Global| Mar 31 2021

Global| Mar 31 2021EMU Inflation...A Reversal of Fortune?

Summary

EMU inflation in March and February is tranquil. But in the wake of a massive rise in January, calculated inflation rates for three-months and six-months are uncomfortably large. Year-on-year inflation in the EMU is just at 1.2%. That [...]

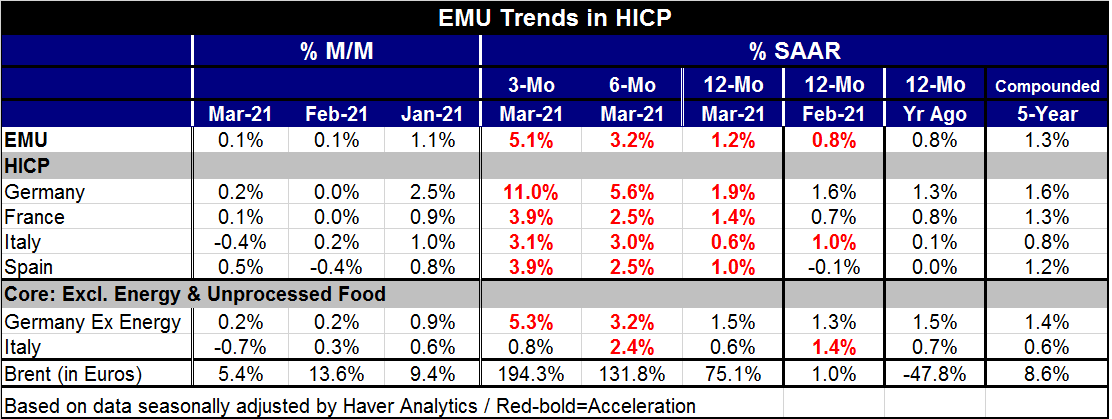

EMU inflation in March and February is tranquil. But in the wake of a massive rise in January, calculated inflation rates for three-months and six-months are uncomfortably large. Year-on-year inflation in the EMU is just at 1.2%. That pace is up from year-on-year pace in February (that was 0.8%) and it is above the year-on-year pace of 12-months before which was up by 0.8% as well. At a 1.2% annualized rate, inflation is still a tick below what it has averaged over the last five years (1.3%). This marks a massive undershoot compared to the ECB's target of just less than 2%.

EMU inflation in March and February is tranquil. But in the wake of a massive rise in January, calculated inflation rates for three-months and six-months are uncomfortably large. Year-on-year inflation in the EMU is just at 1.2%. That pace is up from year-on-year pace in February (that was 0.8%) and it is above the year-on-year pace of 12-months before which was up by 0.8% as well. At a 1.2% annualized rate, inflation is still a tick below what it has averaged over the last five years (1.3%). This marks a massive undershoot compared to the ECB's target of just less than 2%.

Inflation's pace is touch and go...in Germany

In Germany, inflation is on a tear; it is up at an 11% annualized rate over three months and up at a 5.6% annualized rate over six months; however, over 12 months, the HICP comes in just below or right at the pace that the ECB targets EMU-wide at 1.9%. The ECB seeks an inflation rate that is just under 2% and that is for the EMU-wide rate which weights the performance of all members. There are no separate country by country formulations, but Germans had adopted those same parameters for Germany under the Bundesbank before the EMU was formed. So in Germany itself, inflation is already in a touch-and-go state.

Germany stands more or less alone

Germany is alone is on this razors edge, at least among the largest EMU economies. Inflation is accelerating in the other large EMU countries as well but over three months annualized the pace is 3.1% to 3.9%. Over six months France Italy and Spain see inflation accelerating to a pace of 2.5% to 3.0%. And the year-over-year inflation in these three countries ranges from a low of 0.6% in Italy to a high of 1.4% in France.

Ex-energy trends are more subdued

We can glimpse ex-energy inflation in Germany and core inflation in Italy. Germany shows acceleration in its ex-energy rate as the pace rises to 5.3% over three months from 3.2% over six months and 1.5% over 12 months. German year-on-year ex-energy inflation does offer more breathing room than the headline HICP. Italy's core inflation rate fell in March dropping outright, not just slowing. It fell by 0.7%. Over three months Italian core inflation decelerates; however, it accelerates to a pace of 2.4% over six months but then it decelerated over 12 months running at just 0.6% compared to 0.7% over 12-months for the period beginning 12-months ago. Italian core inflation also decelerates month-to-month on an annualized basis with the annual gain of 0.6%, well below the gain of 1.4% reported in February. Italy also sees a deceleration in its year-over-year core pace in March compared to February.

Impact of oil

Of course, oil (and other commodity prices) is having an impact here. Brent oil prices rose by 9.4% in January, then by 13.6% in February and at the end of March Brent is up by 5.4% compared to February. The annualized gain over three months is a very hefty 194.3%, so it is not surprising that headline inflation is rising at a time like this. Still, the real bulge in oil prices is relatively recent as Brent is also up at a 131.8% annual rate over six months and then by 75.1% over 12 months. The upward pressure from Brent has been mounting.

Germany's domestic inflation gauge surged after year-end

These oscillations in oil prices up and down also drag the headline of the HICP up and down, but oil has a much more marginal impact on ex-energy and core prices. Germany where inflation is leading this dubious parade saw that inflation was well-heaved through December. Then, the domestic CPI headline gain over three months was just at a 1.1% annualized pace, but after that the annualized gain surged to 5.8% in January, 7.8% in February and 8.6% in March. These trends also are reflected in HICP patterns. Germany's core domestic CPI was actually flat over the three months ending in December 2020 then it surged to an annualized gain of 8.1% in January 2021 and pretty much held that pace at 7.7% over the three months ended in February 2021.

The past path of oil prices: Oil helped inflation to a shaky foundation

From June 2019 through February 2020, Brent was in the 50-euro per barrel range – the oil markets saw oscillations but in a moderately narrowed range. Of course, the virus struck and oil prices fell and sharply to €30.9 in March and to a low of €24.9 in April. After that, oil began to recover. For six months from June through November, oil prices traded in the range of €30. In December 2020, prices stepped up to €41.3. From there it traded at €45.2 in January 2021, then at €51.4 and currently is trading at about €54.2 per barrel. The price gains in 2021 have come quickly. And putting aside the point estimate for how much oil has risen, it is basically back in the same €50 per barrel range that it occupied from June 2019 through February 2020. And, of course, inflation in Germany and in the EMU slid sharply during that period when oil prices weakened form that range and now oil is beginning to recoup its losses, pushing the German domestic CPI and the HICP higher. The erratic run of Brent has provided an unstable base from which to measure inflation as Brent, EMU and Germany inflation rates have vibrated to the same rhythms over the past eighteen months or so.

Fingerprints from the virus

There is more to inflation than just oil prices. But oil can and does bounce around the HICP headline a lot. A good part of what we see in this historic re-telling of oil prices is when and how the virus impacted the economy as one of the main effects was also the impact on oil prices.

Current trends and policy

We do not hear the ECB complaining about inflation now because the main EMU inflation rate is not pressured relative to target. Short-term inflation is what's surging. But there is pressure in the pipeline. Moreover, the virus is still the number one problem and threat especially with European vaccinations lagging the U.S. and the U.K. And then there are the new virus variants circulating dangerously. Right now there does not seem to be any demand to take out the sharp pencils over inflation. It is not clear either how much (or ‘if') Europe will be willing to provide any flexibility for the past undershoots of inflation (the way the U.S. has done). Europe has given no hints that it might be willing to do that. Remember that the ECB has a ‘single objective' price stability for the HIPC just below a pace of 2%. For now all efforts are focused on economic revival; dealing with the virus has become the biggest issue for Europe, especially after being late to order vaccines. But soon some of these inflation facts will creep into the picture. Then policy making will become really difficult business.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief