The early reporters of August's HICP that are ‘original' EMU members are listed in the table. EMU inflation is low; most member inflation rates are low and below the pace set for the EMU-wide HICP itself. There are no country level targets. The chart shows trends in three key countries. Germany which has been the low inflation country and that used to dominate the low end of inflation among EMU members until the Great Recession struck.

The early reporters of August's HICP that are ‘original' EMU members are listed in the table. EMU inflation is low; most member inflation rates are low and below the pace set for the EMU-wide HICP itself. There are no country level targets. The chart shows trends in three key countries. Germany which has been the low inflation country and that used to dominate the low end of inflation among EMU members until the Great Recession struck.

The chart shows how, prior to locking in the fixed currency values in January 1999, both Spain and Greece were running inflation rates well above what EMU discipline would require. However, those rates came closer into line – still running too hot, after the euro was formed. However, Germany was the largest economy in the EMU and because of that its performance got a larger weight than for the rest of the EMU and compensated for the overshoots in Spain and Greece and other countries as the EMU area remained largely inflation compliant.

But after the Great Recession, Maastricht rules began to be enforced with a vengeance. Portugal, Spain, Greece and Italy were put under substantial austerity pressure. Greece went through painful and public debt renegotiations. As a result of fiscal austerity programs, inflation in the high inflation rate austerity countries came down steadily and inexorably. And so did growth…

The chart shows that from 2012 onward, among this small group of three countries Germany went from being the clear low inflation country to the high inflation country. From January 2012 onward, the German price level rose by 9.7%, Spain's price level rose by 6.7%, and Greece's price level fell by 1.2%. Germany became one of the annual high inflation countries in this small group in the period as austerity reduced inflation and limited growth elsewhere.

The legacy of these developments and the damage – despite the inflation progress – engendered by austerity continues to haunt the EMU today. In Italy, another austerity country, the Five Star movement has risen. Italy, with a brand new government, is still railing against the debt limits of Maastricht being imposed on it as Italy and Greece are the only two EMU countries with real GDP levels (yes, LEVELS) still below their prerecession marks of one decade ago. This kind of impact on growth almost necessarily creates blowback and has political consequences for which the EMU and the EU are still unprepared. In Spain, the party Podemos was formed to fight traditional parties and austerity. The pressure also helped to fuel nationalistic sentiment among the Catalans who made a since-quashed bid for a breakoff state. Portugal, too, continues to show dissent. In the EU, a new EU Commission slate has been elected with a wholly new gender-balanced make up and is facing a raft of new issues.

The United Kingdom left the EU- oops is leaving the EU… may be leaving the EU… is planning to leave the EU... will definitely leave the EU by October 31.. Well, you get the idea. Leaving the EU can he difficult and the U.K. has some unique circumstances that make its departure entangled. But the desire to leave came from Britain's disenchantment with their being told by Brussels what they could do and how they could do it. The migrant requirements were probably a back breaking issue. Many current EU member countries are similarly vexed with encroaching centralized EU control. But EU rules and requirements that go beyond what is necessary to streamline commerce have been the issue. The changes in the EU Commission we see being implemented are in part a response to EU-wide disaffection for the way that it has ruled and enforced the rules. Whether this Commission will be better-liked remains to be seen. As of now, it still has the same rules to enforce.

But there may be hope. Even Germany seems to be seeking a work-around for its own strict debt rules to enable it to take advantage of these super low financing rates in order to attack some infrastructure and environmental needs and issue more debt. Maybe there is still hope for change.

However, the sticking point in Europe is growth. And as this week's Thursday ECB meeting draws near, there is more opposition to Mario Draghi's plan for more monetary stimulus. Certainly, the load placed on the backs of the central banks has been too great. The Great Recession was substantially a reaction to debt, too much of it and not enough attention paid to who was allowed to run it up as well as how it was packaged. But in the aftermath of that blow up, it is still a world of rapid Asian progress in which Asian producers want to take a growing slice of a pie that is now growing much slower or, in the case of Italy and Greece, one that was downsized in absolute terms. So the burden to do something to relive pressure falls on the ECB. Yet, monetary solutions have been greatly overtaxed and Mario Draghi is now experiencing what looks like significant blowback on his proposals. We will see the results on Thursday.

It is not surprising that trade tensions have arisen but perhaps not as predictable that they rose because of U.S.-China conflict. While the U.S. has a point about unfair trade and while the assessments of Free Trade get very poor grades for the last 30 years, it is a bad time to seek to redress the system. There are simply too many shocks still reverberating through this system from the Great Recession itself as well as lingering or budding geopolitical issues. How Hong Kong will work out is anybody's guess. Nor is it clear whether events in Hong Kong will become a larger problem for U.S.-China relations or for ongoing trade negotiations. Whatever monetary policy does in the U.S. or in Europe, everything is still at risk to trade war developments. But is that an excuse to do less?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief